Market news

-

23:29

Stocks. Daily history for Nov 14’2016:

(index / closing price / change items /% change)

Nikkei 225 17,672.62 +297.83 +1.71%

Shanghai Composite 3,210.10 +14.06 +0.44%

S&P/ASX 200 5,345.73 0.00 0.00%

FTSE 100 6,753.18 +22.75 +0.34%

CAC 40 4,508.55 +19.28 +0.43%

Xetra DAX 10,693.69 +25.74 +0.24%

S&P 500 2,164.20 -0.25 -0.01%

Dow Jones Industrial Average 18,868.69 +21.03 +0.11%

S&P/TSX Composite 14,598.45 +43.04 +0.30%

-

20:00

DJIA 18866.77 19.11 0.10%, NASDAQ 5224.48 -12.64 -0.24%, S&P 500 2165.64 1.19 0.05%

-

17:25

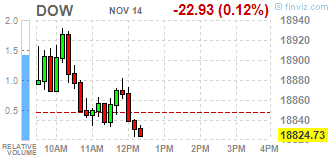

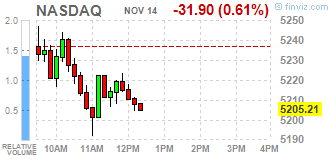

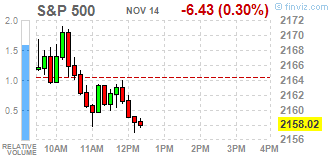

Wall Street. Major U.S. stock-indexes slightly fell

Major U.S. stock-indexes slightly fell. The S&P 500 and the Dow Jones industrial average pared early gains and were little changed on Monday as investors looked for more clarity on President-elect Donald Trump's policies. The tech-heavy Nasdaq Composite was lower, adding to last week's losses. The Dow, which capped off its best week in five years on Friday, hit a another record-high just after the start of trading. Since Trump's triumph last Tuesday, investors have been betting on his campaign promises to simplify regulation in the health and financial sectors and boost spending on infrastructure.

Most of Dow stocks in negative area (19 of 30). Top gainer - UnitedHealth Group Incorporated (UNH, +3.61%). Top loser - Visa Inc. (V, -4.59%).

Most of S&P sectors also in negative area. Top gainer - Conglomerates (+1.7%). Top loser - Technology (-1.3%).

At the moment:

Dow 18782.00 -5.00 -0.03%

S&P 500 2154.75 -6.75 -0.31%

Nasdaq 100 4690.25 -57.75 -1.22%

Oil 42.34 -1.07 -2.46%

Gold 1219.20 -5.10 -0.42%

U.S. 10yr 2.21 +0.09

-

17:00

European stocks closed: FTSE 6753.18 22.75 0.34%, DAX 10693.69 25.74 0.24%, CAC 4508.55 19.28 0.43%

-

16:35

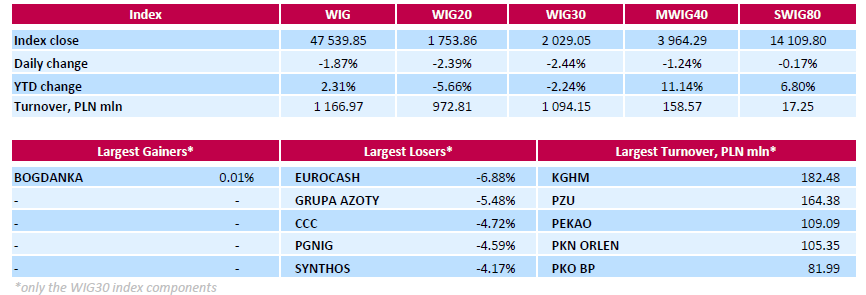

WSE: Session Results

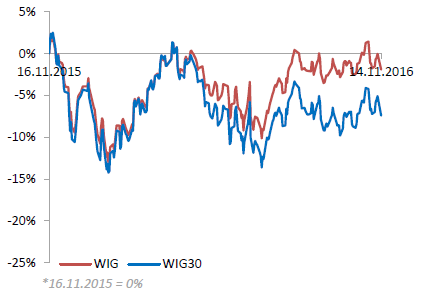

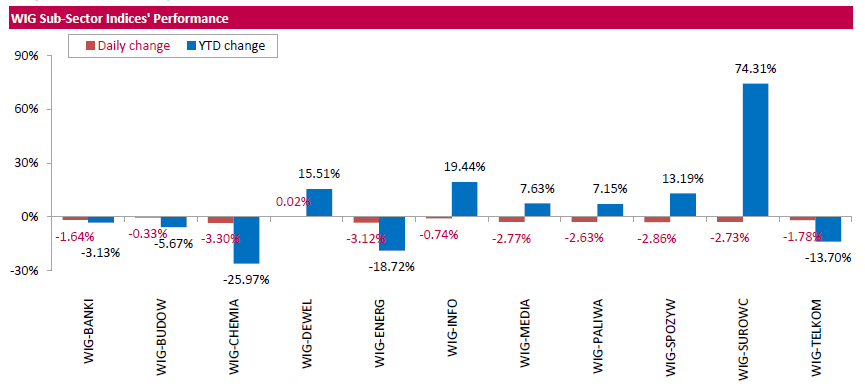

Polish equity market closed lower on Monday. The broad market benchmark, the WIG Index, plunged by 1.87%. The WIG sub-sector indices were mainly lower with chemicals (-3.3%) lagging behind.

The large-cap companies' measure, the WIG30 Index, fell by 2.62%. Thermal coal producer BOGDANKA (WSE: LWB) was sole gainer within the index constituents, edging up 0.01%. At the same time, FMCG-wholesaler EUROCASH (WSE: EUR) and chemical producer GRUPA AZOTY (WSE: ATT) suffered the steepest drops, down 6.88% and 5.48% respectively. Other major underperformers were footwear retailer CCC (WSE: CCC), oil and gas producer PGNIG (WSE: PGN), chemical producer SYNTHOS (WSE: SNS), agricultural producer KERNEL (WSE: KER), and two gencos PGE (WSE: PGE) and ENERGA (WSE: ENG), which lost between 3.88% and 4.72%.

-

14:51

WSE: After start on Wall Street

The week on the Warsaw market did not start well. The trading for a few hours is not able to pick up from the session lows. Adding to this the style of today's descent (width, rotation, scale) it does not look good. In the initial phase of the session we were not able to take advantage of the relatively positive sentiment on core markets and in particular the surprisingly positive start of trading in Europe, which was inspired by a better behavior of the US contracts. Entry into afternoon phase of trading in Europe was held under the sign of far more modest than previously growth, and at the same time leaving the level of resistance, visible especially in Germany and France.

The market in the US opens with increase, but the beginning looks neutral on the background of recent observed volatility.

An hour before the end of today's trading the WIG20 index was at the level of 1,759 points (-2.06%).

-

14:33

U.S. Stocks open: Dow +0.23%, Nasdaq -0.10%, S&P +0.12%

-

14:27

Before the bell: S&P futures +0.27%, NASDAQ futures +0.06%

U.S. stock-index futures inched up as a slump in crude prices sapped some momentum from investors' surging appetite for riskier assets.

Global Stocks:

Nikkei 17,672.62 +297.83 +1.71%

Hang Seng 22,222.22 -308.87 -1.37%

Shanghai 3,210.10 +14.06 +0.44%

FTSE 6,752.16 +21.73 +0.32%

CAC 4,506.42 +17.15 +0.38%

DAX 10,723.30 +55.35 +0.52%

Gold $42.77 (-1.47%)

Crude $1,221.40 (-0.24%)

-

13:57

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

29.53

0.23(0.785%)

330

ALTRIA GROUP INC.

MO

61.89

0.13(0.2105%)

3595

Amazon.com Inc., NASDAQ

AMZN

744.78

5.77(0.7808%)

25016

Apple Inc.

AAPL

108.19

-0.24(-0.2213%)

97997

AT&T Inc

T

36.59

0.08(0.2191%)

8340

Barrick Gold Corporation, NYSE

ABX

14.74

-0.10(-0.6739%)

115163

Boeing Co

BA

149

0.48(0.3232%)

1146

Caterpillar Inc

CAT

93.29

0.28(0.301%)

7214

Chevron Corp

CVX

106.35

-0.29(-0.2719%)

1810

Cisco Systems Inc

CSCO

31.42

0.06(0.1913%)

7504

Citigroup Inc., NYSE

C

53.09

0.26(0.4921%)

267959

E. I. du Pont de Nemours and Co

DD

69.57

0.36(0.5202%)

685

Exxon Mobil Corp

XOM

85.38

-0.29(-0.3385%)

6612

Facebook, Inc.

FB

119.35

0.33(0.2773%)

133164

Ford Motor Co.

F

12.24

-0.04(-0.3257%)

26080

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

14.17

0.23(1.6499%)

208937

General Electric Co

GE

30.82

0.11(0.3582%)

36271

General Motors Company, NYSE

GM

33.82

-0.20(-0.5879%)

5761

Goldman Sachs

GS

204.94

1.00(0.4903%)

18585

Google Inc.

GOOG

758

3.98(0.5278%)

9745

Home Depot Inc

HD

130.55

0.70(0.5391%)

2216

HONEYWELL INTERNATIONAL INC.

HON

113.68

0.43(0.3797%)

184

Intel Corp

INTC

34.63

0.02(0.0578%)

2262

International Business Machines Co...

IBM

161.96

0.69(0.4279%)

3114

International Paper Company

IP

45.79

0.13(0.2847%)

100

Johnson & Johnson

JNJ

119

0.53(0.4474%)

1314

JPMorgan Chase and Co

JPM

77.05

0.36(0.4694%)

25692

McDonald's Corp

MCD

114.55

0.33(0.2889%)

950

Merck & Co Inc

MRK

64.2

0.25(0.3909%)

3617

Microsoft Corp

MSFT

59.15

0.13(0.2203%)

59590

Pfizer Inc

PFE

33.09

0.50(1.5342%)

30448

Procter & Gamble Co

PG

83.71

0.13(0.1555%)

2365

Starbucks Corporation, NASDAQ

SBUX

54

0.07(0.1298%)

4548

Tesla Motors, Inc., NASDAQ

TSLA

188

-0.56(-0.297%)

11387

Twitter, Inc., NYSE

TWTR

18.85

0.30(1.6173%)

225765

Visa

V

82.55

0.67(0.8183%)

290

Yahoo! Inc., NASDAQ

YHOO

40.3

-0.12(-0.2969%)

367

Yandex N.V., NASDAQ

YNDX

18.42

-0.29(-1.55%)

945

-

13:52

Upgrades and downgrades before the market open

Upgrades:

Citigroup (C) upgraded to Overweight from Equal-Weight at Morgan Stanley

Downgrades:

Other:

-

12:03

WSE: Mid session comment

The Warsaw market from the very beginning of the session grabs clear shortness of breath, unable to fully take advantage of a favorable environment, which is consolidating at key resistance of core markets indices. But this is not a surprise, the WSE fits clearly in the attitude of emerging markets where trade is taking increasingly lower levels. To the weakness of blue chips attached worse attitude of the broad market in the form of small and medium-sized companies. In addition, in Western Europe there was also deterioration in sentiment in the noon phase of trading, although increases there are still maintained. Locally, in the case of blue chips not much left from the post-election rally and at the level of the WIG20 index we are back to the area of lows from the beginning of November, when the market feared a victory of Trump.

At the halfway point of today's trading the WIG20 index was at the level 1,767 points (-1,67%), with the turnover of PLN 465 million.

-

08:51

Major stock exchanges trading in the green zone: FTSE + 0.9%, DAX + 0.8%, CAC40 + 0.9%, FTMIB + 0.9%, IBEX + 0.9%

-

08:18

WSE: After opening

WIG20 index opened at 1794.23 points (-0.14%)*

WIG 48626.04 0.37%

WIG30 2089.27 0.46%

mWIG40 4029.09 0.38%

*/ - change to previous close

The cash market started the day from a discount of 0.14% to 1,794 points, but quickly rises above, piercing even the psychological level of 1,800 points.

The beginning of the session on the Warsaw Stock Exchange is the answer to better performance of core markets, namely the maintenance of nearby peaks, which opens the way to the theoretically possible attack. The first violin again plays KGHM, reacting to Friday's turmoil in the copper market, which look like classic solstice. The market is very volatile and these fluctuations after the one day break must find a new balance.

After fifteen minutes of trading the WIG20 index was at the level of 1,799 points (+0,17%).

-

07:20

WSE: Before opening

The Warsaw Stock Exchange into the new week comes with the need to catch up the one missing day of trading. On Friday, during our national holiday the global financial market worked and a lot on it happened. Investors are still trying to discount the possible changes associated with Donald Trump winning. The market is counting on increased spending financed by increased issuance of bonds while reducing taxes. As a result increase the bonds profitability, strengthens the dollar, and the assets of emerging markets have come under pressure. On Friday, the MSCI Emerging Markets index went down by 2.9% and broke the important support. It's not the best news for the Warsaw Stock Exchange.

Morning mood is very positive. Contracts in the US gain of 0.6%, which should lead to positive openings in Europe.

In Asia, the Nikkei gaining only and the other emerging parquets are under pressure. Copper prices remain very volatile but the balance puts the price of metal near the close on Thursday, which means a relatively neutral impact on our market.

-