Notícias do Mercado

-

23:46

White House: The President has made clear this bill has no chance of becoming law

“The President has made clear this bill has no chance of becoming law,” mentioned the White House (WH) spokesperson after the "Limit, Save, Grow Act" passed with a dicey majority late Wednesday.

The Republican debt ceiling bill crossed the White House barrier with a mostly partisan 217-215 vote, which in turn will lure US President Joe Biden to negotiate on cutting spending with House Speaker Kevin McCarthy and the Democratic team in Congress.

“The US House of Representatives on Wednesday narrowly passed a bill to raise the nation's $31.4 trillion debt ceiling, defying President Joe Biden by attaching sweeping spending cuts for the next decade,” said Reuters.

More comments from WH

US President Biden will never force middle-class and working families to bear the burden of tax cuts for the wealthiest.

We pay our bills, congressional Republicans must do that again now and act to avoid default.

Market sentiment improves

S&P 500 Futures print mild gains of 0.20% around 4,083 by the press time, following a mixed close of Wall Street.

Also read: Forex Today: A mixed US Dollar and cautious markets before crucial US data

-

23:39

GBP/USD Price Analysis: Continuous failure of instability above 1.2500 makes Pound Sterling delicate

- GBP/USD has shown a corrective move after failing to sustain above 1.2500.

- A survey from Reuters showed that most shop chains do not foresee a lasting improvement in retail sales.

- The lack of upside momentum in the Pound Sterling makes it a fragile counter for market participants.

The GBP/USD pair has gradually corrected after failing to sustain above the psychological resistance of 1.2500 in the Asian session. The Cable has failed plenty of times in sustaining above the aforementioned resistance this month, making the Pound Sterling prone to further losses.

On Wednesday, investors dumped risk-sensitive assets and ran for the US Dollar Index (DXY) as a safe-haven after First Republic Bank cornered the US administration for not providing liquidity support. The USD Index showed a V-shape recovery after dropping to near the crucial support of 101.00.

Meanwhile, the Pound Sterling sensed selling pressure amid a slowdown in accelerating British retail sales. A survey from Reuters showed that most shop chains do not foresee a lasting improvement in retail sales. Also, expectations for May were slightly negative. This might provide some relief to Bank of England (BoE) policymakers.

GBP/USD is auctioning in a Rising Channel chart pattern on a two-hour scale in which every pullback is considered a buying opportunity. It is worth noting that the lack of upside momentum in the Pound Sterling is making it a fragile counter for the market participants. The Cable is still above 20-period Exponential Moving Average (EMA) at 1.2468, indicating that the upside bias has not faded yet. Potential resistance is placed from April 14 high at 1.2545.

Meanwhile, the Relative Strength Index (RSI) (14) has slipped back into the 40.00-60.00 range, signaling a lack of momentum.

A decisive move above April 13 high at 1.2537 will drive the asset towards a fresh 10-month high at 1.2597, which is 08 June 2022 high. A breach of the latter will expose the asset to May 27 high at 1.2667.

On the flip side, a slippage below April 10 low at 1.2345 will expose the asset to March 30 low at 1.2294 followed by March 27 low at 1.2219.

GBP/USD daily chart

-

23:32

USD/CHF steady around 0.8900 amidst risk aversion, eyes 0.9000 on the double bottom formation

- USD/CHF remains steady at around 0.8900 amidst risk aversion and higher US T-bond yields.

- After the US economic data release, the major rebounded from daily lows and surged above 0.8900.

- USD/CHF Price Analysis: Double bottom looming could pave the way towards 0.9000, ahead of the 50-day EMA at 0.9100.

The USD/CHF remains steady at around 0.8900 after hitting a daily low of 0.8851 and appears to have bottomed after falling from last year’s highs of 1.0147. As the Asian session begins, the USD/CHF is trading at 0.8906, above its opening price by a minuscule 0.01%.

The main drivers for USD/CHF price action continue to be risk-jitters around the First Republic Bank crisis. Although triggered flows towards the Swiss Franc (CHF), higher US T-bond yields, bolstered the US Dollar (USD), capping the USD/CHF’s fall.

The US economic agenda featured Durable Good Orders for March, which jumped 3.2% MoM, above estimates. Excluding transport orders advanced 0.3%, and stripping defense and aircraft, fell 0.4% MoM. After the release, the USD/CHF bounced off the daily lows and rose above 0.8900.

Later in the New York session, Atlanta’s Fed updated its GDP NOW model, reigniting recessionary worries about the United States economy. The GDPNOW model foresees GDP for Q1 at 1.1% vs. a previous reading of 2.5%.

In the Europan session, the Swiss Economic Sentiment advanced to -33.3 points in April, an improvement compared to -41.3 points in March, according to data from Credit Suisse.

What to watch?

The US economic docket will feature Initial Jobless Claims and the Gross Domestic Product (GDP) Advance for Q1, 2023.

USD/CHF Price Analysis

From a daily chart perspective, a double bottom could be forming. Nevertheless, to cement the case, the USD/CHF must break above the April 19 high at 0.9003. A breach of the latter and the USD/CHF will challenge the 0.9050 figure before testing the 50-day EMA at 0.9103.

-

23:26

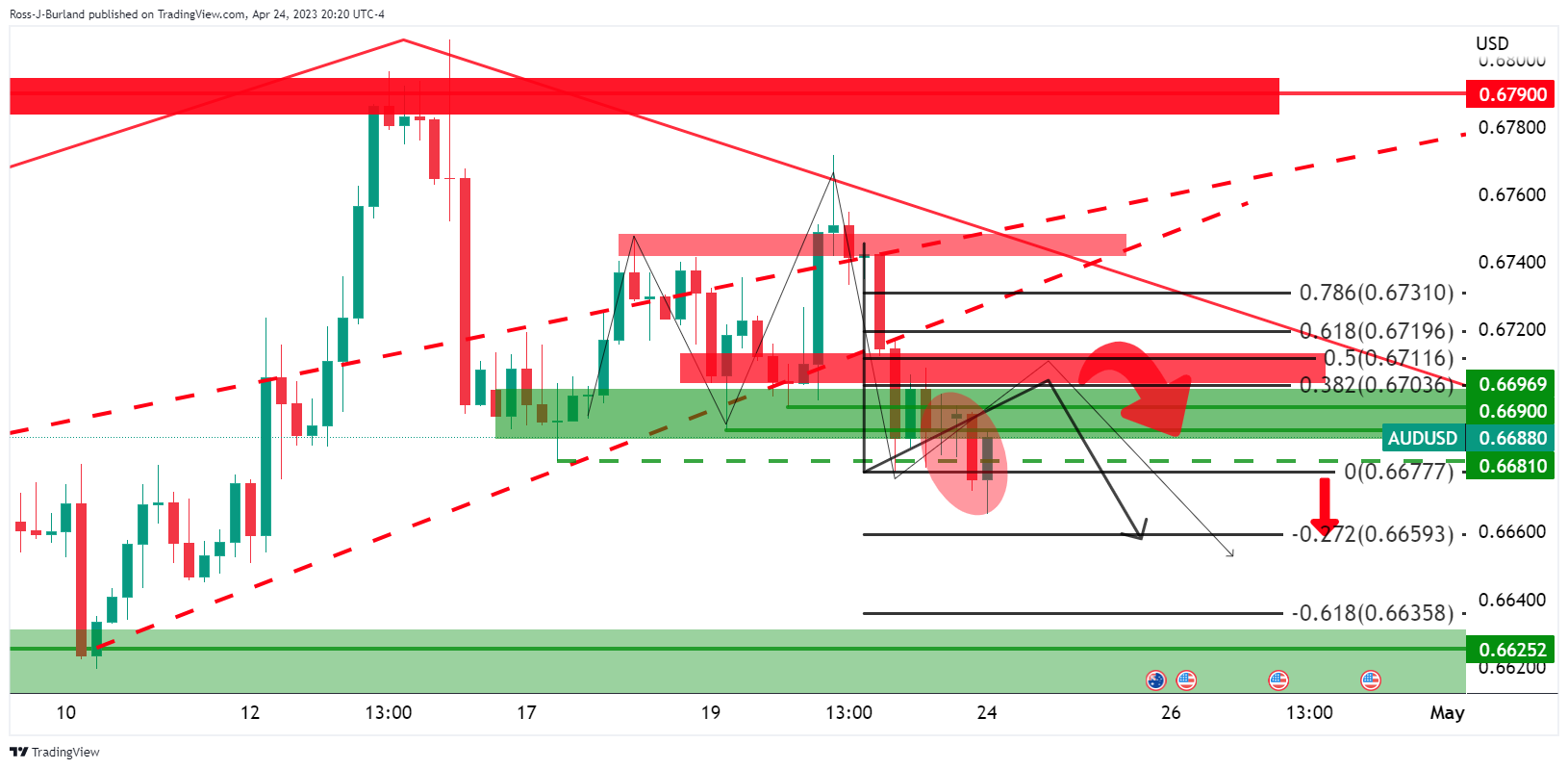

AUD/USD eyes further downside as bears prod 0.6600 amid banking woes ahead of US Q1 GDP

- AUD/USD licks its wounds at the lowest levels in six weeks.

- Mostly downbeat risk profile, mixed Aussie inflation clues weigh on AUD/USD price.

- Cautious mood before US GDP, First Republic Bank-inflicted fears and voting on US debt ceiling increase favor Aussie pair bears.

- Australia Export, Import Price Indexes for Q1 will be eyed ahead of the US growth figures.

AUD/USD consolidates recent losses at the 1.5-month low as it flirts with the 0.6600 round figure during early Thursday morning in the Asia-Pacific zone. In doing so, the Aussie snaps two-day downtrend but the bearish bias remains intact amid multiple negatives to the risk profile and surrounding the Reserve Bank of Australia’s (RBA) next move.

On Wednesday, downbeat Aussie inflation numbers justify the RBA’s pause in rate hike trajectory and suggested one such move in the next monetary policy meeting of the Australian central bank. However, the details weren’t too bad and hence may allow the RBA to show readiness of further rate hikes if needed.

That said, Australia’s Monthly Consumer Price Index (CPI) dropped to 6.1% YoY in March versus 6.6% expected and 6.8% prior. On the same line, the Q1 CPI also eased to 1.4% QoQ from 1.9% in previous readings but crossed the 1.3% market forecasts. Further, the RBA Trimmed Mean CPI declined below 1.4% consensus and 1.7% prior to 1.2% QoQ in the first quarter (Q1).

On the other hand, US Durable Goods Orders rose by 3.2% in March versus 0.8% expected and -1.2% prior. Further details suggest that the Durable Goods Orders ex Transportation and ex Defense also rose past market forecasts and previous readings in March.

It’s worth noting that the cautious mood surrounding the US debt ceiling expiration exerts downside pressure on the AUD/USD price as most policymakers aren’t agreeing on the measures suggested by US President Joe Biden. It should be observed that the US House of Representatives currently votes on a bill suggesting the increase in the debt ceiling and to cut government spending, known as the "Limit, Save, Grow Act". Although the passage of the bill is only one step closer to the final destination, any disappointment can add to the risk-off mood and exert more downside pressure on the AUD/USD.

Elsewhere, market sentiment sours amid escalating fears from the First Republic Bank (FRB) after the troubled bank’s shares dropped another 20% on Wednesday, following a 50% slump the previous day. With this, the FRB is likely to face the limits on its Fed borrowings, which in turn spreads the ripple effect across the markets and weighs on the risk appetite and the Aussie pair.

Against this backdrop, the US Dollar Index (DXY) dropped to the lowest levels in two weeks before paring some of the daily losses to end Wednesday’s trading near 101.43. Further, Wall Street closed mixed while the United States Treasury bond yields are mostly sidelined.

Given the mostly downbeat market sentiment and dovish bias surrounding the RBA, the AUD/USD pair is likely to remain pressured ahead of the key US first quarter (Q1) Gross Domestic Product (GDP), expected to ease to 2.0% on an annualized basis versus 2.6% prior. On an immediate basis, Australia’s Q1 Export Price Index and Import Price Index can entertain the pair traders.

Technical analysis

Unless providing a sustained break of the seven-week-old previous support line, around 0.6655 by the press time, the AUD/USD pair remains vulnerable of refreshing the yearly low, currently around 0.6565.

-

23:25

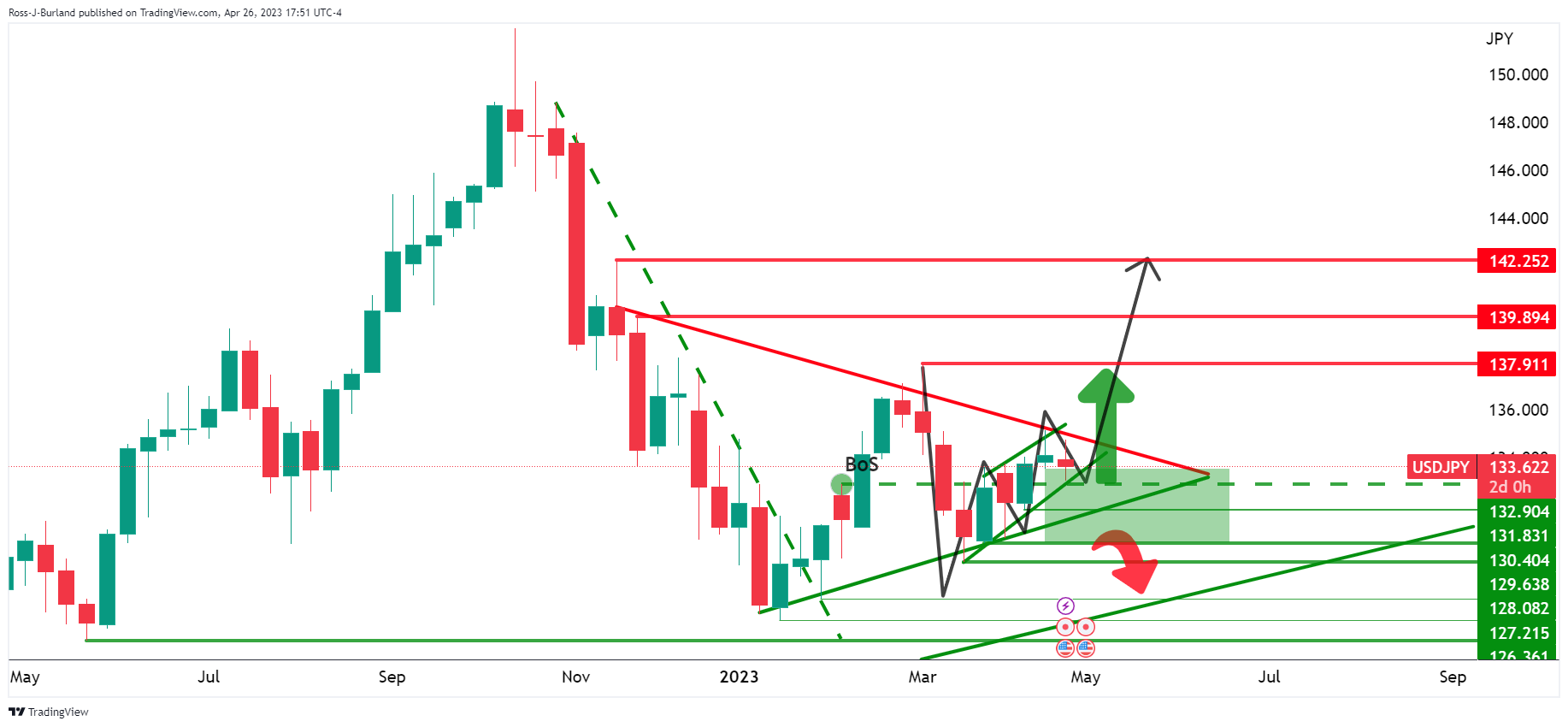

USD/JPY Price Analysis: Bulls taking a reincheck as bears eye 132.80s

- USD/JPY bears are in the market front side of the bearish trend.

- Bears are a meanwhile extension to the downside.

- Bulls are lurking on longer-term time frames.

As per the prior analysis, USD/JPY bears carving out a bias front side of bearish trend, the market remains in the hands of the bears, for the meantime, as the following analysis will illustrate.

The key notes for the near-term outlook are as follows:

- We have the head and shoulders formed.

- We have seen a break of the 4-hour structure.

- There has been a correction into the bearish trendline resistance meeting the 38.2% ratio.

- A downside continuation with 132.80 eyed.

USDJPY weekly charts

Zooming in on the weekly chart, we can see that a W-formation is taking shape with the potential for the correction to run deeper into the Fibonacci scale. The 38.2% ratio has already been met where trendline support meets the lows, so a bullish impulse could take shape from this point. However, monitoring for a deeper more to the 50% mean reversion could offer the patient bulls a discount.

USD/JPY H4 chart

We have the head and shoulders formed with the price on the back side of the prior rising trendline support that is now expected to act as a counter-trendline. We also have seen a break of the 4-hour structure and a correction into the bearish trendline resistance meeting the 38.2% ratio. Bears could engage here which would possibly result in a downside continuation with 132.80 eyed.

-

23:08

Gold Price Forecast: XAU/USD bulls lack conviction ahead of US GDP

- Gold price grinds lower after snapping two-day winning streak as bulls await the key United States statistics.

- Downbeat sentiment, mostly upbeat US data and steady Treasury bond yields prod XAU/USD bulls.

- Softer US Q1 Gross Domestic Product can enable Gold price to refresh 2023 high.

Gold price (XAU/USD) pares the first weekly gains in thee after snapping a two-day uptrend the previous day, depressed near $1,990 amid early Thursday. In doing so, the yellow metal justifies the market’s cautious mood ahead of the United States' first quarter (Q1) Gross Domestic Product (GDP), especially amid banking sector fears and recently mixed US data. That said, the US Dollar’s rebound during late Wednesday also exert downside pressure on the XAU/USD price. Furthermore, the ongoing voting on the bill suggesting an increase in the US debt ceiling adds to the market’s anxiety and keeps the Gold price on a back foot.

Gold price retreat amid escalating banking fears, pre-data anxiety

Gold price marked its first daily loss in three the previous day as market sentiment sours amid escalating fears from the First Republic Bank (FRB) after the troubled bank’s shares dropped another 20% on Wednesday, following a 50% slump the previous day. With this, the FRB is likely to face the limits on its Fed borrowings, which in turn spreads the ripple effect across the markets and weighs on the risk appetite and the XAU/USD.

Elsewhere, the cautious mood surrounding the US debt ceiling expiration also exerts downside pressure on the Gold price as most policymakers aren’t agreeing on the measures suggested by US President Joe Biden. That said, the US House of Representatives currently votes on a bill suggesting the increase in the debt ceiling and to cut government spending, known as the "Limit, Save, Grow Act". Although the passage of the bill is only one step closer to the final destination, any disappointment can add to the risk-off mood and exert more downside pressure on the Gold price.

On a different page, recently mixed US data also confuse the market players about the Federal Reserve’s (Fed) moves past May’s 0.25% rate hike.

On Wednesday, US Durable Goods Orders rose by 3.2% in March versus 0.8% expected and -1.2% prior. Further details suggest that the Durable Goods Orders ex Transportation and ex Defense also rose past market forecasts and previous readings in March. Before that, US Conference Board's Consumer Confidence Index edged lower to 101.3 for April, versus 104.0 prior. Additional details of the publication stated that the Present Situation Index ticked up to 151.1 during the said month from 148.9 prior whereas the Consumer Expectations Index dropped to 68.1 from 74 previous readings. Further, the one-year consumer inflation expectations eased to 6.2% in April from 6.3% in March.

Amid these plays, the US Dollar Index (DXY) dropped to the lowest levels in two weeks before paring some of the daily losses to end Wednesday’s trading near 101.43. Further, Wall Street closed mixed while the United States Treasury bond yields are mostly sidelined.

To sum up, the downbeat sentiment and recent pick-up in the DXY prods the Gold buyers ahead of the key United States Q1 GDP data, expected to ease to 2.0% on an annualized basis versus 2.6% prior.

Also read: Gold Price Forecast: Bears take control as concerns mount

Gold price technical analysis

Gold price remains depressed within a small trading area between an eight-day-old descending resistance line, around $2,010, and the $1,978 support confluence including the 200-bar Simple Moving Average (SMA) and a five-week-long upward-sloping trend line.

Given the steady Relative Strength Index (RSI) line, placed at 14, the latest grind is likely to continue. However, bullish signals from the Moving Average Convergence and Divergence (MACD) indicator suggest the XAU/USD’s further upside.

In that case, the Gold price needs a successful break of the $2,010 hurdle, which in turn could trigger the bullion’s run-up towards the monthly high of around $2,049.

Following that, the $2,050 round figure and 61.8% Fibonacci Expansion (FE) of the XAU/USD moves between March 15 and April 19, close to $2,070.

Meanwhile, the Gold price pullback remains elusive unless the quote stays beyond the $1,978 key support, a break of which won’t hesitate to direct the XAU/USD bears toward the late March swing low surrounding $1,934.

Overall, the Gold price remains on the bull’s radar as the United States Gross Domestic Product data loom.

Gold price: Four-hour chart

Trend: Further upside expected

-

23:03

EUR/USD finds a cushion around 1.1040, market mood turns cautious ahead of US GDP

- EUR/USD has gauged an intermediate cushion around 1.1040 after a corrective move from a fresh annual high.

- A statement from the First Republic Bank that the US government was reluctant to provide liquidity support dented market sentiment.

- Investors are divided about the pace of interest rate hike to be adopted by the ECB in its monetary policy meeting.

The EUR/USD pair is consolidating in a narrow area around 1.1040 in the early Asian session. The major currency pair witnessed some profit booking after printing a fresh annual high of 1.0966 in the New York session. Investors turned cautious as the focus shifted to United States Gross Domestic Product (GDP) (Q1) data.

Market sentiment was extremely positive as investors were cheering bumper earnings data from US technology stocks such as Microsoft and Meta Platforms, however, the statement from the First Republic Bank that the government was reluctant to provide liquidity support after its collapse diluted the confidence of investors in the US administration.

S&P500 futures ended Wednesday’s session on a weak note despite soaring chances of steady interest rate guidance from the Federal Reserve (Fed) for its May policy meeting after the release of downbeat US Durable Goods Orders data.

The US Dollar Index (DXY) showed a V-shape rally after dropping to near the crucial support of 101.00 as downbeat market sentiment improved the appeal for the greenback as a safe-haven. Going forward, investors will keep their focus on the preliminary US GDP (Q1) data. As per the consensus, the US economy has grown by 2.0% in the first quarter of CY2023 on an annualized basis lower than the former growth rate of 2.6%. The lower pace of growth will cement fears of economic slowdown.

On the Eurozone front, investors are divided about the pace of interest rate hike to be adopted by the European Central Bank (ECB) in its monetary policy meeting next week. The street believes that options of 25 and 50 basis points (bps) are open as the shortage of labor is consistently propelling inflationary pressures.

-

22:05

NZD/USD bears move to fresh cycle lows and eye the 0.6080s

- NZD/USD bears eye the 0.6080s and 0.6060s as potential structural points.

- The 0.6150s can be regarded as potential resistance.

NZD/USD is down by some 0.3% and fell from a high of 0.6148 to score a low of 0.6111 making fresh lows for the current downtrend as banking sector woes continue to weigh on high beta currencies.

First Republic Bank's shares sank more than 20%, hitting a fresh record low for the second day in a row, on a report that the US government was unwilling to engineer its rescue, after the lender reported plunging deposits earlier this week.

The bears have taken the market toward the 2023 low of 0.6085.´´Given the Kiwi’s outperformance against AUD but staggering underperformance against EUR and GBP, it seems clear that markets are lumping AUD and NZD in the same basket, with the former struggling after softer Consumer Price Index data yesterday, and the latter struggling after yawning trade deficit data yesterday,´´ analysts at ANZ Bank said. ´´High-interest rates are just not cutting it for the Kiwi, and instead markets seem focussed on the big picture: twin deficits, and generally shaky global risk sentiment.´´

Meanwhile, earlier in the month, the Reserve Bank of New Zealand surprised the market and hiked the OCR by 50bps to 5.25%. Analysts at TD Securities noted that upside risks to inflation have been nudged higher in the near term above Feb MPS forecasts, overriding downside risks to growth.

´´Credit conditions not tightening sufficiently played a key role in the Bank's decision to hike 50bps,´´ they said, adding:

´´We discussed the potential of lowering our RBNZ terminal forecast in our Preview. However, after today's decision we retain our 5.50% peak OCR call. We see limited read-through of today's RBNZ decision for other Central Banks.´´

NZD/USD technical analysis

The market is on the front side of the bearish trend and remains biased to the downside while below 0.6190. The M-formation will possibly hold up the bear, however, and a correction could be on the cards over the coming week or two. The 0.6080s and 0.6060s are structural points that could come under pressure. The 0.6150s can be regarded as potential resistance.

-

22:01

Forex Today: A mixed US Dollar and cautious markets before crucial US data

During the Asian session, in New Zealand the ANZ's Business Outlook survey is due and in Australia, the Import and Export Price Index. Markets await critical Eurozone and US economic data ahead of central bank meetings.

Here is what you need to know on Thursday, April 27:

Wall Street slipped again on Thursday amid banking concerns and a gloomy outlook. First Republic Bank tumbled again. Investors continue to digest the latest earnings results. The earning season continues on Thursday with Amazon, Mastercard, Merck, T-Mobile, Intel, Honeywell, Activision Blizzard, American Airlines and Hertz.

On Thursday, the US will report the first estimate of Q1 GDP growth, which includes the Core Personal Consumption Expenditure Index, an inflation measure closely watched by Fed officials. Analysts at Wells Fargo warn that growth numbers could come significantly below consensus.

A revision to prior retail sales data published this week is a potential game-changer. If our interpretation of the latest revisions is correct, then real GDP growth for Q1-2023, which will be reported on Thursday morning, could come in at half the growth rate that is presently expected by the consensus

Other reports due in the US on Thursday include Jobless Claims, Kansas Fed Manufacturing Activity and Pending Home Sales. However, this number could be offset by inflation and growth numbers ahead of next week’s FOMC meeting. A final 25 basis points rate hike is priced in.

The US Dollar Index dropped 0.40% on Wednesday and finished far from the lows. While the Greenback hit fresh 13-month lows versus the Euro, it reached monthly highs against the Aussie and the Kiwi. Commodity currencies were hit by risk sentiment. Next week, the Fed will have its monetary policy. Markets see a final 25 basis point rate hike, but expectations have eased up a bit following renewed banking concerns. US consumer inflation will be critical for Fed’s forecast.

US Core PCE Preview: Why this is a lose-lose situation for the US Dollar

The Euro outperformed on Wednesday, amid rising odds (still low) of a 50 basis points rate hike from the European Central Bank next week. Germany, Spain and France will release inflation data on Friday, alongside Eurozone Q1 GDP. EUR/USD climbed to 1.1094, reaching the highest intraday level since March 2022 and then pulled back trimming gains.

USD/JPY ended flat around 133.60 amid relatively steady bond yields and a mixed Dollar. On Thursday, the two-day monetary policy meeting kicks off at the Bank of Japan, the first one under Kazuo Ueda. No change is expected.

Inflation slowed further during the first quarter in Australia, cementing the case for the Reserve Bank of Australia (RBA) to stay on hold next week. AUD/USD dropped again, reaching monthly lows under 0.6600. NZD/USD continued to move slowly toward 0.6100 and March lows. The ANZ's Business Outlook survey is due on Thursday. USD/CAD rose marginally, holding above 1.3600.

Metals remained sideways. Gold ended lower at $1,988 after hitting a weekly high at $2,009; while Silver slipped below $25.00. Crude oil prices lost more than 3%; WTI fell to $74.50, erasing April’s gains.

Like this article? Help us with some feedback by answering this survey:

Rate this content -

22:00

South Korea BOK Manufacturing BSI in line with expectations (68) in May

-

21:26

USD/CAD climbs as BoC maintains status quo; risk-off sentiment lingers

- USD/CAD remains positive in the day after piercing to fresh weekly highs.

- USD/CAD rallies as safe-haven demand boosts US dollar amid economic concerns.

- BoC’s minutes assure no rate cuts are expected in 2023 but leaves room for potential adjustments if necessary

The USDCAD prints a fresh four-week high at 1.3651 after the Bank of Canada (BoC) revealed its latest monetary policy minutes, which were perceived as neutral. However, a risk-off impulse and falling oil prices undermined the Canadian Dollar (CAD), a tailwind for the USD/CAD. At the time of writing, the USD/CAD is trading at 1.3642.

USD/CAD climbs as sentiment deteriorates and falling oil prices undermine the CAD

Sentiment remains fragile, as shown by US equities. The latest Atlanta Fed GDPNOW, a model that estimates GDP in the US, came at 1.1%, vs. a prior’s estimate of 2.5%, for Q1 2023. The report flashed a slowdown in the US economy, sparking demand for safe-haven assets and underpinning the US Dollar (USD) to the detriment of the CAD. Additionally, oil prices, mainly WTI, is falling off the cliff at $74.24 per barrel, down 3.70%.

The latest minutes of the Bank of Canada (BoC) revealed discussions about hiking rates in April or waiting for more evidence. However, the Governing Council (GC) noted that inflation was declining, aligned with the BoC’s forecasts. Moreover, it signaled that no rate cuts are expected in 2023, and the bank will act if higher rates are needed.

Aside from this, the US economic docket revealed Durable Good Orders for March exceeded estimates and rose 3.2% MoM, above the last month’s reading. Excluding transportation, the so-called core Orders climbed 0.3%, above forecasts.

US Treasury bond yields were gaining ground and helped the greenback to bounce from two-week lows, reaching 101.013, according to the US Dollar Index (DXY). The DXY sits at 101.468, down 0.37%.

Therefore, the USD/CAD soared and hit a new two-day high at 1.3651, and as long as it persists above 1.3600, a test to 1.3700 is on the cards.

USD/CAD Key Technical Levels

-

21:05

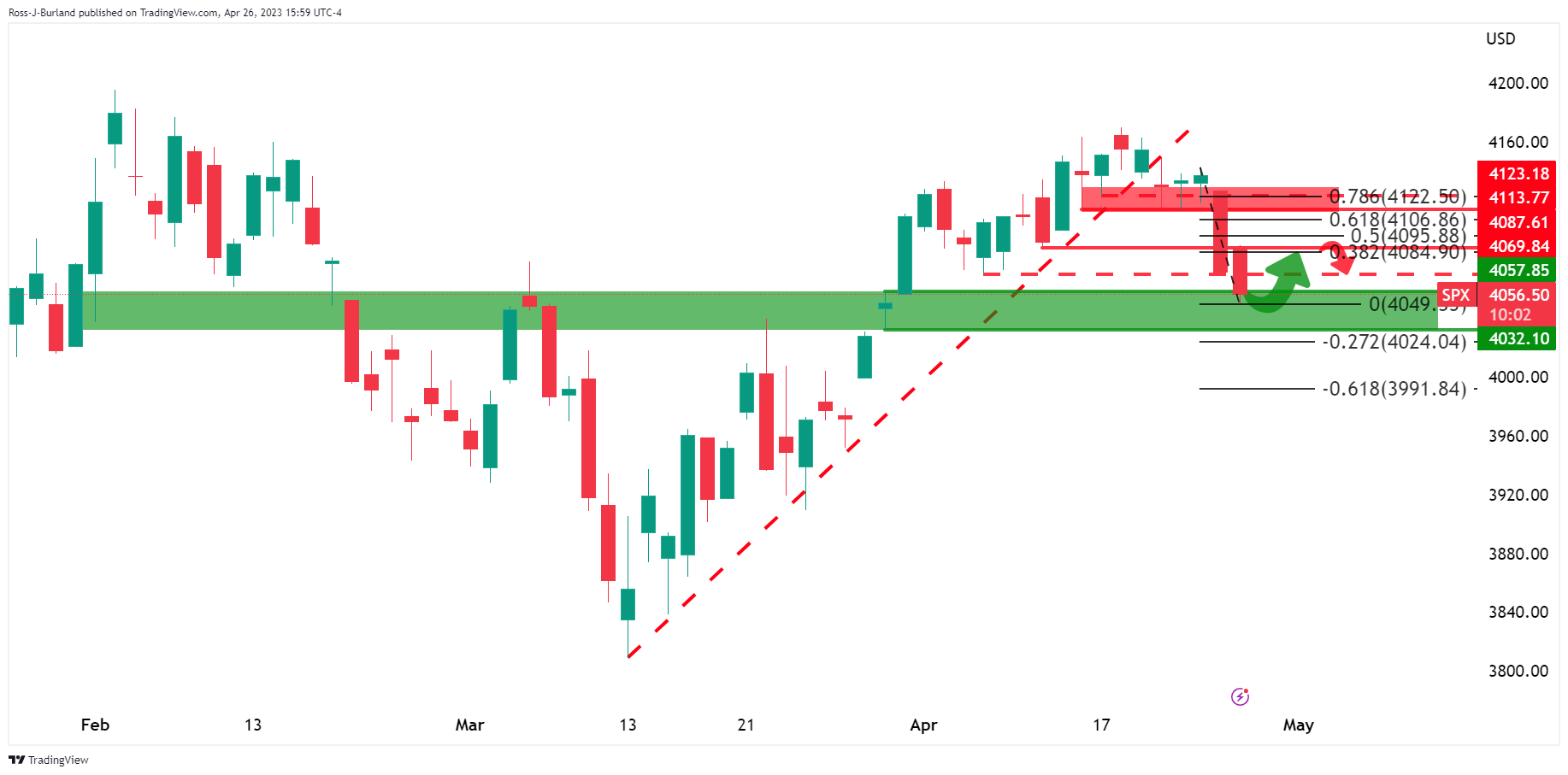

S&P 500 bears in control following break of structure amid banking sector woes

- S&P 500 index is moving into what could be a support area after breaking the structure of 4,069.

- The market will remain biased to the downside while below the 78.6% Fibonacci level and on the backside of the prior bullish trendline.

the S&P 500 dropped again on Wednesday and took out structure on the daily chart at 4,069 to print a low of 4,049.35 so far at the time of writing. The market remains offered towards the close and bears have been motivated by bank stocks which remained under pressure.

´´Support from tech stocks following Q1 earnings from Google’s parent Alphabet Inc. and Microsoft Corp. beating expectations was offset by a further 20% fall in First Republic Bank,´´ analysts at ANZ Bank explained.

First Republic Bank's shares sank more than 20%, hitting a fresh record low for the second day in a row, on a report that the US government was unwilling to engineer its rescue, after the lender reported plunging deposits earlier this week.

Analysts at ANZ bank explained that ´´the latest survey of US community banks showed that expectations of tighter regulation are now their biggest concern. If smaller banks in the US are to be regulated more tightly, that could precipitate a keener focus on bank asset quality, which amid high inflation and expected slower growth, could underpin more cautious lending behavior.´´

The analysts added that ´´it will take time to observe how behaviors are changing and the impact that can have on credit provision, but the ongoing concerns over the future of First Republic are continuing to unsettle risk.´´

Still, analysts are expecting a 3.2% contraction in first-quarter profit for S&P 500 companies compared with expectations for a 3.9% decline just a day ago, Reuters reported.

´´Of the 163 S&P 500 companies that reported first-quarter profit through Wednesday, 79.8% topped analysts' expectations, as per Refinitiv IBES data. In a typical quarter, 66% of companies beat estimates.´´

Meanwhile, the Federal Reserve's monetary policy decision on May 3 is coming up and traders will be on the lookout for clues on policymakers' next steps regarding interest rates. Traders have priced in a 79% chance of the U.S. central bank hiking rates by 25 basis points next week, as per CMEGroup's Fedwatch tool.

Elsewhere, ´´the US House of Representatives could vote as early as Wednesday on a bill that sharply cuts spending for a decade in exchange for a short-term hike in the debt ceiling, though it was unclear if it had enough support in the Republican majority to pass,´´ Reuters reported.

S&P 500 technical analysis

The daily chart shows the index moving into what could be a support area after breaking the structure of 4,069. A move back to 4,080s could be on the cards but the market will remain biased to the downside while below the 78.6% Fibonacci level and on the backside of the prior bullish trendline.

-

20:18

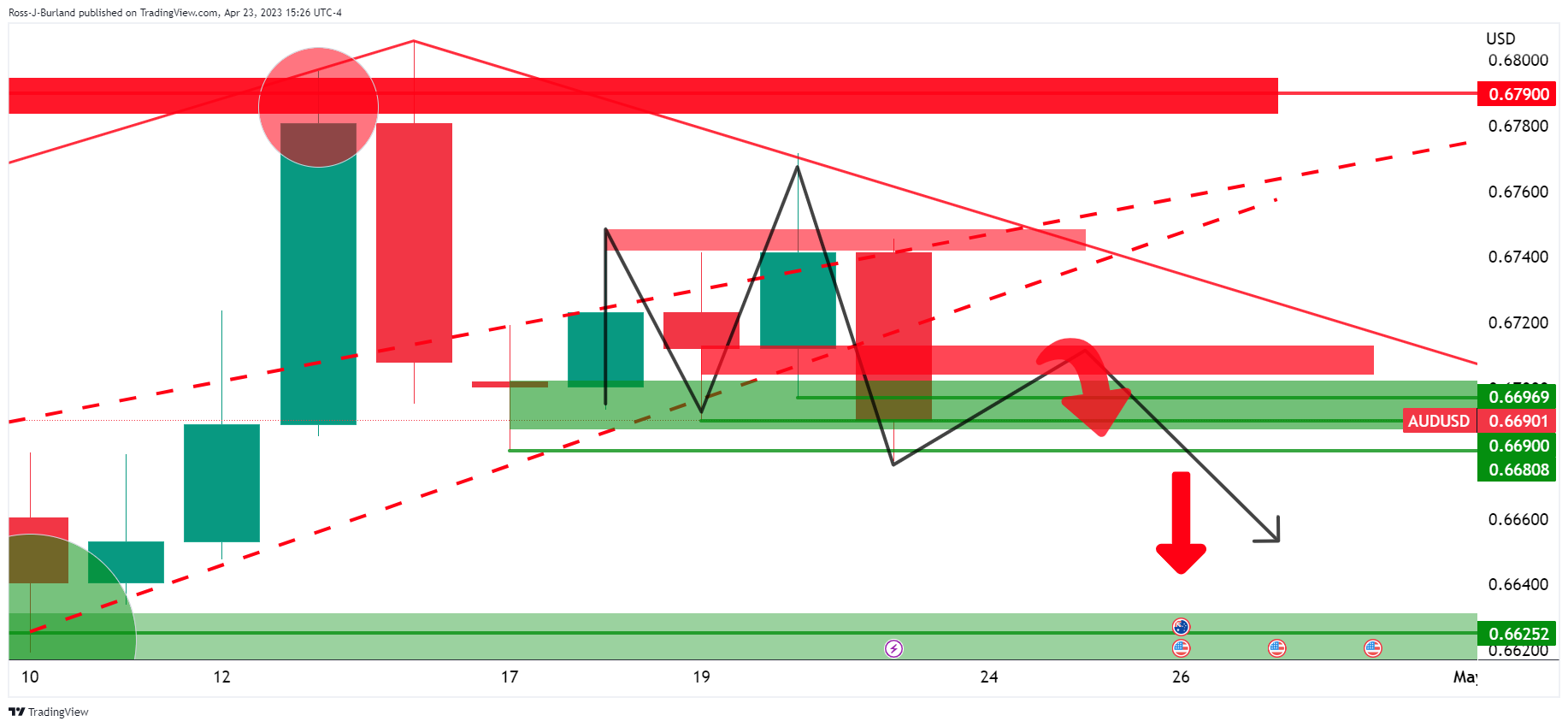

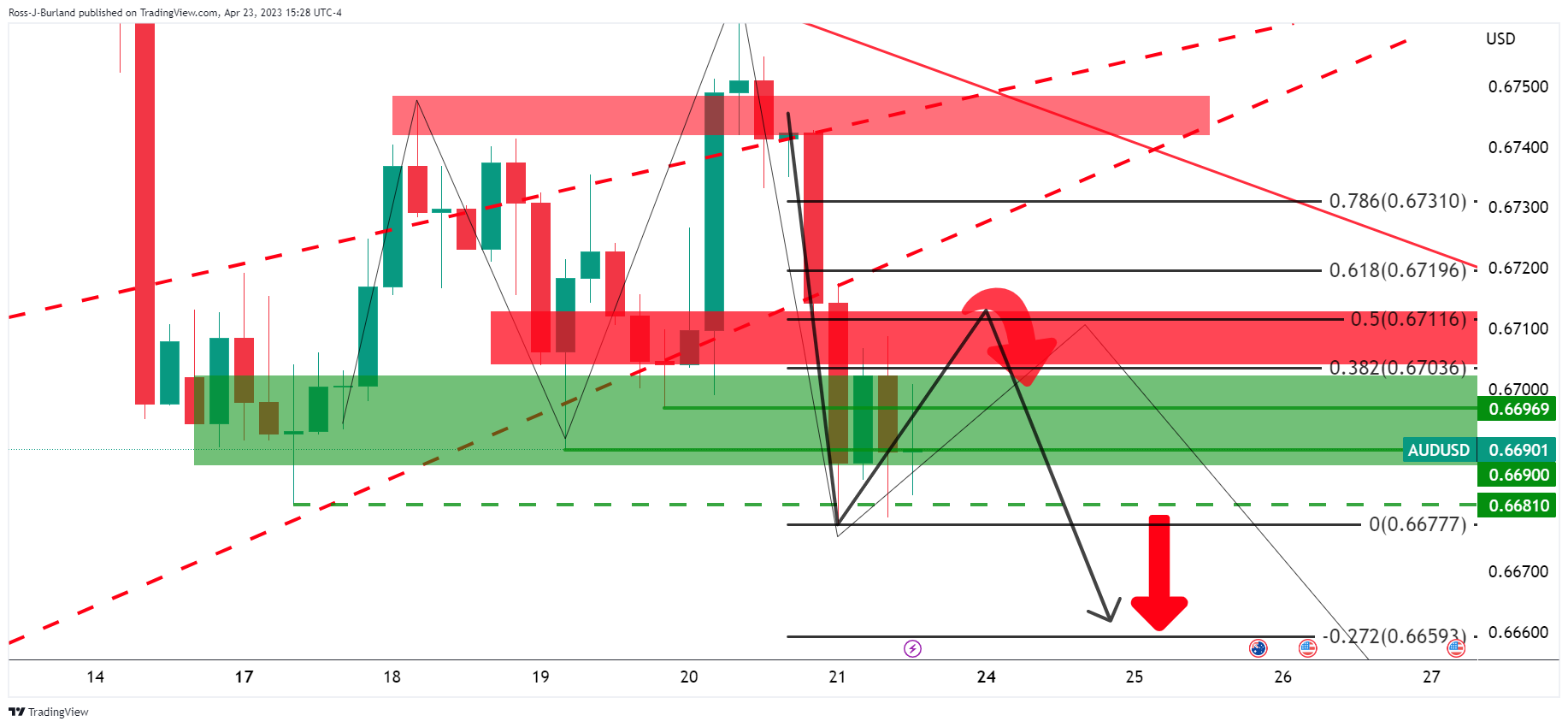

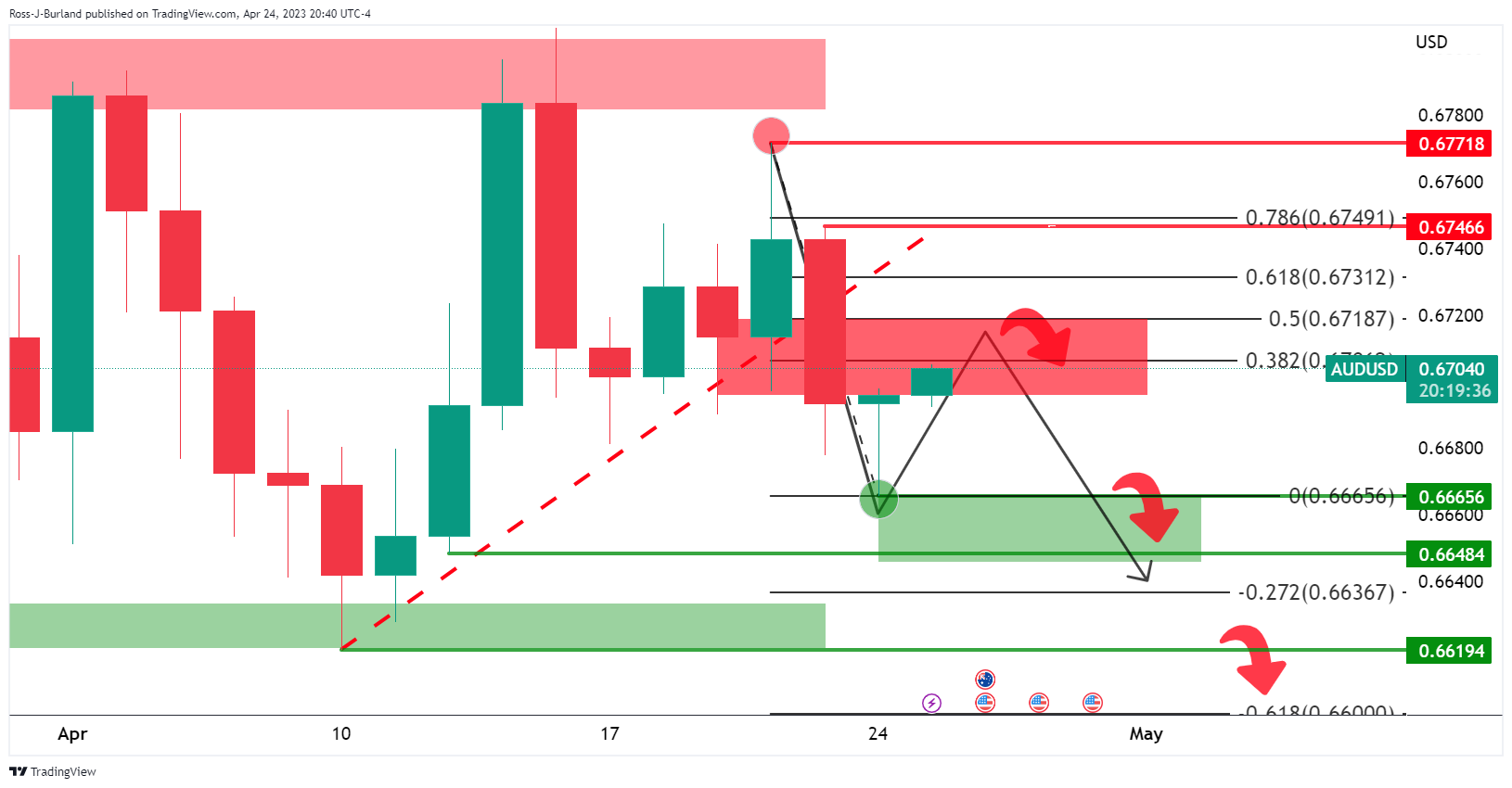

AUD/USD Price Analysis: Bulls could be lurking at the fresh cycle lows but continuaiton not off the table

- AUD/USD bulls could start to show up.

- There will be prospects of a correction into prior support near the 38.2% Fibonacci.

- The 50% mean reversion aligns with the round 0.6650 number also.

As per the prior analysis, AUD/USD Price Analysis: Bears aligned below 0.6710, and AUD/USD Price Analysis: Where are the bears hibernating? where the following illustrated the downside prospects while below 0.6710, we have seen a strong continuation move into 0.6591 today´s low.

AUD/USD prior analysis

The M-formation on the daily chart was expected to act as the peak formation in a correction and lead to a move lower to break the structure on the downside.

AUD/USD H4 chart

The four-hour chart´s 50% mean reversion level near 0.6710 aligned with the neckline of the pattern that could continue to act as resistance.

The price deteriorated but there had been a lack of momentum in the US Dollar and AUD/USD climbed back into the barroom brawl as follows:

In the bearish thrust, there was a break in structure which left the bias to the downside so long as the bears showed up and guarded the 0.67s.

However, there was an adjustment to the daily chart´s Fibonaccis as follows:

AUD/USD update

The 38.2% Fibonacci acted as resistance and we got a strong bearish impulse from there to test 0.6600 and the -61.8% Fibo.

There are long positions from below 0.6590 and 0.6560 that could see the market move into and further out:

... there is a lot of downside potential below. However...

If the bulls step in, then there will be prospects of a correction into prior support near the 38.2% Fibonacci. The 50% mean reversion aligns with the round 0.6650 number also.

-

20:03

First Republic Banks faces potential curb in Fed’s borrowing; Dow Jones extends losses

“US bank regulators are weighing the prospect of downgrading their private assessments of First Republic Bank — a move that may curb the troubled firm’s access to Federal Reserve lending facilities”, reported Bloomberg.

“The Federal Deposit Insurance Corporation (FDIC) has been giving the bank time to reach a private deal to shore up its finances (…) senior officials are increasingly weighing whether to downgrade their scoring of the firm’s condition (…) that would likely limit the bank’s use of the Fed’s discount window and an emergency facility launched last month”, said Bloomberg.

Market reaction

Wall Street indexes printed fresh lows. The Dow Jones is falling 0.70% and the S&P 500 drops 0.46% while the Nasdaq gains 0.45%. First Republic Bank shares are falling 30% on Wednesday at $5.78. Two months ago, it was trading at 121.00.

-

19:51

Gold Price Forecast: XAU/USD falls below 20-Day EMA as Gold price surrenders to US bond yields rise

- Gold price lost its bright as the US 10-year Treasury bond yield recovers lost ground, eyeing 3.45%.

- US Durable Goods Orders soar in March, surpassing estimates, while Core Orders (excl. transport) edge up.

- Gold Price Analysis: XAU/USD shows bearish signs as it stays below the 20-day EMA, and RSI accelerates a downtrend.

Gold price retreats after hitting a weekly high of $2009.34, drops as an uptick in US Treasury bond yields weighed on the yellow metal price. Though the XAU/USD dived below the 20-day Exponential Moving Average (EMA), a weak US Dollar (USD) capped its fall. The XAU/USD is trading at $1987, down 0.50%.

Gold price dulls amidst rising US bond yields and bearish XAU/USD signals

OF late, market sentiment shifted sour, as Wall Street’s turned negative, except for the Nasdaq. US economic data revealed in the day, namely Durable Good Orders surprisingly jumped by 3.2% MoM in March, exceeding estimates of 0.7%. Core Durable Good Orders, which exclude Transports, edged up 0.3% MoM, compared to a contraction of -0.2% estimated by the consensus.

Aside from this, US regional bank woes continued to dent investors’ mood, while a bid in US Treasury bond yields undermined appetite for the XAU/USD. The US 10-year Treasury bond yield advances four basis points, at 3.447%, but remains well below the opening week levels of 3.568%.

In the meantime, expectations for a US Federal Reserve (Fed) 25 bps rate hike in May, diminished, with odds at 76.1%, below the previous week’s 83.3% chance.

Regarding US politics, later news, the Republican Debt ceiling bill advanced in the US House of Representatives toward a debate and a possible vote.

Meanwhile, recession fears in the United States increased, as the US Atlanta Fed GDPNow for Q1 stands at 1.1%, versus a previous reading of 2.5%, ahead of the release on Thursday of Advance GDP figures for Q1 2023.

Besides that, the US economic agenda will feature Initial Jobless Claims for the latest week, alongside Pending Home Sales and Friday’s release of the Fed’s preferred gauge for inflation, the core PCE.

XAU/USD Technical Analysis

From a technical perspective, some signs suggest the XAU/USD could test the $1950 area in the near term. Firstly, the XAU/USD stays below the 20-day EMA, which sits at $1988.65, not far from the current price, but a daily close below the former, is a signal of bearishness. Moreover, the Relative Strength Index (RSI) accelerated its downtrend and is about to cross below the 50-mid line. That said, further downward action is warranted.

Hence, the XAU/USD first support would be the latest couple of weeks’ low at $1969.34, followed by the February 2 high at $1959.74, before falling to the confluence of the figure and the 50-day EMA at $1950.

Conversely, if XAU/USD reclaims the 20-day EMA, further sideways action between the $1980-$2000 area is expected.

-

18:50

BoC’s Summary of Deliberations: Expectations for rate cuts later in 2023 are not the most likely scenario

The Bank of Canada's Summary of Deliberations from the April 12th meeting when it kept interest rate unchanged, showed they discussed hiking rates. The document notes that inflation was declining in line with BoC Governing Council estimates. Officials agreed that expectations for rate cuts later in 2023 are not the most likely scenario.

“Governing Council agreed that while the new economic projection was similar to January’s, there was a sense that the economy was proving a little stronger than expected,” said the summary. Members were concerned that the current pace of wage growth is not consistent with getting inflation back to 2% without a substantial increase in productivity.

Members agreed that it was important to continue to signal that the central bank is prepared to tighten policy further if needed.

Key quotes:

“Governing Council noted that while global economic growth remained subdued, it was again coming in stronger than expected, particularly in the euro area and the United States.”

“Governing Council assessed recent data and developments in Canada and judged them to be evolving broadly in line with their January projection. Headline inflation was coming down, and signs of a rebalancing of supply and demand were becoming evident. But Governing Council acknowledged that the labour market was still tight and the slowing in growth would likely come a little later.”

“Members of Governing Council revisited their concern that the current pace of wage growth, if sustained, would not be consistent with getting inflation back to 2% without a substantial increase in productivity (which has been declining in recent quarters).”

“Governing Council agreed that, overall, consumer spending is anticipated to be subdued in the second half of 2023 and into 2024 as the effects of the tightening in monetary policy work their way through the economy.”

“Governing Council was more confident that inflation in Canada would continue to fall in the coming months to around 3%, the second stage of disinflation all the way back to 2% could prove more difficult.”

“Members agreed that while a risk of a sharper slowdown remains, based on their current outlook, cutting rates later this year did not seem to be the most likely scenario.”

“The discussion around increasing the interest rate further focused on whether monetary policy was restrictive enough and whether it was best to raise the policy rate now or wait for more evidence.”

Market reaction

The USD/CAD pair dropped modestly after the minutes fell below 1.3620. It is flat for the day after surging on Tuesday from 1.3545 to 1.3647, reaching the highest level in a month.

-

18:39

GBP/USD bulls flush out shorts to test 1.25s

- GBP/USD bulls move into fresh daily highs testing bearish commitments in the 1.25s.

- A break of trendline support is eyed for the days ahead.

GBP/USD rallied on Wednesday to a fresh high of 1.2515 on further signs of a US economic slowdown that has dented the US Dollar. Data this week has not been favorable for the Greenback and today´s orders for core capital goods slipping more than expected in March has weighed on the currency further.

The US Dollar index, DXY, which measures the currency against six major rivals, dropped to a low of 101.013 as new orders for key U.S.-manufactured capital goods fell more than expected last month. Shipments also fell suggesting that business spending on equipment was likely a drag on economic growth while investors await the Gross Domestic Product numbers. All in all, driving the US Dollar versus other major currencies has been early signs of a US slowdown and decelerating inflation.

Meanwhile and domestically, investors are pricing in rate hikes from the Bank of England that will push up Bank Rate to around 4.9% by September from 4.25% currently. Last week´s strong wage and Consumer Price Index data have shown that underlying inflation pressures are more persistent than previously expected. the CPI data in fact revealed Britain's inflation rate remained above the 10% mark for a seventh straight month in March.

For that, analysts at TD Securities said that they expect a final 25bps hike in June, bringing the BoE's terminal rate to 4.75% (was 4.50%). ´´Strong inflation data continues to weigh on GBP rates. We believe the hawkish price action supports entering longs in GBP on a cross-market basis.´´

However, the more recent data have painted a mixed picture of the country's economy. Data from the ONS showed that Retail Sales fell more than expected in March amid the rising cost of living and poor weather conditions. The latest Markit PMI survey suggested that Britain's Gross Domestic Product grew the most in a year in April.

GBP/USD technical analysis

The rally in GBP/USD has moved into the prior day´s shorts and has squeezed positions above yesterday´s highs. This could be a signal that the market is preparing to finally head lower as per the head and shoulders. However, a close above 1.2505 and then 1.2537, April 23 highs, will leave the bias in the hands of the bulls.

-

18:28

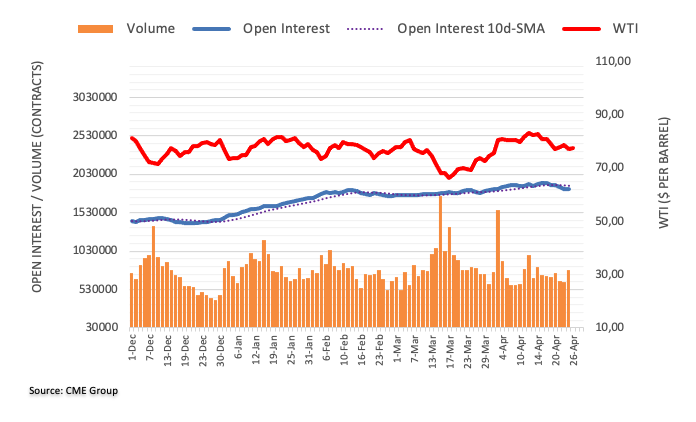

WTI is under pressure from rising US Dollar despite a dip in US oil inventories

- WTI bounced as US EIA revealed crude inventories dropped by 5.1 million barrels compared to the last week.

- Gasoline and distillates followed suit, though they did not underpin WTI’s price.

- WTI Price Analysis: Downward pressured by solid resistance around $77.24-$78.37.

Western Texas Intermediate (WTI), the US crude oil benchmark, trims some of its earlier losses that carried oil prices toward its weekly low at $75.69 per barrel. However, a late recovery in the US Dollar (USD) keeps WTI pressured, even though a report on US crude inventories falls more than expected, as data shows. At the time of writing, WTI is trading at $76.42 PB, down 1.21%.

On Wednesday, the US Energy Information Administration (EIA) revealed that crude inventories slid by 5.1 million barrels compared to last week, exceeding estimates of -1.5 million. The EIA informed that gasoline and distillates also declined by 2.4 million barrels and almost 600,000 barrels, respectively.

Following the release of the EIA’s report, WTI bounced off daily lows at around $75.60 PB toward the current price level.

Of note is that WTI prices had almost erased all of their gains after the Organization of the Petroleum Exporting Countries (OPEC) and its allies, known collectively as OPEC+, announced additional cuts to crude oil in early April.

WTI dived on Tuesday on concerns that additional rate hikes by global central banks could dent demand. The latest tranche of US economic data, particularly Federal Reserve’s (Fed) Regional Banks Manufacturing and Business activity indices, flashed an ongoing economic deceleration. Nevertheless, expectations for further tightening remain high, with most investors expecting a 25 bps rate hike by the Fed at the May 2-3 meeting.

Moreover, US consumer confidence deteriorated to a nine-month-low in April, as concerns mounted that the US economy may tip into a recession late in the year.

WTI Technical Analysis

After covering the $6.00 gap, WTI is attempting a recovery towards the $77.00 PB area but faces solid resistance upwards. The 50-day Exponential Moving Average (EMA), at $77.24, would be difficult to surpass, followed by the 20 and 100-day EMAs, at $78.10 and $78.37, respectively. On the flip side, a daily close below the March 31 high of $75.68 could pave the way for a fall toward the $74.00 area.

-

18:02

United States 5-Year Note Auction: 3.5% vs previous 3.665%

-

17:22

USD/MXN gains momentum as investors seek safety amidst US banking sector woes

- US Durable Good Orders exceeded forecasts, while Core advanced above estimates.

- Banxico’s Governor, Victoria Rodriguez Ceja, hints at a potential tightening cycle pause.

- USD/MXN maintains a downward trend with resistance at 18.1122, which, if cleared, expects further upside toward 18.3132.

USD/MXN advanced past the 20-day Exponential Moving Average (EMA) spurred by a risk-off impulse, as US banking sector woes reignited as First Republic Bank stock sank in Tuesday’s session. That said, outflows from the emerging market currency seeking safety moved to the US Dollar (USD). At the time of writing, the USD/MXN is trading at 18.1059, shy of the 20-day EMA.

Positive US economic data and Banxico’s hints of policy changes support USD/MXN

US equities are seesawing between gains and losses as tech companies reported earnings that exceeded estimates. However, bank crisis jitters in the US keep sentiment fragile. US economic data, namely Durable Good Orders for March, jumped by 3.2% MoM, exceeding estimates of 0.7%. Excluding transports, figures advance 0.3% MoM, above forecasts of -0.2%.

Even though risk appetite improved, as shown by the global equity markets, flows toward safety bolstered the USD/MXN. In addition, recent comments from the Bank of Mexico (Banxico’s) Governor Victoria Rodriguez Ceja suggest that Banxico could pause the tightening cycle. She said, “We will be evaluating in the next decision, on May 18, these factors and will be discussing whether it’s the moment to stop the increase in rates. We still have to have the discussion with the members of the board.”

Lately, inflation in Mexico for mid-April was reported at 6.24% YoY, below 6.52% in March, while Core dropped from 8.03% YoY in mid-March to 7.75%. The market is pricing that Banxico will hold rates unchanged for about six months before cutting 175 bps in the subsequent semester.

Given that central banks could diverge in the near term, with the Federal Reserve hiking rates and Banxico’s pausing, further upside in the USD/MXN is expected.

USD/MXN Technical Analysis

USD/MXN remains downward biased. However, buyers had remained resilient at around the 17.9000-18.0000 area but had failed to decisively break above the 20-day EMA at 18.1122, which would pave the way for further gains. If that scenario continues, the USD/MXN’s next resistance would be the 50-day EMA at 18.3132, ahead of challenging the April 5 cycle high at 18.4010. Conversely, expect further losses if USD/MXN dives below 18.0000.

-

17:01

Russia Industrial Output above expectations (-1.6%) in March: Actual (1.2%)

-

15:30

Breaking: EUR/USD hits a new 13-month high, approaches 1.1100

- EUR/USD rallied to a fresh multi-month high, nearby 1.1100.

- Fears around another round of a banking crisis in the US weighed on the odds for a Fed 25 bps rate hike.

The EUR/USD soars sharply above the past yearly high of 1.1076 and hits a 13-month high at around 1.1095. Concerns about the health of regional banks in the United States (US) triggered flows outside the US Dollar (USD), as shown by the US Dollar Index (DXY), collapsing 0.75%. At the time of writing, the EUR/USD is trading at 1.1067.

US Treasury bond yields, and the risks of a banking crisis in the US, the drivers of EUR/USD’s jump

As the North American session began, the EUR/USD achieved a daily high shy of the 1.1100 figure, as First Republic Bank, which took over Silicon Valley Bank (SVB), witnessed its shares plunge 49% on Tuesday, as deposits shrank. That sparked fears of a possible contagion and a potential pause on the US Federal Reserve (Fed) tightening cycle. Therefore, the greenback fell.

US Treasury bond yield dropping is one reason for the EUR/USD’s rise. Additionally, expectations for a US Federal Reserve 25 bps rate hike diminished to 75.3%, compared to 1 week 83.3%.

EUR/USD Market Reaction

The EUR/USD jumped from around the R1 daily pivot at 1.1040 and accelerated its uptrend towards the 1.1095 multi-month high, some pips of reaching the R1 daily pivot. Though it has retraced some 30 pips from the daily high, buyers are still in charge of the uptrend, and the 1.1100 figure is still in sight.

EUR/USD Technical Levels

-

15:30

United States EIA Crude Oil Stocks Change registered at -5.054M, below expectations (-1.486M) in April 21

-

15:26

US Durable Goods Orders: Not as good as the headline suggests – Wells Fargo

Data released on Wednesday in the US showed that Durable Goods Orders rose 3.2% in March surpassing expectations. Analysts at Wells Fargo point out the increase was due almost entirely to a surge in aircraft orders. They argue that private-sector core capital goods orders is what matters and are showing a continued reversal in demand.

Key quotes:

“Look through the headline durable goods data that suggest orders leaped 3.2% in March. The gain last month was due almost entirely to a pop in aircraft orders specifically after weakness in the first two months of the year. It's not unusual to get wide swings in aircraft orders month-to-month.”

“The trend in private-sector core orders has slowed and suggests the goods sector of the economy still appears to be going through correction as new demand slows amid increased economic uncertainty. Core durable goods orders (excluding defense and aircraft), slid 0.4% in March, marking the fifth decline in seven months.”

-

15:16

Gold Price Forecast: XAU/USD jumps to six-day highs near $2,010 and retreats

- A volatile session for Gold price that continues to move sideways.

- US Dollar weakens during the American session despite upbeat US data.

- US Treasury yields print fresh weekly lows ahead of next week’s FOMC meeting.

Gold price jumped at the beginning of the American session, rising from $1,995 to $2,009, reaching the highest level in six days and then pulled back to the $2,000 area. A weaker US Dollar and lower Treasury yields boosted XAU/USD.

Data from the US came in above expectation with Durable Goods Orders rising 3.2% in March, above the 0.8% of market consensus. Despite the upbeat numbers, the US Dollar weakened particularly against EUR, GBP and JPY.

The US 2-year Treasury yield is at 3.88%, the lowest level in three weeks while the 10-year stands at 3.90%. The US Dollar Index trades at 101.99 (weekly low), down 0.73% for the day.

The rally in XAU/USD is seen as vulnerable amid the lack of clear drivers. The chart is bullish but the price is unable to confirm a firm break of the current range. Volatility is set to remain elevated considering the incoming US data and next week’s FOMC meeting. On Thursday, the US will report the first estimate of Q1 GDP, including consumer inflation figures.

A consolidation above $2,005 would suggest more gains ahead, with the next strong resistance around $2,030. On the flip side, if the current retreat extends, support awaits at $1,990. The crucial level is $1,970.

-638181152725276974.png)

-

15:01

USD/JPY drops to 133.00 neighbourhood, over one-week low amid heavy USD selling

- USD/JPY drops to a nearly two-week low amid the heavily offered tone surrounding the USD.

- Speculations for an imminent Fed rate cut later this year continues to drag the USD lower.

- The BoJ’s dovish stance, a positive risk tone could undermine the JPY and lend some support.

The USD/JPY pair fades a modest intraday uptick to the 134.00 neighbourhood and drops to a one-and-half-week low during the early North American session. The pair is currently placed around the 133.15-133.10 region, down over 0.40% for the day, and is pressured by the heavily offered tone surrounding the US Dollar (USD).

In fact, the USD Index, which tracks the Greenback against a basket of currencies, reverses a major part of the overnight strong gains and is seen weighing on the USD/JPY pair lower. Fresh concerns about the regional banking sector crisis in the US, along with fears of an imminent recession and worries about the US debt ceiling, have been fueling speculations that the Federal Reserve (Fed) will cut interest rates later this year. This, in turn, continues to drag the US Treasury bond yields lower and exerts heavy downward pressure on the Greenback.

That said, the Bank of Japan (BoJ) Kazuo Ueda's dovish remarks earlier this week, along with a modest recovery in the US equity futures, could undermine the safe-haven Japanese Yen (JPY) and lend support to the USD/JPY pair. It is worth recalling that the new BoJ Governor said on Monday that the central bank must maintain monetary easing as trend inflation is still below 2% and added that inflation forecasts must be quite strong and close to 2% in the coming year to consider tweaking yield curve control. This, in turn, warrants caution for bearish traders.

Hence, any subsequent downfall is more likely to find decent support near the 133.00-132.90 region, representing a technically significant 100-day Simple Moving Average (SMA) support. The market focus now shifts to the release of the US Q1 GDP report on Thursday and the US Core PCE Price Index - the Fed's preferred inflation gauge on Friday. This, along with the highly-anticipated BoJ monetary policy meeting, should provide some meaningful impetus and help investors to determine the near-term trajectory for the USD/JPY pair.

Technical levels to watch

-

14:56

USD Index loses the grip and challenges 101.00

- The index accelerates losses and puts 101.00 to the test.

- US yields extend the leg lower across the curve on Wednesday.

- US Durable Goods Orders came in above expectations in March.

The USD Index (DXY), which tracks the Greenback vs. a basket of its main competitors, gathers further selling pressure and challenges the key support at the 101.00 region on Wednesday.

USD Index on the defensive on rising risk-on trade

The index drops to multi-day lows and revisits the 101.00 neighbourhood on the back of the acute bounce in the risk-associated assets, eroding at the same time the strong advance seen in the previous session.

No news from the macro scenario, where the recent resurgence of banking jitters sponsored the return of the risk aversion on Tuesday and propelled the index to the proximity of the 102.00 region.

In the meantime, investors continue to favour a 25 bps rate hike by the Fed at the May 3 event, although the probability of that outcome shrinks a tad to around 75% (from nearly 90% a day ago).

In the US data space, MBA Mortgage Applications rose 3.7% in the week to April 21, while Durable Goods Orders expanded at a monthly 3.2% in March and advanced figures saw the trade deficit shrinking to $84.6B also in March.

What to look for around USD

The U-turn in the index now opens the door to a deeper retracement, including a potential breakdown of the 101.00 level and a subsequent challenge of 2023 lows near 100.80.

Looking at the broader picture, the index continues to navigate in a consolidative phase against steady expectations of another rate increase in May by the Fed.

In favour of a pivot in the Fed’s hiking cycle following the May event appears the persevering disinflation and nascent weakness in some key fundamentals.

Key events in the US this week: MBA Mortgage Applications, Durable Goods Orders, Advanced Goods Trade Balance (Wednesday) – Flash Q1 GDP Growth Rate, Initial Jobless Claims, Pending Home Sales (Thursday) – PCE/Core PCE, Employment Cost, Personal Income, Personal Spending, Final Michigan Consumer Sentiment (Friday).

Eminent issues on the back boiler: Persistent debate over a soft/hard landing of the US economy. Terminal Interest rate near the peak vs. speculation of rate cuts in 2024. Fed’s pivot. Geopolitical effervescence vs. Russia and China. US-China trade conflict.

USD Index relevant levels

Now, the index is losing 0.79% at 101.04 and the breach of 100.78 (2023 low April 14) would open the door to 100.00 (psychological level) and finally 99.81 (weekly low April 21 2022). On the other hand, the next hurdle emerges at 102.80 (weekly high April 10) followed by 103.05 (monthly high April 3) and then 103.21 (55-day SMA).

-

14:29

NZD/USD bounces off its lowest level since March amid notable USD supply

- NZD/USD remains under some selling pressure for the second straight day.

- The downside seems cushioned amid the emergence of fresh USD selling.

- The upbeat US data fails to impress the USD bulls or provide any impetus.

The NZD/USD pair drifts lower for the second straight day on Wednesday and drops to its lowest level since March 10 during the early North American session. The pair, meanwhile, react little to the upbeat US macro data and bounces to the 0.6135-0.6140 region in the last hour amid the emergence of fresh US Dollar (USD) selling.

In fact, the USD Index, which tracks the Greenback against a basket of currencies, erases a major part of the overnight gains and turns out to be a key factor lending some support to the NZD/USD pair. A slight improvement in the global risk sentiment - as depicted by a goodish recovery in the US equity markets - is seen as a key factor weighing on the safe-haven buck. The USD bulls fail to gain any respite following the better-than-expected release of US Durable Goods Orders and a modest uptick in the US Treasury bond yields.

fresh concerns about the regional banking sector crisis in the US, along with the possibility of an imminent recession and worries about the US debt ceiling, have been fueling speculations that the Federal Reserve (Fed) will cut interest rates later this year. The Fed, however, is still expected to hike interest rates by 25 bps in May, which, along with fears about economic headwinds stemming from rising borrowing costs could help limit the downside for the USD. This, in turn, is seen as a key factor exerting pressure on the NZD/USD pair.

Bearish traders, meanwhile, might wait for a sustained break through the 0.6100 mark and some follow-through selling below the YTD low, around the 0.6085 region touched in March before placing fresh bets. The focus now shifts to the release of the US Q1 GDP report on Thursday and the US Core PCE Price Index - the Fed's preferred inflation gauge on Friday. This will play a key role in influencing the near-term USD price dynamics and help investors to determine the next leg of a directional move for the NZD/USD pair.

Technical levels to watch

-

14:11

RBA: Data suggests it will not raise the key rate next week – Commerzbank

Inflation data from Australia showed it continues to slow down. Next week, the Reserve Bank of Australia (RBA) will have its monetary policy meeting. Analysts at Commerzbank point out that inflation data suggest the central bank will not raise rates.

Key quotes:

“The Reserve Bank of Australia (RBA) can't really breathe a sigh of relief yet, but it can breathe a little. Inflation fell quite significantly in the first quarter, from 7.8% to 7.0%. The two measures of core inflation also fell noticeably to 6.6% and 5.8%. This is likely to confirm the RBA's expectation that inflation will gradually decline and that the interest rate pause earlier this month was justified.”

“The data suggest that the RBA will not raise the key rate next week either, but leave it at 3.60%. However, with (core) inflation still well above the 2-3% inflation target, it is likely to maintain the restrictive undertone in its statement and assure that it is ready to do more should it be necessary.”

“The market already expects that the interest rate cycle in Australia is over and that no more rate hikes will follow, but that the first rate cuts are on the agenda in the fall.”

-

13:52

GBP/USD sticks to gains near daily peak, comfortably above mid-1.2400s post-US data

- GBP/USD regains positive traction on Wednesday amid the emergence of fresh USD selling.

- A slight improvement in the global risk sentiment is seen weighing on the safe-haven buck.

- The upbeat US Durable Goods Orders fail to impress the USD bulls or provide any impetus.

The GBP/USD pair sticks to its strong intraday gains, around the 1.2465-1.2470 area through the early North American session and moves little in reaction to the US macro data.

The US Census Bureau reported this Wednesday that Durable Goods Orders in the US smashed market expectations by a big margin and increased by 3.2% in March. Excluding transportation, new orders increased 0.3% during the reported month as against consensus estimates pointing to a 0.2% fall and the 0.3% decline registered in March. The upbeat data, however, fails to impress the US Dollar (USD) bulls or provide any meaningful impetus to the GBP/USD pair.

Meanwhile, a slight improvement in the global risk sentiment - as depicted by a modest uptick in the US equity futures - is seen weighing on the safe-haven Greenback amid speculations for an imminent rate cut by the Federal Reserve (Fed) later this year. Apart from this, rising bets for another 25 bps interest rate hike by the Bank of England (BoE) in May continue to underpin the British Pound and remains supportive of the strong bid tone surrounding the GBP/USD pair.

That said, a modest uptick in the US Treasury bond yields might hold back bearish traders from placing aggressive bets around the USD and keep a lid on any further gains for the major, at least for the time being. Investors also seem reluctant and could move to the sidelines ahead of the US Q1 GDP report on Thursday. This will be followed by the release of the US Core PCE Price Index - the Fed preferred inflation gauge on Friday.

The data will play a key role in influencing the near-term USD price dynamics and should provide some meaningful impetus to the GBP/USD pair. Nevertheless, the intraday positive move assists spot prices to reverse a major part of the previous day's retracement slide from over a one-week high - levels just above the 1.2500 psychological mark - and is exclusively sponsored by the prevalent USD selling bias.

Technical levels to watch

-

13:35

US: Durable Goods Orders rise by 3.2% in March vs. 0.8% expected

- Durable Goods Orders in the US rose at a much stronger pace than expected in March.

- US Dollar Index stays deep in negative territory below 101.50.

Durable Goods Orders in the US increased by 3.2%, or $8.6 billion, in March to $276.4 billion, the US Census Bureau announced on Wednesday. This reading followed February's contraction of 1.2% (revised from -1%) and surpassed the market expectation for an increase of 0.8% by a wide margin.

"Excluding transportation, new orders increased 0.3%," the publication further read. "Excluding defense, new orders increased 3.5%. Transportation equipment, also up following two consecutive monthly decreases, led the increase, $8.1 billion or 9.1% to $97.4 billion."

Market reaction

The US Dollar stays under pressure despite the upbeat data and the US Dollar Index was last seen losing 0.5% on the day at 101.35.

-

13:31

United States Goods Trade Balance came in at $-84.6B, above expectations ($-89B) in March

-

13:31

United States Wholesale Inventories came in at 0.1%, below expectations (0.2%) in March

-

13:30

United States Durable Goods Orders ex Transportation came in at 0.3%, above expectations (-0.2%) in March

-

13:30

United States Durable Goods Orders above forecasts (0.8%) in March: Actual (3.2%)

-

13:30

EUR/USD Price Analysis: Immediately to the upside comes the YTD high

- EUR/USD regains upside traction and advances past 1.1000.

- Bulls continue to target the 2023 peak at 1.1075.

EUR/USD leaves behind Tuesday’s pronounced decline and reclaims the area beyond 1.1000 the figure on Wednesday.

The pair looks poised to extend the recovery further in the near term. That said, the immediate hurdle is expected at the 2023 high at 1.1075 (April 14) seconded by the round level at 1.1100.

Looking at the longer run, the constructive view remains unchanged while above the 200-day SMA, today at 1.0404.

EUR/USD daily chart

-

13:30

United States Durable Goods Orders ex Defense above forecasts (0%) in March: Actual (3.5%)

-

13:00

Brazil Mid-month Inflation registered at 0.57% above expectations (0.53%) in April

-

12:21

Dollar soft as risk sentiment improves – BBH

Strong earnings reports from the big tech companies last night have helped improve market sentiment and weigh on the US Dollar, write Economists at BBH. DXY is trading lower near 101.269 and has given back nearly all of yesterday’s gains.

Key quotes:

“WIRP suggests over 80% odds of 25 bp hike at the May 2-3 meeting, down from 90% at the start of this week and back to the 80% seen at the start of last week and 70% at the start of the week before that. We believe a hike next week is a done deal. There are no longer any odds of another 25 bp hike in June, down from about 15% at the start of this week. Between the May 2-3 and June 13-14 meetings, the Fed will have digested two more job reports, two CPI/PPI reports, and one retail sales report. At this point, a pause in June might just be the most likely outcome but it really will depend on how all that data come in. After all that, two cuts are now priced in by year-end vs. one at the start of this week and back to two seen at the start of last week. In that regard, Powell has said that Fed officials “just don’t see” any rate cuts this year. We concur.”

-

12:17

USD Index Price Analysis: No changes to the consolidative theme

- DXY comes under pressure amidst choppy price action this week.

- The loss of 101.00 could open the door to a probable test of the YTD low.

DXY fades part of Tuesday’s acute rebound and return to the 101.40/50 region on Wednesday.

The recent choppy performance in the index seems to have now refocused back on the downside. Against that, DXY could cling to this consolidative theme ahead of a probable drop to the 101.00 zone. The loss of the latter could expose a move to the so far 2023 lows near 100.80 (April 14).

Looking at the broader picture, while below the 200-day SMA, today at 106.12, the outlook for the index is expected to remain negative.

DXY daily chart

-

12:17

When are the US Durable Goods Orders and how could they affect EUR/USD?

US Durable Goods Orders Overview

The US Census Bureau will publish the monthly Durable Goods Orders data for March later during the early North American session this Wednesday, at 12:30 GMT. The report is expected to show that headline orders rose by 0.8% during the reported month as compared to the 1% fall reported in February. Orders excluding transportation items, which tend to have a broader impact, are anticipated to register a modest 0.2% decline in March.

How could it affect EUR/USD?

Ahead of the key macro data, the emergence of fresh selling around the US Dollar (USD) lifts the EUR/USD pair back above the 1.1050 level, closer to a one-year high touched earlier this month. A weaker US Durable Goods Orders data will add to worries about a deeper economic downturn and reaffirm market expectations for an imminent interest rate cut by the Federal Reserve (Fed) later this year. This, in turn, could lead to a further decline in the US Treasury bond yields and weigh heavily on the buck, pacing the way for a further intraday appreciating move for the major.

In contrast, the market reaction to stronger US macro data is likely to be short-lived and do little to provide any respite to the USD bulls. Traders might prefer to wait on the sidelines ahead of the release of the Advance Q1 GDP report on Thursday and the US Core PCE Price Index - the Fed's preferred inflation gauge on Friday. This, in turn, suggests that the path of least resistance for the EUR/USD pair is to the downside and any intraday pullback might still be seen as a buying opportunity.

Eren Sengezer, Editor at FXStreet, offers a brief technical outlook for the EUR/USD pair and writes: “The 100-period Simple Moving Average on the four-hour chart at 1.0960 stays intact following Tuesday's pullback, highlighting buyers' willingness to continue to defend this level. The Fibonacci 23.6% retracement level of the latest uptrend is also located slightly below that level at 1.0950 to reinforce that support. Additionally, the Relative Strength Index (RSI) indicator recovered back above 50, confirming the bullish tilt in the short-term outlook.”

Eren also outlines important technical levels to trade the EUR/USD pair: “On the upside, 1.1050 (static level) could be seen as the next bullish target before 1.1075 (end-point of the latest uptrend) and 1.1100 (psychological level).”

“1.1000 (psychological level, static level) aligns as interim support before 1.0960/50. A four-hour close below the latter could cause technical sellers to come into play and drag the pair lower toward 1.0900,” Eren adds further.

Key Notes

• EUR/USD Forecast: Buyers manage to keep Euro above key support

• EUR/USD regains the smile and the 1.1000 barrier

• EUR/USD looks side-lined for the time being – UOB

About US durable goods orders

The Durable Goods Orders, released by the US Census Bureau, measures the cost of orders received by manufacturers for durable goods, which means goods planned to last for three years or more, such as motor vehicles and appliances. As those durable products often involve large investments they are sensitive to the US economic situation. The final figure shows the state of US production activity. Generally speaking, a high reading is bullish for the USD.

-

12:13

EUR/JPY Price Analysis: Target remains at 148.00 and above

- EUR/JPY regains some balance following Tuesday’s pullback.

- Further recovery should retest the 148.00 barrier in the near term.

EUR/JPY resumes the uptrend and leaves behind part of Tuesday’s pronounced pullback to weekly lows near 146.30.

The underlying strong upside momentum in the cross appears so far unabated. Against that, the surpass of the 148.00 hurdle should put a potential test of the 2023 peak at 148.63 (April 25) back on the radar.

Further north, the cross could embark on further gains and attempt a visit to the key 150.00 mark.

So far, further upside looks favoured while the cross trades above the 200-day SMA, today at 142.34.

EUR/JPY daily chart

-

12:01

South Korea: Technical recession avoided – UOB

UOB Group’s Economist Ho Woei Chen reviews the latest GDP figures in South Korea.

Key Takeaways

“South Korea’s advance 1Q23 GDP growth was in line with expectations at 0.8% y/y, 0.3% q/q SA. The sequential rebound in GDP meant that South Korea’s economy avoided a technical recession.”

“The q/q expansion was due to stronger private consumption as well as goods exports that were led by motor vehicle shipments even as electronics had remained in a downcycle. This mitigated declines in facilities investment and services exports in 1Q23.”

“We maintain our cautious outlook for South Korea’s growth in 2023 at 1.3% (2022: 2.6%) with lackluster forecasts of 0.8% y/y in 2Q23 and 1.0% y/y in 3Q23 before a recovery to 2.5% y/y in 4Q23.”

“We continue to expect the BOK to remain on hold at 3.50% for the rest of 2023.”

-

12:00

United States MBA Mortgage Applications: 3.7% (April 21) vs -8.8%

-

11:50

USD/CAD oscillates in a range around 1.3620 area, just below a nearly one-month high

- USD/CAD consolidates its recent strong gains to a nearly one-month high touched on Tuesday.

- A modest recovery in Oil prices underpins the Loonie and caps the pair amid fresh USD selling.

- Rebounding US bond yields lend some support to the Greenback and help limit the downside.

The USD/CAD pair enters a bullish consolidation phase on Wednesday and oscillates in a narrow trading band through the first half of the European session. The pair is currently placed in neutral territory, around the 1.3620 region, just below a nearly one-month high touched the previous day.

Crude Oil prices gain some positive traction and reverses a part of Tuesday's slide to a fresh monthly low amid reports of falling US fuel inventories, which pointed to robust demand in the world's top consumer. This, in turn, underpins the commodity-linked Loonie and acts as a headwind for the USD/CAD pair amid the emergence of fresh US Dollar (USD) selling.

The intraday USD downtick could be attributed to the recent slump in the US Treasury bond yields amid fresh concerns about the regional banking sector. In fact, the yield on the benchmark 10-year US government bond registered its largest decline since March after the First Republic Bank reported a more than $100 billion plunge in deposits during the first quarter.

The Conference Board's Consumer Confidence Index unexpectedly dropped to a nine-month low in April and fueled worries about a deeper economic downturn. This, in turn, lifted bets for an imminent rate cut by the Federal Reserve (Fed) later this year, which dragged longer-duration Treasury yields lower across the board and is seen weighing on the Greenback.

Apart from this, signs of stability in the equity markets turn out to be another factor weighing on the safe-haven buck and contributing to capping the upside for the USD/CAD pair, at least for the time being. The Fed, however, is still expected to deliver a 25 bps rate hike in May, which acts as a tailwind for the US bond yields and lends support to the USD.

The aforementioned fundamental backdrop favours bulls and suggests that the path of least resistance for spot prices is to the upside. Traders, however, seem reluctant and move to the sidelines ahead of this week's key US macro releases, including the Advance Q1 GDP on Thursday and the Core PCE Price Index - the Fed's preferred inflation gauge on Friday.

In the meantime, traders on Thursday will take cues from the release of the US Durable Goods Orders data, due later during the early North American session. The data might influence the USD and provide some impetus to the USD/CAD pair. Apart from this, Oil price dynamics might further contribute to producing short-term opportunities around the major.

Technical levels to watch

-

11:06

Gold Price Forecast: XAU/USD lacks firm intraday direction, stuck in a range around $2,000

- Gold price oscillates in a narrow band and is influenced by a combination of diverging factors.

- The emergence of fresh US Dollar selling is seen as a key factor lending support to the XAU/USD.

- Bets for another 25 bps rate hike by the Federal Reserve in May act as a headwind for the metal.

Gold price struggles to capitalize on its gains recorded over the past two sessions and seesaws between tepid gains/minor losses on Wednesday. The XAU/USD holds steady around the $2,000 psychological mark through the first half of the European session and is influenced by a combination of diverging forces.

Fresh US Dollar selling lends support to Gold price

The US Dollar (USD) comes under renewed selling pressure and erodes a major part of the overnight gains amid the uncertainty over the Federal Reserve's (Fed) rate-hike path. This, in turn, is seen lending support to the US Dollar-denominated Gold prices. Fresh concerns about the regional banking sector crisis, the possibility of an imminent recession and worries about the debt ceiling in the United States (US) lift bets for an imminent rate cut by the Fed later this year. This led to the overnight slum in the US Treasury bond yields and continues to act as a headwind for the Greenback.

Federal Reserve rate hike bets cap XAU/USD

It is worth recalling that the yield on the benchmark 10-year Treasury yields registered its largest decline since March. That said, the US central bank is still expected to deliver a 25 bps rate hike at the next Federal Open Market Committee (FOMC) monetary policy meeting in May. This, in turn, allows the US bond yields to stage a modest recovery on Wednesday and keeps a lid on any meaningful upside for the non-yielding Gold price. Apart from this, signs of stability in the equity markets further contribute to caping gains for the safe-haven precious metal, at least for the time being.

Traders now eye macro data from United States for fresh impetus

The aforementioned fundamental backdrop makes it prudent to wait for strong follow-through buying before confirming that the Gold price has formed a near-term bottom around the $1,970 area and positioning for any further gains. Market participants now look forward to the US economic docket, featuring the release of the Durable Goods Orders data later during the early North American session. This, along with the US bond yields, might influence the USD price dynamics. Apart from this, the broader risk sentiment might provide some impetus to the Gold price.

Focus remains on US Q1 GDP and US PCE Price Index

The focus, however, remains glued to the release of the first-quarter US Gross domestic product (GDP) report on Thursday. This will be followed by the US Core Personal Consumption Expenditure (PCE) Price Index - the Fed's preferred inflation gauge - on Friday, which will help determine the near-term trajectory for the Greenback and the Gold price. In the meantime, the XAU/USD is more likely to extend its sideways consolidative price moves and remain confined in a familiar trading band held over the past one-and-half-weeks or so.

Gold price technical outlook

From a technical perspective, any subsequent move up is likely to confront stiff resistance near the $2,010 area. A sustained move beyond might trigger a fresh bout of a short-covering and lift Gold price beyond the $2,020 hurdle, towards the $2,040 horizontal zone en route to the YTD peak, around the $2,047-$2,049 region.

On the flip side, the $1,980 level, followed by the $1,969 region might continue to act as immediate support levels. Some follow-through selling will be seen as a fresh trigger for bearish traders and drag Gold price towards the next relevant support near the $1,956-$1,955 area. The XAU/USD could eventually drop to the monthly low around the $1,950 region.

Key levels to watch

-

10:32

South Africa Producer Price Index (MoM) registered at 1% above expectations (0%) in March

-

10:30

South Africa Producer Price Index (MoM) meets forecasts (0%) in March

-

10:30

South Africa Producer Price Index (YoY) registered at 10.6% above expectations (10.4%) in March

-

10:27

USD/CNH: Upside faces a solid resistance at 6.9650 – UOB

Extra gains in USD/CNH appear on the cards and are expected to meet a tough barrier around 6.9650, note UOB Group Lee Sue Ann and Markets Strategist Quek Ser Leang.

Key Quotes

24-hour view: “The strong jump in USD came as a surprise (we were expecting it to trade sideways). The rapid advance appears to be overdone but with no sign of easing just yet, USD could rise above the NY high near 6.9510. However, the major resistance at 6.9650 is likely out of reach today. Support is at 6.9300, followed by 6.9230.”