Market news

-

23:32

Stocks. Daily history for Feb 02’2017:

(index / closing price / change items /% change)

Nikkei -233.50 18914.58 -1.22%

TOPIX -17.36 1510.41 -1.14%

Hang Seng -133.87 23184.52 -0.57%

FTSE 100 +33.10 7140.75 +0.47%

DAX -31.55 11627.95 -0.27%

CAC 40 -0.29 4794.29 -0.01%

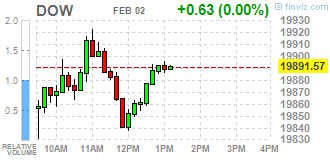

DJIA -6.03 19884.91 -0.03%

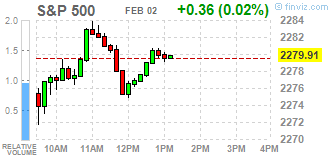

S&P 500 +1.30 2280.85 +0.06%

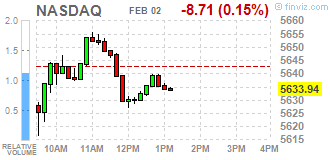

NASDAQ -6.45 5636.20 -0.11%

-

21:08

Major US stock indexes showed little change

Major US stock indexes finished trading around as investors on their guard against the latest protectionist decisions President Donald Trump. In recent weeks, Trump's priorities, such as the imposition of travel restrictions to the United States and out of the trade agreement, have caused uncertainty and made them unpredictable for investors.

As it became known today, the number of Americans who applied for unemployment benefits fell more than expected last week, pointing to a tightening of labor market conditions, which should support the economy this year. Primary applications for state unemployment benefits fell by 14,000 and amounted to a seasonally adjusted 246,000 for the week ending January 28, reported Thursday the Ministry of Labour.

However, the report published by Challenger Gray & Christmas Inc, showed that the number of job cuts in the USA in January was 45,934 compared to 33,627 in December. However, compared with the same period of 2016, the number of job cuts decreased significantly (then figure was 75,114).

DOW index components closed mostly in the red (17 of 30). Most remaining shares fell Caterpillar Inc. (CAT, -1.46%). leaders of growth were shares of Merck & Co., Inc. (MRK, + 3.19%).

Sector S & P index finished the session mixed. The leader turned utilities sector (+ 0.8%). the health sector fell the most (-0.7%).

At the close:

Dow -0.03% 19,884.98 -5.96

Nasdaq -0.11% 5,636.20 -6.45

S & P + 0.06% 2,280.85 +1.30

-

20:00

DJIA -0.18% 19,855.04 -35.90 Nasdaq -0.26% 5,628.05 -14.60 S&P -0.13% 2,276.57 -2.98

-

18:14

Wall Street. Major U.S. stock-indexes little changed

Major U.S. stock-indexes little changed on Thursday, as investors turned wary following President Donald Trump's latest protectionist comments. Trump in a meeting with key lawmakers said he would like to speed up talks to either renegotiate or replace the North American Free Trade Agreement (NAFTA). Investors are also assessing possible consequences of Trump's other comments, including labeling a refugee swap agreement with staunch ally Australia as a "dumb deal" and putting Iran "on notice" for firing a ballistic missile.

Most of Dow stocks in negative area (17 of 30). Top loser - UnitedHealth Group Incorporated (UNH, -1.22%). Top gainer - Merck & Co., Inc. (MRK, +2.69%).

S&P sectors mixed. Top loser - Utilities (+0.8%). Top loser - Healthcare (-0.6%).

At the moment:

Dow 19820.00 +4.00 +0.02%

S&P 500 2275.25 +0.75 +0.03%

Nasdaq 100 5140.00 -8.50 -0.17%

Oil 53.65 -0.23 -0.43%

Gold 1217.00 +8.70 +0.72%

U.S. 10yr 2.47 -0.01

-

17:01

European stocks closed: FTSE 100 +33.10 7140.75 +0.47% DAX -31.55 11627.95 -0.27% CAC 40 -0.29 4794.29 -0.01%

-

16:40

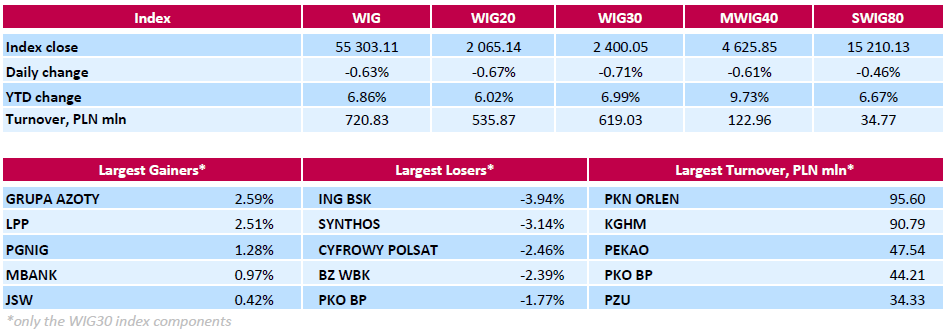

WSE: Session Results

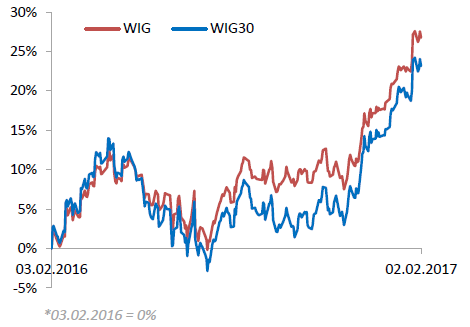

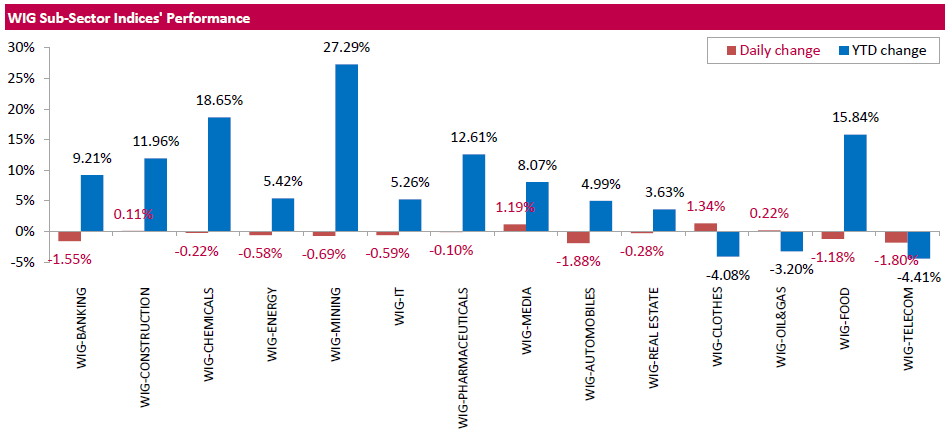

Polish equity market closed lower on Thursday. The broad market measure, the WIG Index, declined by 0.63%. The WIG sub-sector indices mostly closed in negative territory, with WIG-AUTOMOBILES Index (-1.88%) lagging behind.

The large-cap stocks' gauge, the WIG30 Index, fell by 0.71%. A majority of the index components declined, with banking name ING BSK (WSE: ING) underperforming with a 3.94% drop, weighted down by worse-than-forecast Q4 earnings result. The bank reported its net profit amounted to PLN 254.9 mln (+23.9 y/y) in Q4, missing analysts' consensus estimate of PLN 271.8 mln. Other major laggards were chemical producer SYNTHOS (WSE: SNS), media group CYFROWY POLSAT (WSE: CPS) and bank BZ WBK (WSE: BZW), which tumbled by 3.14%, 2.46% and 2.39% respectively. At the same time, chemical producer GRUPA AZOTY (WSE: ATT) and clothing retailer LPP (WSE: LPP) led a handful of gainers, advancing 2.59% and 2.51% respectively. The later was helped by monthly sales report, which revealed the group's revenues totaled about PLN 508 mln in January 2017, up 22% y/y.

-

14:54

WSE: After start on Wall Street

Quotations in the US began with discounts. Today's macro data brought little new to the valuations and investors are clearly waiting for tomorrow's monthly report from the labor market. From the Warsaw market today blows boredom and probably this image will be continued to the end of the session.

An hour before the close of trading WIG20 index was at the level of 2,074 points (-0.24%).

-

14:33

U.S. Stocks open: Dow -0.25%, Nasdaq -0.41%, S&P -0.29%

-

14:29

Before the bell: S&P futures -0.25%, NASDAQ futures -0.22%

U.S. stock-index futures fell after the Federal Reserve gave little insight into whether it would raise interest rates at its next meeting, even as the central bank painted an upbeat picture of the economy.

Global Stocks:

Nikkei 18,914.58 -233.50 -1.22%

Hang Seng 23,184.52 -133.87 -0.57%

Shanghai - Closed

FTSE 7,162.58 +54.93 +0.77%

CAC 4,802.89 +8.31 +0.17%

DAX 11,638.98 -20.52 -0.18%

Crude $54.02 (+0.26%)

Gold $1,225.20 (+1.40%)

-

13:53

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

36.68

0.42(1.1583%)

9017

ALTRIA GROUP INC.

MO

71.5

0.11(0.1541%)

2849

Amazon.com Inc., NASDAQ

AMZN

837

4.65(0.5587%)

45263

Apple Inc.

AAPL

128.29

-0.46(-0.3573%)

170494

AT&T Inc

T

42

-0.06(-0.1427%)

2659

Barrick Gold Corporation, NYSE

ABX

19

0.52(2.8139%)

154158

Boeing Co

BA

163.81

-0.16(-0.0976%)

2018

Caterpillar Inc

CAT

95

-0.11(-0.1157%)

1266

Chevron Corp

CVX

111.21

0.21(0.1892%)

1006

Cisco Systems Inc

CSCO

30.55

0.05(0.1639%)

20174

Citigroup Inc., NYSE

C

55.35

-0.54(-0.9662%)

21505

Deere & Company, NYSE

DE

107.39

0.24(0.224%)

1000

E. I. du Pont de Nemours and Co

DD

76.15

-0.19(-0.2489%)

600

Exxon Mobil Corp

XOM

83.08

0.14(0.1688%)

6643

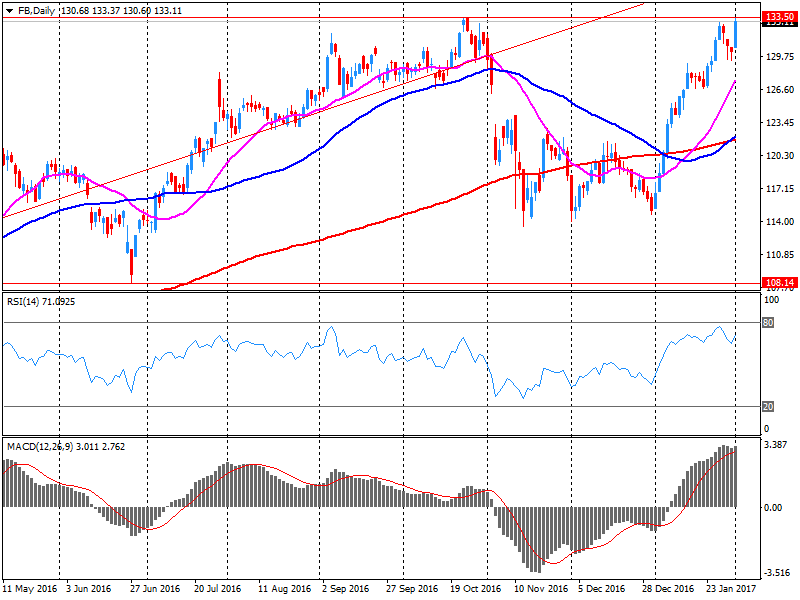

Facebook, Inc.

FB

134.47

1.24(0.9307%)

1741995

FedEx Corporation, NYSE

FDX

185.27

-1.00(-0.5369%)

164

Ford Motor Co.

F

12.29

-0.03(-0.2435%)

24489

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

16.62

-0.22(-1.3064%)

18840

General Electric Co

GE

29.64

-0.05(-0.1684%)

1940

General Motors Company, NYSE

GM

36.12

-0.02(-0.0553%)

1725

Goldman Sachs

GS

228.67

-2.00(-0.867%)

6417

Google Inc.

GOOG

793.28

-2.415(-0.3035%)

2036

Intel Corp

INTC

36.35

-0.17(-0.4655%)

50774

International Business Machines Co...

IBM

173.82

-0.47(-0.2697%)

365

International Paper Company

IP

55.41

-1.09(-1.9292%)

1715

Johnson & Johnson

JNJ

112.83

-0.40(-0.3533%)

710

JPMorgan Chase and Co

JPM

84.15

-0.80(-0.9417%)

13308

McDonald's Corp

MCD

122.17

-0.25(-0.2042%)

201

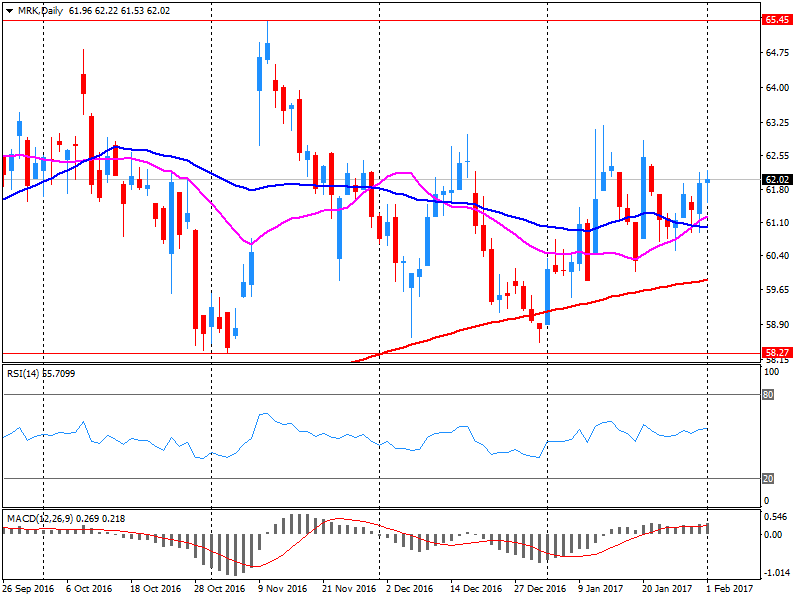

Merck & Co Inc

MRK

62.34

0.24(0.3865%)

180948

Microsoft Corp

MSFT

63.38

-0.20(-0.3146%)

35843

Nike

NKE

52.79

-0.23(-0.4338%)

1868

Pfizer Inc

PFE

31.51

-0.16(-0.5052%)

2484

Starbucks Corporation, NASDAQ

SBUX

53.85

-0.05(-0.0928%)

9753

Tesla Motors, Inc., NASDAQ

TSLA

247.75

-1.49(-0.5978%)

11288

The Coca-Cola Co

KO

41.18

-0.08(-0.1939%)

7846

Twitter, Inc., NYSE

TWTR

17.38

0.14(0.8121%)

57988

United Technologies Corp

UTX

108.01

-0.17(-0.1571%)

1253

Verizon Communications Inc

VZ

48.46

0.07(0.1447%)

3629

Visa

V

82.77

0.33(0.4003%)

2291

Wal-Mart Stores Inc

WMT

66.2

-0.03(-0.0453%)

1305

Walt Disney Co

DIS

111.05

-0.25(-0.2246%)

4596

Yandex N.V., NASDAQ

YNDX

23.43

0.07(0.2997%)

934

-

13:49

Upgrades and downgrades before the market open

Upgrades:

Apple (AAPL) upgraded to Hold from Sell at BGC

Alcoa (AA) upgraded to Overweight from Neutral at JP Morgan

Downgrades:

Facebook (FB) downgraded to Hold at Pivotal Research Group; target lowered to $135

Other:

Facebook (FB) target raised to $148 from $146 at Mizuho

-

13:37

Company News: Facebook (FB) posts stronger-than-expected Q4 results

Facebook reported Q4 FY 2016 earnings of $1.41 per share (versus $0.79 in Q4 FY 2015), beating analysts' consensus estimate of $1.31.

The company's quarterly revenues amounted to $8.809 bln (+50.8% y/y), beating analysts' consensus estimate of $8.495 bln.

FB rose to $134.40 (+0.88%) in pre-market trading.

-

13:26

Company News: Merck (MRK) posts Q4 EPS in line with analysts' estimates

Merck reported Q4 FY 2016 earnings of $0.89 per share (versus $0.93 in Q4 FY 2015), in-line with analysts' consensus estimate.

The company's quarterly revenues amounted to $10.115 bln (-1% y/y), missing analysts' consensus estimate of $10.234 bln.

The company also issued downside guidance for FY 2017, projecting EPS of $3.72-3.87 (versus analysts' consensus estimate of $3.87) and revenues of $38.60-40.10 bln (versus analysts' consensus estimate of $40.19 bln).

MRK fell to $62.00 (-0.16%) in pre-market trading.

-

13:08

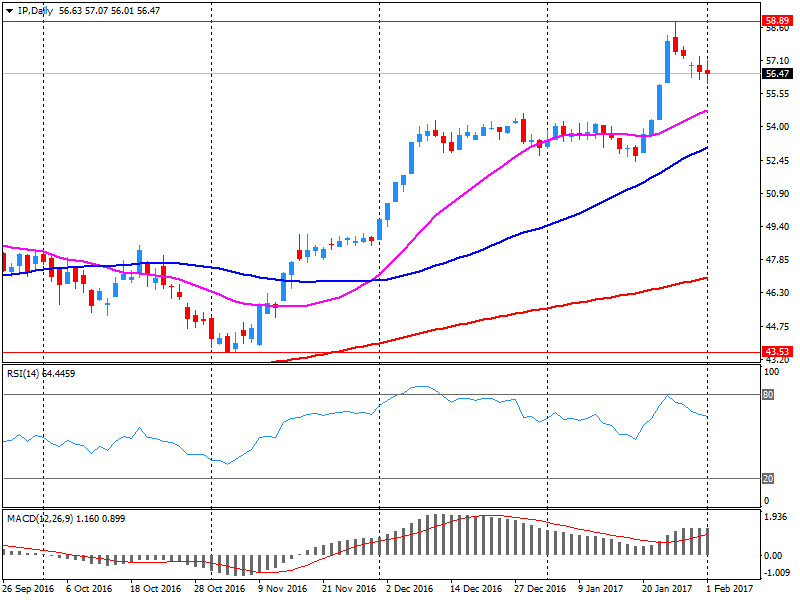

Company News: Intl Paper (IP) Q4 results beat analysts’ expectations

Intl Paper reported Q4 FY 2016 earnings of $0.73 per share (versus $0.87 in Q4 FY 2015), beating analysts' consensus estimate of $0.71.

The company's quarterly revenues amounted to $5.381 bln (-1.1% y/y), beating analysts' consensus estimate of $5.320 bln.

IP rose to $57.00 (+0.89%) in pre-market trading.

-

12:03

WSE: Mid session comment

The first half of today's trading has not brought major changes. Both the Warsaw market and on exchanges Euroland prevail slight descent down. Above-average weakness stands out the banking sector. The level of turnover on both the broad market and the sector's largest companies is mediocre.

After four hours of trading the WIG20 index was at the level of 2,074 points (-0,25%).

-

08:16

WSE: After opening

WIG20 index opened at 2078.01 points (-0.05%)*

WIG 55633.43 -0.03%

WIG30 2416.41 -0.04%

mWIG40 4653.69 -0.01%

*/ - change to previous close

The cash market (the WIG20 index) started the day from a modest discount of 0.05% with a moderate turnover. The German DAX is falling more than 0.3%, and against this background neutral beginning in Warsaw looks quite good.

After fifteen minutes of trading, the WIG20 index was at the level of 2,078 points (-0,01%).

-

07:37

Negative start of trading expected on the major stock exchanges in Europe: DAX -0.3%, CAC40 -0.2%, FTSE -0.2%

-

07:18

WSE: Before opening

Wednesday's session on the New York stock markets ended with slight increases in the major indexes. Heavily went up course of Apple (over 6%), which the day before, after the session, presented better than expected the quarterly results.

The Dow Jones Industrial rose at the close of 0.13 percent, the S&P 500 went up by 0.03 percent and the Nasdaq Comp. gained 0.50 percent. The fourth week in a row there was an increase in crude oil inventories in the US.

Important was also the decision of the Federal Open Market Committee. The noticeable was the lack of guidance to raise rates in March, which resulted in a slight weakening of the US currency and an increase in raw material prices.

In the night futures on US indices began to fall , while the Japanese Nikkei lost 1.2% in the morning. Thus, beginning in Europe can present a slightly down.

-

06:31

Global Stocks

U.K. stocks closed lower Tuesday, locking in a monthly loss, weighed down in part by a jump in the British pound, though gains by miners helped limit the drop. Pound strength can unsettle U.K. stock investors, as it cuts into profit made overseas by British multinational companies.

U.S. stocks closed up modestly Wednesday after the Federal Reserve stood pat on interest rates and offered a positive view of the economy, while shares of Apple rallied a day after the iPhone maker reported strong earnings. Apple, as the largest U.S. company by market cap, which means it has a heavy weighting in major indexes, was offsetting weakness elsewhere in the market. Seven of the S&P 500's 11 primary sectors were lower on the day, continuing a recent bout of fragility seen this week.

Global investors continued to search for direction Thursday after the U.S. Federal Reserve's latest policy statement, which held interest rates steady, as expected. For weeks, investors have been flipping between optimism and concern. This week started with worry, but the mood became more upbeat, with strong economic data out of the U.S., China and Europe.

-