Noticias del mercado

-

22:25

Most U.S. stocks fell

Most U.S. stocks fell, with earnings and the price of crude largely setting the tone for individual shares as investors assessed the Federal Reserve's latest policy decision for the timing of interest-rate increases.

Job gains were "strong" in June and indicators "point to some increase in labor utilization in recent months," the Federal Open Market Committee said in a statement Wednesday after a two-day meeting in Washington. The Fed held rates steady and continued to emphasize a gradual pace of increases.

"Not much has changed, though there's some option for them to raise rates in September," said Brent Schutte, chief investment strategist at Northwestern Mutual Wealth Management Company, which manages $89 billion in assets. "That's why the market's not reacting much. We all have to get used to the fact that every one of these meetings is going to be something different."

Fed fund futures show even odds the Fed will raise rates at its December meeting, up from 48 percent before the statement.

The main U.S. equity gauge has surged in the past month with global equities on speculation the Fed won't rush to add stimulus even as the economy shows signs of picking up steam. After recovering its losses following the U.K.'s vote to leave the European Union, the S&P 500 went on to post seven records in 10 days.

Optimism that corporate earnings would help support gains has boosted the gauge by 19 percent from a February low. Analysts have tempered their estimates for second-quarter profit declines to 4.5 percent and are forecasting a rebound starting in the current period. The S&P 500 is now up 6.1 percent for the year, one of the biggest winners among developed-market benchmarks.

Before the Fed's statement, traders priced in little chance of a rate increase today. Uneven data and the possible fall out from Brexit have held down expectations for higher borrowing costs this year. December is the first month for which traders projected an at least even chance of a rate increase.

Apple jumped 6.6 percent, the most since April 2014, after posting a smaller-than-expected revenue decline as its cheaper iPhone model gained more traction. Boeing Co. rose 0.8 percent after reporting a narrower loss than analysts projected. Twitter sank 14.5 percent, the most in three months, after its third-quarter sales fell well short of predictions. Coca-Cola dropped 3.3 percent, the most since April, after sales trailed estimates.

-

21:01

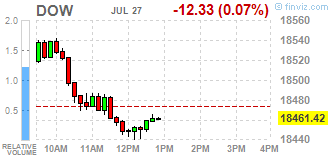

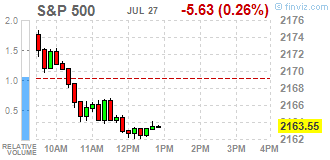

DJIA 18505.80 32.05 0.17%, NASDAQ 5142.10 32.05 0.63%, S&P 500 2169.15 -0.03 0%

-

18:57

Wall Street. Major U.S. stock-indexes demonstrated mixed dynamics

Major U.S. stock-indexes demonstrated mixed dynamics as encouraged by better-than-expected quarterly results of Apple (AAPL) growth in the technology sector was offset by decline in energy sector on weakening oil prices. Investors also expect the US Federal Reserve decision to raise interest rates.

Oil prices dropped sharply after a government report showed that the U.S. crude inventories unexpectedly rose during the week ending July 22.

In macroeconomic environment, the Commerce Department reported orders for the U.S.durable goods fell 4% in June, marking the biggest drop in almost two years. Economists had forecast durable goods orders falling 1.1 percent last month.

The National Association of Realtors (NAR) reported pending home sales in June increased by mere 0.2% to 111.0 points. That was the second highest value in the last 12 months and well above the average reading for 2015 (108.9 points). Economists had expected the index to increase by 1.4% after falling 3.7% in May.

Most of Dow stocks in negative area (22 of 30). Top loser - The Coca-Cola Company (KO, -3.44%). Top gainer - Apple Inc. (AAPL, +6.55%).

All S&P sectors, but for Healthcare (+0.06%), in negative area. Top loser - Utilities (-0.96%).

At the moment:

Dow 18390.00 -8.00 -0.04%

S&P 500 2158.25 -5.00 -0.23%

Nasdaq 100 4686.75 +23.00 +0.49%

Crude Oil 41.96 -0.96 -2.24%

Gold 1325.90 +5.10 +0.39%

U.S. 10yr 1.55 -0.02

-

18:12

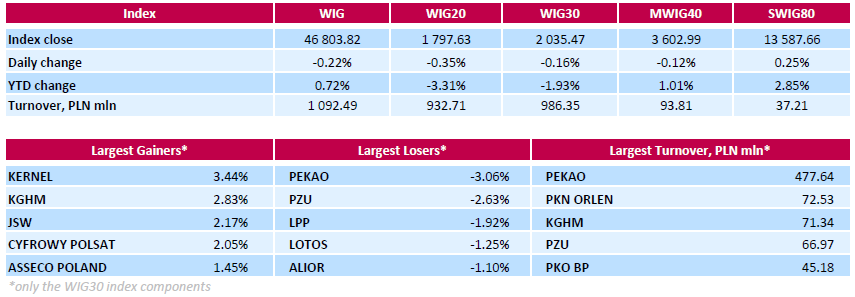

WSE: Session Results

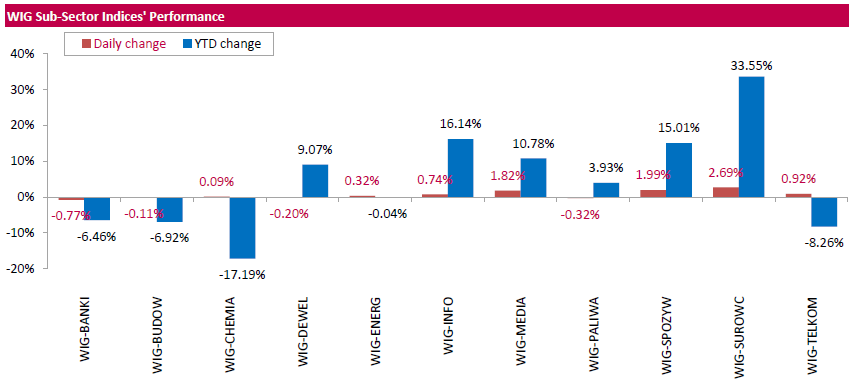

Polish equity market closed lower on Wednesday. The broad market measure, the WIG Index, fell by 0.22%. Sector performance within the WIG Index was mixed. Banking sector (-0.77%) dropped the most, while materials (+2.69%) fared the best.

The large-cap stocks' measure, the WIG30 index, went down 0.16%. In the index basket, bank PEKAO (WSE: PEO) led the decliners, dropping by 3.06% on the back of the announcement that UniCredit considers selling its stake in the bank. Other biggest losers were insurer PZU (WSE: PZU), clothing retailer LPP (WSE: LPP) and oil refiner LOTOS (WSE: LTS), retreating by 2.63%, 1.92% and 1.25% respectively. On the country, agricultural producer KERNEL (WSE: KER), copper producer KGHM (WSE: KGH) and coking coal miner JSW (WSE: JSW) were the top advancers, gaining 3.44%, 2.83% and 2.17% respectively.

-

18:03

European stocks closed: FTSE 6750.43 26.40 0.39%, DAX 10319.55 71.79 0.70%, CAC 4446.96 52.19 1.19%

-

15:50

WSE: After start on Wall Street

Today's afternoon we met the preliminary (June) reading of data on the durable goods orders in the US, which were clearly worse than expected and support the scenario in which the Fed's policy will not change until the end of the year. The market reacted accordingly by weakening of the dollar.

The US market started from increases and the situation on the Warsaw Stock Exchange has improved in effect the WIG 20 index has returned to the region of 1,800 points.

-

15:34

U.S. Stocks open: Dow +0.30%, Nasdaq +0.65%, S&P +0.20%

-

15:29

Before the bell: S&P futures +0.21%, NASDAQ futures +0.81%

U.S. index futures rose.

Global Stocks:

Nikkei 16,664.82 +281.78 +1.72%

Hang Seng 22,218.99 +89.26 +0.40%

Shanghai 2,991.12 -59.043 -1.94%

FTSE 6,771.9 +47.87 +0.71%

CAC 4,467.61 +72.84 +1.66%

DAX 10,341.6 +93.84 +0.92%

Crude $42.84 (-0.19%)

Gold $1322.60 (+0.14%)

-

15:04

Upgrades and downgrades before the market open

Upgrades:

Apple (AAPL) upgraded to Outperform from Mkt Perform at Raymond James

Downgrades:

Twitter (TWTR) downgraded to Hold from Buy at Cantor Fitzgerald

Twitter (TWTR) downgraded to Hold from Buy at Canaccord Genuity

Twitter (TWTR) downgraded to Hold at Axiom Capital; target lowered to $16

Other:

Apple (AAPL) reiterated with a Buy Mizuho; target $120

Apple (AAPL) target raised to $115 at Macquarie

Verizon (VZ) target raised to $57 from $54 at FBR Capital

Twitter (TWTR) target lowered to $14 at Wedbush

Twitter (TWTR) target lowered to $17 from $20 at RBC Capital Mkts

Twitter (TWTR) reiterated with a Sell at Stifel; target lowered to to $9

Caterpillar (CAT) target raised to $73 at RBC Capital Mkts

-

14:27

Company News: Altria (MO) Q2 results beat analysts’ expectations

Altria reported Q2 FY 2016 earnings of $0.81 per share (versus $0.74 in Q2 FY 2015), beating analysts' consensus estimate of $0.80.

The company's quarterly revenues amounted to $6.521 bln (-1.4% y/y), beating analysts' consensus estimate of $5.014 bln.

MO rose to $68.74 (+1.19%) in pre-market trading.

-

14:14

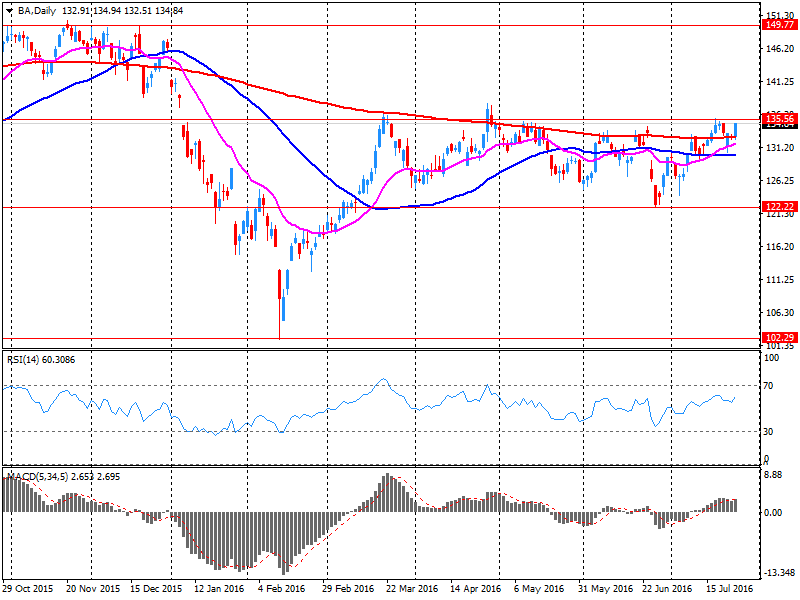

Company News: Boeing (BA) suffers losses in Q2

Boeing reported Q2 FY 2016 loss of $0.44 per share (versus income of $1.62 in Q2 FY 2015), missing analysts' consensus estimate of income of $2.24.

The company's quarterly revenues amounted to $24.755 bln (+0.9% y/y), beating analysts' consensus estimate of $24.174 bln.

BA rose to $137.00 (+1.59%) in pre-market trading.

-

13:49

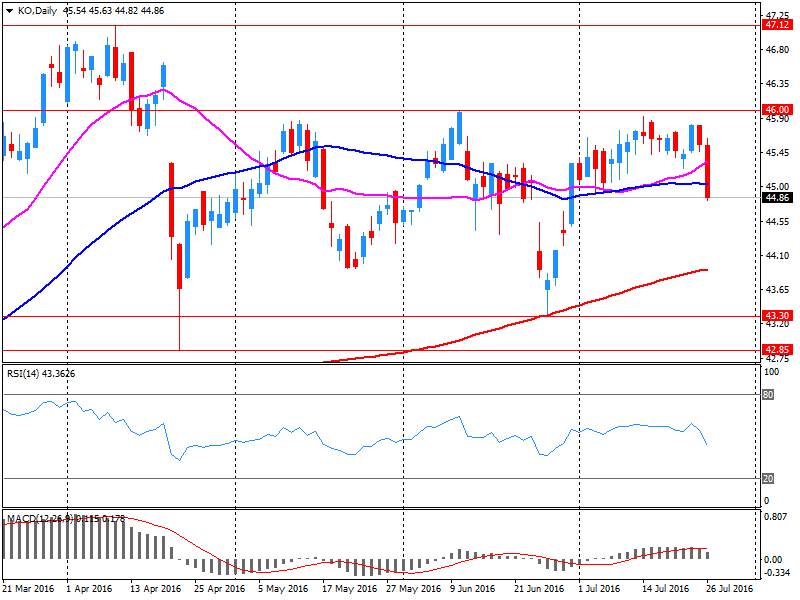

Company News: Coca-Cola (KO) Q2 EPS beat analysts’ estimate

Coca-Cola reported Q2 FY 2016 earnings of $0.60 per share (versus $0.63 in Q2 FY 2015), beating analysts' consensus estimate of $0.58.

The company's quarterly revenues amounted to $11.539 bln (-5.1% y/y), slightly missing analysts' consensus estimate of $11.630 bln.

KO fell to $44.00 (-1.96%) in pre-market trading.

-

13:11

WSE: Mid session comment

Indices of the Warsaw Stock Exchange record today declines in contrast to the indices in Western Europe, which have clearly increased. The balance of power in the market is dominated by a strong sell-off of shares of Pekao. Discount of Pekao reached more than 4 percent. The backfire of decrease in quotations of Pekao came also in other financial companies (PZU, PKO, Alior). The market has long speculated that the "re-Polonization" of the banking sector in Poland would take place just via PZU.

Noticeably loses the Polish zloty and this refers to the actual supply of PLN, not a response to changes in the eurodollar, which happens to be very stable today.

With the passage of time the pulse associated with Pekao slowly blurred, and the market seeing the stable pros in environment begins to mitigate imbalances. If we manage to finish the trading within level of 1,800 points or above, results of the session would be optimistic, but of course with an open risk for tomorrow's opening in reaction to what the global market will do after the message of the FOMC meeting.

The WIG20 ended the first half of the session at 1,793 points (-0.56%) and with turnover of PLN 403 mln, which almost half of it was made on the shares of Pekao.

-

12:40

Major stock indices in Europe show a positive trend

European stocks showing again strong increases after four days of consolidation, helped by positive corporate earnings and expectations of large package of stimulus measures in Japan. However, investors are cautious on the eve of the announcement of the Federal Reserve and Bank of Japan meetings.

Analysts say that the Fed is likel not to change the interest rate, but market participants are hoping to get new guidelines on the possible timing of interest rate increases in the coming months after a series of strong data in the US. Today futures on interest rates suggest that the market is taken into account a 2% probability of a rate hike in July. Meanwhile, the probability of a rate hike in December, up almost 20%.

Some support for the market had statistical data on Britain. The ONS said that in the 2nd quarter gross domestic product grew by 0.6 percent compared with an increase of 0.4 percent in the first three months of this year. It was expected that the economy will expand again by 0.4 percent. In annual terms, GDP grew by 2.2 percent, recording the strongest growth during the year, and accelerate the pace compared to the first quarter (+2.0 percent). It was predicted that economic growth will stabilize at 2.0 percent. However, experts say that such a steady rate of growth can not continue into the second half of the year, given the shock to the economy as a result of voting for a way out of the EU. In the 2nd quarter, the services sector recorded an increase of 0.5 percent, while the manufacturing sector - by 2.1 percent (the best figure since 1999). In contrast, the segment of construction and agriculture reported a decrease of 0.4 percent and 1.0 percent respectively.

The composite index of the largest companies in Europe Stoxx 600 added 0.5%. The French CAC 40 index, which shows an increase of 1.4%, is the leader among the Western European markets.

Quotes of LVMH Moet Hennessy Louis Vuitton rose 7.8% after the world's largest luxury goods reported a strong demand for champagne and cognac.

PSA Group's shares rose 7.1 percent, as the automaker announced the increase of earnings for the first half of the year.

The cost of Airbus Group SE has grown by 4.9 percent since the airline revenue beat analysts' expectations.

The price of Air France-KLM Group increased by 2.8 percent after the news about the increase in operating profit.

Capitalization of ITV Plc rose 7.5 percent after the British broadcaster reported an increase in sales in the first half of the year.

Cost of Banco Santander SA rose 3.5 percent as the bank's profit exceeded analysts' expectations.

At the moment:

FTSE 100 +23.92 6747.95 + 0.36%

DAX +71.12 10318.88 + 0.69%

CAC 40 +60.80 4455.57 + 1.38%

-

09:20

WSE: After opening

WIG20 index opened at 1800.65 points (-0.18%)*

WIG 46818.98 -0.18%

WIG30 2033.02 -0.28%

mWIG40 3607.99 0.02%

*/ - change to previous close

European exchanges began optimistically, the DAX and the CAC are gaining in value. However, the Warsaw Stock Exchange has a problem with the stock price movements of Pekao (WSE: PEO). As reported in a previous comment, the bank Uncredit considering getting rid of all of his shares in this company. This information dominated morning trading and shares of Pekao stand out both in terms of deflection and turnover. This information spoiled sentiment across the segment of blue chips, and brought the WIG20 index to the level of 1,790 points, which is in the area of support in the form of upward trend line.

-

08:42

Expected positive start of trading on the major stock exchanges in Europe: DAX + 0,3%, FTSE 100 + 0,1%, CAC 40 + 0.4%

-

08:28

WSE: Before opening

Tuesday's session on Wall Street ended on neutral levels and the S&P500 index gained 0.03 percent, so we may expect that openings in Europe will not be particularly exciting. It is worth to note the increase in the share price of Apple in post-session trade - associated with the quarterly results, which turned out to be better than expected at both the net profit and revenue. In response to the results of the share price of Apple's in post-session trade grew more than 5 percent

Warsaw WIG20 index is trying to move away from the level of 1,800 points, but with rather weak attempts. The credibility of the market does not improve low turnover, which signals the summer phase of the trade.

The attention of investors on the Warsaw market should be focused on the banking sector. To the familiar theme of currency loans today comes news that UniCredit is considering a full exit from shareholding of Polish bank Pekao SA (WSE: PEO).

During today's session, there is no significant macroeconomic publications from the domestic market. Investors will focus on the ending of the Fed meeting. No one expects the FOMC hikes interest rate, however, any clues will be searched as to the likelihood of the loan price increase at the September meeting of the American central bank authorities.

From the currencies point of view, on the most currency pairs linked to PLN we may see consolidation in anticipation of a new impetus to trade.

-

07:23

Global Stocks

European stocks closed with small gains Tuesday as analysts pinned the muted action on traders waiting for news from central banks due later in the week.

Investors waded through a slew of corporate updates, including a higher takeover bid for brewer SABMiller PLC and the potential breakdown of a deal involving Italy's Mediaset SpA that drove its shares down by double digits.

The Stoxx Europe 600 SXXP, +0.10% inched up 0.1% to finish at 341.26, after ending 0.2% higher on Monday.

On Tuesday, U.S. equity markets closed mixed while stocks in Europe traded slightly higher with all eyes were on the Fed, which concludes its two-day policy meeting later on Wednesday.

The U.S. central bank is widely expected to stand pat on monetary policy and the markets will sift through its statements - a post-meeting news conference will not be held - for any hints of the timing on future interest rate hikes. Expectations of a September increase are clouded ahead of the U.S. presidential election in November, but markets see a roughly 50-50 chance of a rise in December.

Asian stocks climbed to fresh near one-year highs and the Japanese yen weakened on Wednesday as awaited central bank meetings this week that could see fresh stimulus in Japan and provide clues on U.S. interest rates.

MSCI's broadest index of Asia-Pacific shares outside Japan .MIAPJ0000PUS was up 0.2 percent, climbing to its highest since Aug. 11 2015. It is up 10 percent in a month.

Japan's Nikkei .N225 gained 1.1 percent, leading the region.

There is a near-consensus among traders that the Bank of Japan will ease on Friday, most likely by ramping up its already massive purchases of government bonds and riskier assets.

Cutting interest rates into negative territory has proved unpopular with the public and the government, so deepening those cuts is a less likely option, sources familiar with central bank thinking say.

But some market watchers say a BOJ move may be too close to call, and many central bank policymakers may prefer to hold off on action as they expect an anticipated fiscal stimulus package and a delay in next year's sales tax hike to boost growth.

Japanese Prime Minister Shinzo Abe will announce details of a long-awaited 27 trillion yen ($254.2 billion) fiscal stimulus package later on Wednesday, Fuji TV reported. That would be more than expected earlier, but critics will be watching to see how much is actually new spending.

Hong Kong stocks .HSI rose 0.4 percent as mainland Chinese investors continued to snap up shares through a stock market connection scheme.

-

04:04

Nikkei 225 16,600.87 +1.33%, Shanghai Composite 3,050.55 +0.01%, S&P/ASX 200 5,532 -0.10%

-

00:32

Stocks. Daily history for Jun Jul 26’2016:

(index / closing price / change items /% change)

Nikkei 225 16,383.04 -1.43%

Shanghai Composite 3,050.18 +1.14%

S&P/ASX 200 5,537.47 +0.07%

Xetra DAX 10,247.76 +0.49%

FTSE 100 6,724.03 +0.21%

CAC 40 4,394.77 +0.15%

S&P 500 2,169.18 +0.03%

Dow Jones 18,473.75 -0.10%

S&P/TSX Composite 14,550 +0.36%

-