Notícias do Mercado

-

22:50

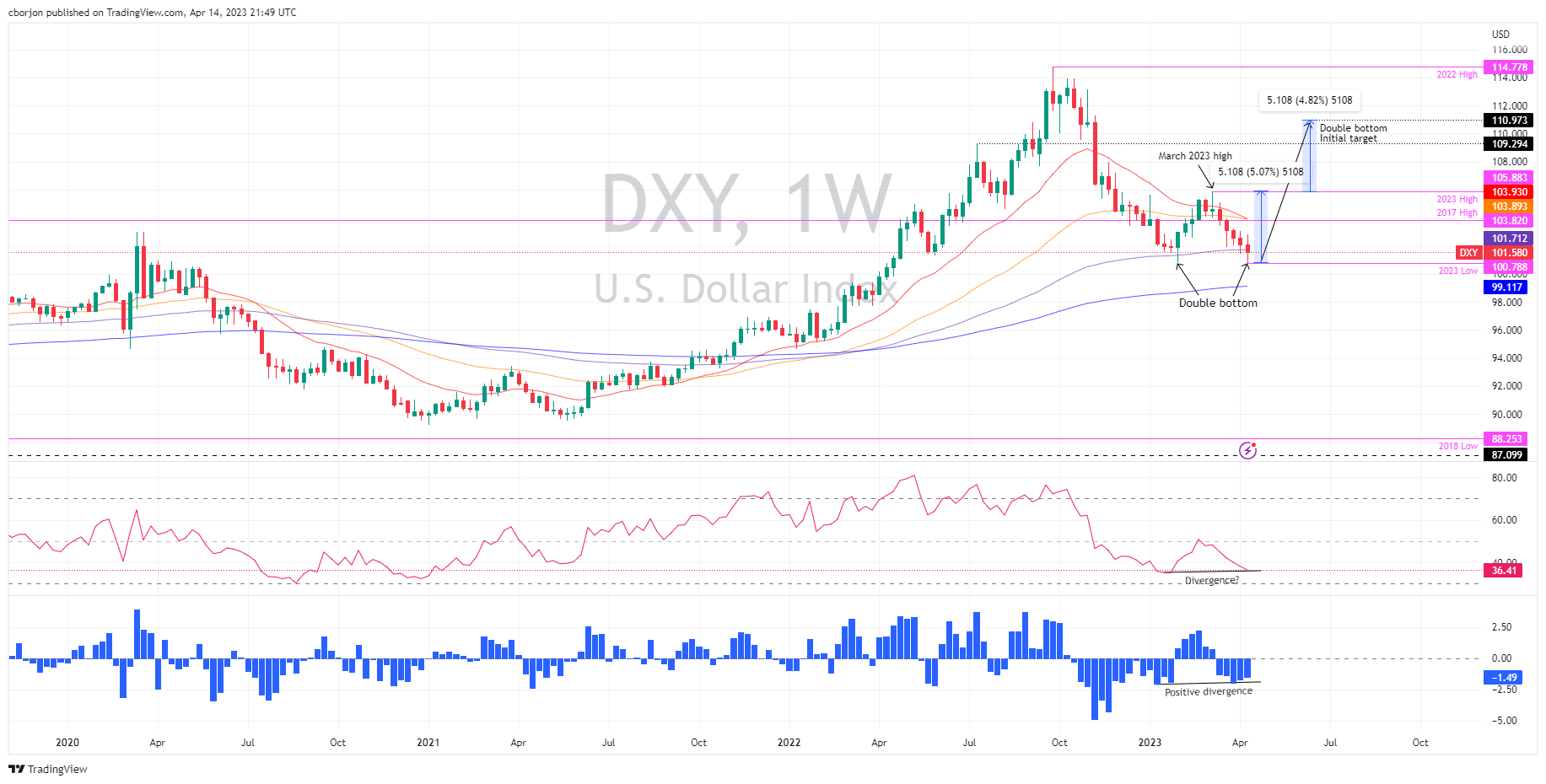

US Dollar Index: Could a double bottom at the weekly chart drive the DXY to 111.000?

- The US Dollar Index found bids at around the YTD lows at 100.788.

- USD bulls must retake 104.000 to challenge YTD high at 105.883 and maintain a double-bottom approach.

- Contrarily, USD bears must reclaim 100.788 to test the 200-week EMA at around 99.117.

The US Dollar Index (DXY), a basket of six currencies against a basket of peers, snaps three days of straight losses and climbs 0.56% as the New York session ends. At the time of writing, the DXY exchanges hand at 101.570 as a bullish engulfing candle pattern emerges in the daily chart.

US Dollar Index Price Action

From a weekly chart perspective, the US Dollar Index remains upward biased. The DXY’s fall from around September 2022 highs at 114.728 towards 2023 lows of 100.788 bottomed around the latter, depicting a double bottom formation. Furthermore, the 200-week Exponential Moving Average (EMA) sits comfortably at around 99.117. The Relative Strength Index (RSI) is in bearish territory, but in the recent dip, the RSI is bottoming higher than the prior’s through. The Rate of Change (RoC) also displays that selling pressure is waning, which could pave the way for further upside.

Upside risks in the DXY lie at the confluence of the 50 and 20-week EMAs, around 103.893-103.930. The break above will expose the 2023 high at 105.883, the last peak, before clearing the way toward 111.000, the double-bottom initial target.

Conversely, the US Dollar Index’s first support would be 100.788. A dip below, and nothing would be in the way toward the 200-week EMA at 99.117.

US Dollar Index Weekly Chart

USD Dollar Index Technical Levels

-

21:33

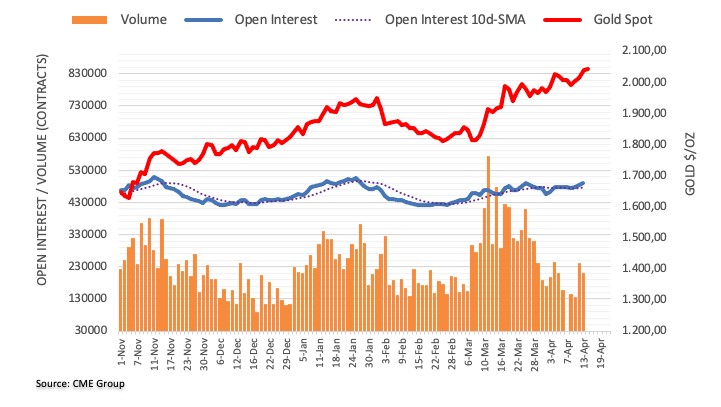

United States CFTC Gold NC Net Positions down to $192.7K from previous $195.2K

-

21:32

Japan CFTC JPY NC Net Positions dipped from previous ¥-57K to ¥-57.2K

-

21:32

United States CFTC S&P 500 NC Net Positions increased to $-307.6K from previous $-321.5K

-

21:32

Australia CFTC AUD NC Net Positions dipped from previous $-27.2K to $-37.9K

-

21:32

European Monetary Union CFTC EUR NC Net Positions: €163.3K vs €143.4K

-

21:32

United States CFTC Oil NC Net Positions increased to 235.6K from previous 226.1K

-

21:31

United Kingdom CFTC GBP NC Net Positions climbed from previous £-14.8K to £-2.4K

-

20:27

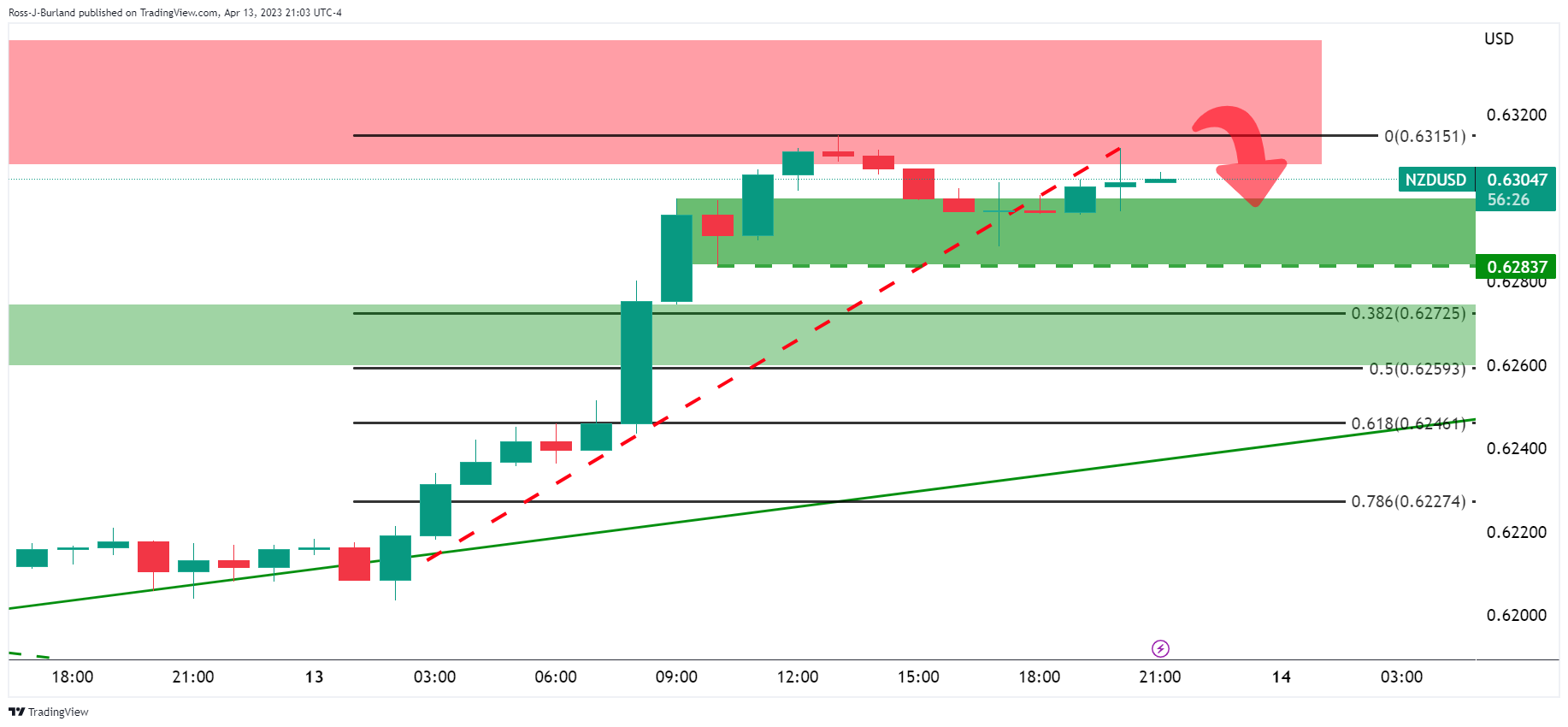

NZD/USD ends two-day gain streak and falls toward 0.6200

- Sentiment deterioration, amidst mixed Fed signals, weakened the NZD.

- Inflation expectations in the United States moved higher, according to Americans.

- NZD/USD traders are eyeing next week’s NZ CPI report.

NZD/USD snapped two days of consecutive gains and slid past the 200, 50, and 100-day Exponential Moving Averages (EMAs) on a risk-off impulse spurred by Fed’s hawkish commentary and expectations for further tightening. US economic data showed further deterioration, but inflation expectations increased the likelihood of another Fed hike past the May meeting. At the time of writing, the NZD/USD is trading at 0.6207, down 1.38%.

The economy in the United States decelerates while inflation expectations arise

Wall Street is set to finish the last trading day of the week with losses. US data in the United States (US) showed that the economy is slowing down, as demonstrated by Retail Sales and Industrial Production. March’s sales dropped 1% MoM, below an anticipated contraction of 0.4%, while YoY figures came at 2.9%, below the prior’s month 5.9%. Meanwhile, Industrial Production (IP) fell for the first occasion in the year and grew 0.4% MoM, below February’s 0.9% reading.

In the meantime, a poll published by the University of Michigan revealed that American consumer sentiment in April improved to 63.5 from the previous reading of 62. The same report flashed that inflation expectations rose to 4.6% from 3.6% in the prior’s report.

Those two reasons drove the NZD/USD price action. As the data was released, the NZD/USD hovered around 0.6260 before collapsing toward the day’s low of 0.6195.

Additionally, to the abovementioned, Federal Reserve officials continued to cross newswires, though they gave mixed signals. Atlanta’s Fed President Raphael Bostic said he favors one more hike, then asses what’s needed in monetary policy. Contrarily, Fed Governor Christopher Waller noted that further tightening is need for a “substantial period and longer than markets anticipate.” Chicago’s President Austan Golsbee said he would focus on tighter credit conditions and lending data regarding his decision for the upcoming May 2-3 meeting.

On the New Zealand (NZ) front, the Business PMIS came at 48.1, below the prior’s month 51.7. Data was mainly ignored by NZD/USD traders, focusing on the following week’s CPI report, with estimates of 1.8% on QoQ Q1 inflation, while YoY is expected to remain at 7.2%.

NZD/USD Technical Levels

-

20:15

USD/CAD: Scope to move lower based on BoC and oil – MUFG

USD/CAD is on its way to the lowest weekly close since February below 1.3400. Analysts at MUFG Bank see that the Canadian Dollar has some scope in the short term to outperform.

Key quotes:

“We have been somewhat cautious over the prospects for CAD and indeed over the year as a whole, we suspect CAD will be a laggard versus most of G10 but taking a short term horizon we do see some scope for CAD to outperform.”

“We don’t expect any additional rate hikes but the resilience of the economy and the BoC’s modestly more hawkish communication this week has helped keep the USCA 2yr swap at levels supportive for further USD/CAD declines.”

“Our rates/crude oil short-term regression model indicates scope for USD/CAD to fall a couple of big figures from here. The IMM analysis below also reveals that CAD shorts are most stretched based on our z-score analysis and that could prompt some CAD buying as well.”

-

20:10

GBP/USD: Can the pound continue to outperform? – MUFG

The strength of the British Pound is reflecting less bad news rather than actual good news, point out analysts at MUFG Bank. They point out that next week UK data (inflation and employment) will be key for the Bank of England.

Key quotes:

“While the pound has performed well this year, data this week may have weighed on near-term performance. The pound is the 3rd worst performing G10 currency this week and the data yesterday looks to be weighing a little on GBP now, with EUR/GBP drifting higher. EUR/GBP is 0.7% higher this week with most of that gain coming since yesterday.”

“The break in GBP/USD above the 1.2500 level which has coincided with the break higher in EUR/USD is significant technically and in circumstances of US dollar sentiment remaining unchanged, there is certainly scope for the move to extend higher, in particular given the lack of conviction behind the move evident in IMM positioning data.”

“A weak set of data next week that changes expectations on a BoE rate hike on 11th May could well undermine GBP performance but that is more likely to be evident versus EUR than against the rest of G10 given many central banks have already moved to a pause and the curve in the US points to aggressive cuts by year-end.”

-

20:02

Argentina Consumer Price Index (MoM) climbed from previous 6.7% to 7.7% in March

-

19:40

Forex Today: Dollar revives, but not out of the woods

Here is what you need to know for next week:

Markets are offering mixed signs amid an uncertain outlook. Not even central bankers know what to do next. After crucial economic data from the US, what is clear is that the economy is softening and inflation is slowing down. Another week went without a banking failure.

The US Dollar staged a strong recovery on Friday, trimming weekly losses. Despite the revival, the trend remains down. Expectations point to one last rate hike by the Federal Reserve (Fed) in May and a long pause, before rate cuts. The bond market sees a recession ahead and, by the end of the year, lower interest rates than the current ones.

Next week, the S&P Global PMIs will offer the first glance of economic activity during April across the globe, an essential report in times of concerns about growth and central banks' "data-dependence". Growth data from China will show the extent of re-opening. The latest export data was encouraging, helping global risk sentiment.

The US Dollar Index dropped for the fifth consecutive week and posted the lowest weekly close since May. The DXY closed above 101.50, far from the lows, a positive sign for the US Dollar that does not suggest a reversal yet, but could point to a consolidation.

As has been the case since late February, EUR/USD rose for another week, and reached the highest level in a year above 1.1000. The trend is still up, but some exhaustion signs are spotted. Eurozone's PMIs next week could be critical for European Central Bank (ECB) expectations. Markets see the ECB raising rates further, but weak numbers could change the outlook for the second half of the year.

GBP/USD ended flat around 1.2400 after retreating from a multi-month high above 1.2500. The deterioration in risk sentiment on Friday weighed on the Pound, which lagged the Euro. EUR/GBP posted the highest weekly close since February above 0.8850. Critical UK data is due next week, with job numbers and consumer inflation.

USD/JPY finished the week little changed, with modest gains near the 133.00 area. The Japanese Yen lost strength amid risk appetite and after hopes for a turnaround in Bank of Japan's (BoJ) monetary policy stance vanished following the first press conference of Kazuo Ueda, the new governor.

USD/CHF continued to slide and broke decisively under 0.9000, to hit the weakest level since January 2021. The Swiss Franc and the Loonie were the top performers in the G10 space. USD/CAD bottomed around 1.3300, the lowest since February, then rebounded to 1.3400, to end the week with a loss of 140 pips. Next week, consumer inflation (Tuesday) and retail sales (Friday) are due in Canada.

When it looked like AUD/USD was ready for a run above 0.6800, it retreated, holding in the familiar range near 0.6700. This week's data showed strength in the labor market. The Reserve Bank of Australia (RBA) is still seen on hold at the next meeting. Next Tuesday, the central bank will release the minutes with details on the decision to pause the tightening cycle.

NZD/USD continued to retreat from the peak at 0.6378, which followed the Reserve Bank of New Zealand (RBNZ) 50 basis point rate hike, and ended near 0.6200. New Zealand's Q1 inflation is due on Thursday.

Latin American currencies were the best weekly performers despite falling on Friday. The Colombian Peso and the Chilean Peso gained more than 2.5% each versus the US Dollar.Gold looked at record highs and blinked, retreating on Friday to $2,000. The trend is still to the upside, but the sharp correction raises doubts about the short-term bullish potential. Silver lost 2% on Friday, trimming some of its weekly gains, but still scoring the fifth advance in a row.

Bitcoin gained 8% during the week and it was holding above $30,000 at the highest level since June 2022.

Like this article? Help us with some feedback by answering this survey:

Rate this content -

19:35

BoC’s Macklem: Officials discussed need for potential hikes at last meeting

Bank of Canada (BoC) Governor, Tiff Macklem mentioned on Friday, that the governing council discussed raising interest rates on Wednesday when they decided to leave them on hold at 4.50%, as expected.

BoC Governor reiterated that interest rates may need to stay at higher levels for a longer period of time to get inflation back to the target. Regarding quantitative tightening, he said that will likely continue amid interest rate normalization, but it could end earlier if the economy needs stimulus.

Macklem is in Washington attending the International Monetary Fund Spring Meeting.

Market reaction

USD/CAD is hovering around 1.3365, up on Friday, but on its way to the lowest weekly close since February. The Loonie outperformed during the week.

-

19:07

AUD/USD reverses course below 0.6700 after hitting resistance at 200-day EMA

- Retail Sales in the United States plunged as Industrial Production decelerated.

- US Consumer Sentiment improved, but the needle on inflation expectations rose.

- AUD/USD Price Analysis: Could test 0.6600 with a daily close below 0.6700.

AUD/USD reverses its course after failing to break the 200-day Exponential Moving Average (EMA) at 0.68099m re-treating beneath 0.6700. economic news from the United States (US), alongside a hawkish tone of US Federal Reserve (Fed) officials, were the driving factors of AUD/USD’s price action. The AUD/USD is trading at 0.6698, down 1.26%.

Risk-off impulse, and US consumer’s higher inflation expectations, bolstered the USD

Sentiment remains deteriorated. US Retail Sales in March dropped 1% MoM, disappointing analysts and indicating a sharper contraction than the anticipated 0.4%. Annual data for the month was 2.9%, falling short of the previous month’s 5.9%. Simultaneously, the Fed disclosed that Industrial Production had decreased for the first time in 2023, expanding only 0.4% MoM, trailing behind February’s 0.9% data and lower than the projected 0.2%. A reduction in durable goods caused a decline in production output.

In April, the University of Michigan (UoM) Consumer Sentiment poll indicated a rise in sentiment from 62 to 63.5. However, there was a 1% increase in inflation expectations for one year, climbing from 3.6% to 4.6%.

Following the UoM report, the AUD/USD extended its losses, as shown by US Treasury bond yields pushing higher, while the US Dollar (USD) jumped from new two-week lows of around 100.788, as portrayed by the US Dollar Index (DXY).

On the Australian front, a solid employment report crushing estimates of 20K, at 53K in March, suggests that although the Reserve Bank of Australia (RBA) paused hiking rates, the RBA might resume its campaign as the Unemployment Rate dipped to 3.5% from 3.6%. In the latest meeting, the RBA’s Governor Philipe Lowe said that the pause did not imply that further increases were off the table and commented that the central bank would be data dependent.

AUD/USD Technical Analysis

Given the backdrop, the AUD/USD plummeted sharply after testing the 200-day EMA. Nevertheless, the fall could be capped by the 20-day EMA at 0.6701, a price level sought by buyers, as the last line of defense. A further decline could pave the way toward the April 13 low at 0.6685, followed by the weekly low at 0.6619.

-

18:07

Colombia Retail Sales (YoY) down to 0.1% in February from previous 1.2%

-

18:07

United States Baker Hughes US Oil Rig Count fell from previous 590 to 588

-

17:19

Silver Price Analysis: XAG/USD hit YTD high at $26.08 but retreated on a bearish-engulfing pattern

- XAG/USD is poised for five consecutive weeks of gains, up 0.81%.

- Silver’s break below $26.00 opened the door for a test of $25.00.

Silver price reached a new YTD high at $26.08, but retraces, as traders booking profits, are forming a bearish-engulfing candle pattern, suggesting that further downside is warranted. Among technical indicators, US economic news and Fed speakers underpinned the US Dollar (USD) to the detriment of the white metal. At the time of typing, the XAG/USD is trading at $25.23, down 2.26%.

XAG/USD Price Action

The XAG/USD is still upward biased from a daily chart perspective. The emergence of a bearish candlestick pattern and the Relative Strength Index (RSI) exiting oversold territory triggered profit-taking in the white metal. Additionally, a negative divergence between XAG/USD’s price action and the Rate of Change (RoC) indicates that buying pressure is waning, exacerbating Silver’s drop below $26.00.

If XAG/USD falls below $25.00, that will pave the way toward the February 2 high at $24.63, the previous resistance turned support, followed by the 20-day Exponential Moving Average (EMA) at $24.20. Once cleared, the psychological $24.00 level would be next.

Conversely, for a bullish continuation, the XAG/USD needs to get above the April 13 low of $25.40, which could motivate XAG buyers to re-enter the market at solid price levels. In that case, the XAG/USD first resistance would be the YTD high at $26.08, followed by April 18, 2022, swing high at $26.21, followed by 2022 high at $26.94.

XAG/USD Daily Chart

XAG/USD Technical Levels

-

16:45

US: Retail sales fell sharply as consumers became more cautious – CIBC

Retail Sales dropped 1% in March in the US, a larger-than-expected contraction. Despite those numbers, analysts at CIBC still see the Federal Reserve raising rates in May, for the last time.

Key quotes:

“US retail sales fell sharply in March as consumers became more cautious, adding to other recent data releases that have signaled a deterioration in activity.”

“The Fed is looking for definitive signs of a cooling in activity and this print is a step in the right direction, but with sales volumes in the control group still 5.8% above their pre-pandemic trend level, this won't prevent a 25bp hike at the May FOMC."

“This data adds to signs of a deterioration in activity that will likely intensify in the second quarter, but the progress in cooling activity won't be enough to prevent a final 25bp Fed hike in May.”

-

16:42

GBP/USD: Risks of dips to 1.20 this year – Rabobank

Analysts at Rabobank see risks of a decline in the GBP/USD pair to 1.20 this year, based on their view that further bouts of Dollar strength are likely.

Key quotes:

“In our view, a move in cable above the 1.26 would likely have to be initiated by further broadbased USD weakness. The market is putting distance between itself and last month’s banking sector jitters.”

“The cautious recovery in sentiment has pushed against the safe haven USD which has also being undermined by market optimism that the Fed may be cutting interest rates before the end of the year to soften recessionary risks. While the USD may retain a softer profile nearterm we see risk of further bouts of USD strength this year.”

“We cannot rule out the risk of further choppy conditions in the USD’s outlook and for choice we maintain the view that the USD will strengthen on a 6 month view. This suggests risks of a drop in cable back to the 1.20 area this year.”

-

16:34

EUR/USD tumbles amid stronger Dollar, drops below 1.1000

- US Dollar strengthens on Friday after US data and Fed talk.

- EUR/USD drops 80 pips from top, but holds firm to weekly gains.

The EUR/USD is losing ground on Friday as the US Dollar recovers a part of recent losses. The pair reached a fresh daily low at 1.0987 moving away from the one-year lows it hit on European hours at 1.1075.

The US Dollar Index (DXY) is up by 0.50% on Friday, hovering around 101.50 following mixed US economic data. Comments from Federal Reserve officials and higher US yields helped the Dollar.

Fed Governor Christopher Waller said that the central bank has not made much progress on the inflation goal and argued rates need to rise further. In an interview with CNBC, Chicago Fed President Austan Goolsbee mentioned that “a mild recession is definitively on the table as a possibility.”

Economic data came in mixed, with lower-than-expected numbers from Retail Sales, but Industrial Production and University of Michigan’s Consumer Sentiment rose more than expected.

Following data and comments, US yields jumped. The 2-year Treasury yield rose from under 4% to 4.10% and the 10-year from 3.45% to 3.52%. Eurozone bond yields are also rising but at a slower pace.

Despite Friday’s reversal, EUR/USD is still on its way to the highest weekly close in a year. It is holding up, however, the retreat from the highs raises doubts about more gains for the next session.

Price is hovering around daily lows at 1.0990. The next support area is seen at 1.0970 followed by 1.0935. On the upside, 1.1040 could become the immediate resistance.

Technical levels

-

16:25

USD/CAD rebounds from weekly lows on Fed speakers’ comments, despite soft US data

- USD/CAD is set to trim some of its weekly losses, with bulls eyeing 1.3400.

- US Retail Sales take a nosedive, plunging 1% MoM in March, while Industrial Production falls for the first time in 2023.

- Inflation expectations for one year in the United States soared 1%, from 3.6% to 4.6%.

The USD/CAD snaps four days of straight losses and bounces from weekly lows around 1.3300 early in the North American session. A tranche of US data flashes the economy is feeling the cumulative tightening by the US Federal Reserve (Fed) while Consumer Sentiment improved. The USD/CAD is trading at 1.3366, above its opening price.

US consumer sentiment improved, but inflation expectations rose

The Canadian Dollar (CAD) encountered headwinds like Fed’s official Christopher Waller saying that more tightening is needed amidst a solid labor market and stickier core inflation on the consumer and producer side. US Retail Sales disappointed analysts and plunged 1% MoM in March, compared to a 0.4% contraction. Annually-based data was 2.9%, below the prior’s month 5.9%.

At the same time, the Fed revealed that Industrial Production in March fell for the first time in 2023, expanding 0.4% MoM vs. estimates of 0.2%, and trailed February’s 0.9% data. Production output dropped due to a pullback in durable goods.

Lately, the University of Michigan (UoM) Consumer Sentiment poll showed an improvement in sentiment in April, up from 62 to 63.5, though inflation expectations for one year jumped 1% from 3.6% to 4.6%. That exacerbated a jump in US bond yields, with the 2-year recovering some ground, jumping 13 basis points, at 4.105%, and underpinning the US Dollar.

The US Dollar Index, a measure of the buck’s value against six currencies, is making a U-turn, up 0.48%, at 101.487.

Another Fed official, Chicago’s President Austan Golsbee, noted that he would focus on tighter credit conditions and lending data regarding his decision for the upcoming May 2-3 meeting. Golsbee added that although inflation is cooling, there is some “clear stickiness: in some price categories.

On the Canadian front, Statistics Canada revealed that manufacturing sales slid 3.6% in February, weighed by sales of petroleum and coal products. Expectations were for a 2.7% plunge, though the slippage in oil and coal products of 14.8% dragged the index lower.

USD/CAD Technical analysis

Given the backdrop, the USD/CAD found some bids before the weekend, though the upward correction toward the 200-day Exponential Moving Average (EMA) at 1.3377 could be short-lived. If USD/CAD buyers reclaim the 200-day EMA, that will expose 1.3400 and could shift the pair’s bias to neutral, with a daily close above the latter. Otherwise, USD/CAD sellers might step in and drag prices towards the YTD low at 1.3262, ahead of falling to 1.3200.

-

16:05

Colombia Industrial output (YoY) rose from previous 0.2% to 0.4% in February

-

15:23

GBP/USD tumbles below 1.2450 as US Dollar strengthens

- US Dollar rises across the board after US data.

- US bond yields and stocks rise despite weaker economic figures.

- GBP/USD erases most of the week’s gains on Friday.

The US dollar is rising sharply on Friday, trimming weekly losses after the release of US economic data. GBP/USD is falling almost a hundred pips on the day, trading at 1.2445.

The pair changed its course after reaching a fresh multi-month high on Asian hours at 1.2546. From the top it dropped more than a hundred pips, and bottomed after Wall Street’s opening bell at 1.2435.

USD shines despite US data

The US Dollar is up across the board, ending a three-day negative streak and recovering from the lowest levels in months. Higher US yields are supporting the Greenback on Friday. The US 10-year yield reached 3.50% and the 2-year is at 4.09%, up by 2.90% for the day.

Data from the US came in mixed. Retail Sales dropped by 1% in March, more than the 0.4% expected. Industrial Production expanded 0.4%, more than the 0.2% forecast. University of Michigan’s Consumer Sentiment Index improved in April to 63.5 from 62.

The key support to the Dollar came from Fed talk. Federal Reserve Governor Christopher Waller said on Friday that the central bank has not made much progress on the inflation goal and said rates need to rise further. In an interview with CNBC, Chicago Fed President Austan Goolsbee argued that “mild recession” is definitively on the table as a possibility.

Technical levels

-

15:05

US: UoM Consumer Confidence Index improves modestly to 63.5 in April vs. 62 expected

- Consumer Confidence Index in the US rose slightly in April.

- US Dollar Index clings to daily recovery gains above 101.00.

Consumer sentiment in the US improved modestly in early April with the University of Michigan's (UoM) Consumer Confidence Index rising to 63.5 (preliminary) from 62 in February. This reading came in better than the market expectation of 62.

"Year-ahead inflation expectations rose from 3.6% in March to 4.6% in April," the UoM further noted. "Uncertainty over short-run inflation expectations continues to be notably elevated, indicating that the recent volatility in expected year-ahead inflation is likely to continue. The bumpiness in inflation expectations is limited to the short run as long-run inflation expectations remained remarkably stable."

Market reaction

The US Dollar Index edged higher with the immediate reaction to this report and was last seen rising 0.3% on the day at 101.30.

-

15:00

United States UoM 5-year Consumer Inflation Expectation remains at 2.9% in April

-

15:00

United States Michigan Consumer Sentiment Index above forecasts (62) in April: Actual (63.5)

-

15:00

United States Business Inventories registered at 0.2%, below expectations (0.3%) in February

-

14:49

US: Consumer spending gradually losing momentum – Wells Fargo

Data released on Friday showed a larger-than-expected decline in US Retail Sales in March. According to analysts at Wells Fargo, the level of spending remains elevated, demonstrating there remains an underlying resilience among consumers.

Retail Sales slip again after unusually strong start to year

“But even with some payback after an unusually strong start to the year, the level of retail spend is still nearly 2% ahead of where it was in December. More plainly, consumers continue to spend at an elevated level, though the momentum appears to be downshifting.”

“The March retail sales data demonstrate continued reversal after an unusually strong gain in January sales. Consumers' appetite continues to shift away from goods, particularly those that come with a high price tag or typically require financing. The rise in borrowing costs over the past year may be starting to bite consumers desire to take on credit card debt or purchase a new auto or appliance.”

“Lost momentum and the slow end to the first quarter for retail positions for a weak second quarter of spending. We anticipate consumer spending continues to gradually lose momentum through Q2 before growth slips negative later this year.”

-

14:43

Gold Price Forecast: XAU/USD recedes from tops near $2050

- Gold prices correct lower after three daily gains in a row.

- The dollar’s rebound along with higher yields weigh on bullion.

- US Retail Sales surprised to the downside in March.

Following new 2023 highs near the $2050 mark per ounce troy as well as a 3-day positive streak, the precious metal embarked on a corrective decline which has so far met initial contention near $2015 on Friday.

Corrective drop triggered by USD, yields

The so far daily retracement in the yellow metal came in response to the rebound in the greenback after the USD Index (DXY) sank to new 2023 lows in the 100.80/75 band earlier in the European session. Also weighing on bullion appears the moderated bounce in US yields across the curve, at the time when investors continue to price in a 25 bps rate hike by the Fed at the May 3 gathering.

According to CME Group’s FedWatch Tool, the probability of the above-mentioned scenario hovers around the 80%, from around 40% a month ago.

Gold price technical outlook

If gold surpasses the so far 2023 peak at $2048 (April 13) it could then open the door to a probable move to the 2022 high at $2070 (March 8), which lies just ahead of the all-time top at $2075 (August 7 2020). Bears, in the meantime, should clear the minor support at the weekly low at $1981 (April 10) to spark a deeper retracement to the April low at $1949 (April 3) ahead of another weekly low at $1934 (March 22). Further losses could put the 55- and 100-day SMAs at $1909 and $1874, respectively, back on the traders’ radar prior to the March low at $1809 (March 8) and the 2023 low at $1804 (February 28).

-

14:25

US: Industrial Production rises by 0.4% in March vs. 0.2% expected

- Industrial Production in the US grew at a stronger pace than expected in March.

- US Dollar Index stays in positive territory above 101.00.

Industrial Production in the US expanded by 0.4% in March following February's increase of 0.2% (revised from 0%), the US Federal Reserve reported on Friday. This reading came in slightly better than the market expectation for a growth of 0.2%.

"In March, manufacturing and mining output each fell 0.5 percent," the Fed further noted in its publication. "Capacity utilization moved up to 79.8 percent in March, a rate that is 0.1 percentage point above its long-run (1972–2022) average."

Market reaction

The US Dollar stays resilient against its rivals after this report and the US Dollar Index was last seen rising 0.2% on the day at 101.22.

-

14:18

China: Exports surged in March – UOB

Economist at UOB Group Ho Woei Chen reviews the latest trade balance figures in China.

Key Takeaways

“Exports unexpectedly surged in Mar while imports were less robust but still came in above consensus’ expectation. China’s shipments improved amid the normalisation of domestic production and stronger demand from the Asian and European markets.”

“In volume terms, China’s imports of commodities such as crude and refined petroleum, LPG, coal and iron ore were strong compared to the year-ago period which is an indication of inventory rebuilding, pick-up in construction activity and concerns over energy shortages particularly as domestic demand rebounds. Commodity imports are expected to continue benefiting from domestic demand recovery and stronger construction activities ahead.”

“In 1Q23, exports rose 0.5% y/y while imports contracted by 7.1% y/y. Despite the strong export data, we are less convinced of a sustained improvement in China’s export outlook as global demand has remained sluggish with an upturn only expected in the later part of this year.”

“Overall, we maintain our forecast for China’s export to register a contraction of 3.0% this year while imports may see a small gain of around 2.0% in 2023 as domestic demand recovers.”

-

14:15

United States Industrial Production (MoM) came in at 0.4%, above forecasts (0.2%) in March

-

14:15

United States Capacity Utilization above expectations (79%) in March: Actual (79.8%)

-

14:02

EUR/USD Price Analysis: Outlook keeps pointing to extra gains near term

- EUR/USD clinches new YTD peak before sparking a corrective decline.

- The continuation of the uptrend could revisit the round level at 1.1100.

EUR/USD deflates from earlier 2023 highs around 1.1075 at the end of the week.

Despite the knee-jerk, the pair’s outlook keeps favouring the continuation of the uptrend for the time being. Against that, the surpass of the YTD high at 1.1075 (April 14) could then dispute the round level at 1.1100 prior to the weekly high at 1.1184 (March 21 2022).

Looking at the longer run, the constructive view remains unchanged while above the 200-day SMA, today at 1.0368.

EUR/USD daily chart

-

13:52

USD/JPY jumps above 133.00 after weak US Retail Sales

- US dollar gains momentum after US retail sales data.

- Data comes in below expectations but triggers dollar’s correction.

- USD/JPY bounces almost a hundred pips.

The USD/JPY rose sharply after the release of US economic data and climbed to 133.18, hitting a fresh daily high. The Greenback appreciated across the board despite a larger-than-expected slide in March Retail Sales.

US data below expectations

Retail Sales drooped 1% in March, against the consensus of a 0.4% slide; following a 0.2% decline (revised from -0.4%) in February. Sales excluding autos fell by 0.8% in March, more than the decline expected of 0.3%.

The Import Price Index fell at an annualized rate of 4.6%, more than the 3.7% of market consensus, and the Export Price Index fell by 4.8%, more than the 4.2% slide expected.

The latest economic figures suggest some weakness in demand and also diminishing inflation pressures. However, the immediate reaction following US Retail Sales triggered a bullish correction of the US Dollar across the board. US yields rose sharply, probably amid expectations of even weaker-than-expected figures. Wall Street futures remain in positive ground. The Japanese Yen printed fresh lows versus its main rivals.

The USD/JPY initially dropped to 132.17 and then bounced almost a hundred pips in a few minutes. It is trading at 133.10, at daily highs. The next resistance level is seen on Thursday’s high at 133.40. On the flip side, now 132.80 is the immediate support.

Technical levels

-

13:51

Fed's Waller: Fed hasn't made much progress on inflation goal, rates need to rise further

Federal Reserve Governor Christopher Waller argued on Friday that the recent data show that the Fed hasn't made much progress on its inflation goal and added that rates need to rise further, as reported by Reuters.

Key takeaways

"Extent of further increases depends on incoming data, credit tightening."

Still uncertain how SVB failure, bank stress, will impact broader credit conditions."

"Monetary policy will need to remain tight for a substantial period, and longer than markets anticipate."

"First quarter 2023 data continue to surprise with stronger growth, job creation."

"Significant credit tightening could offset need for rate hikes, but judgment difficult in real time."

"Developments so far validate decision to raise rates at last meeting, but continuing to watch data even more closely than usual."

"Liquidity steps taken after SVB failure appear to have succeeded in stabilizing the banking system."

Market reaction

The US Dollar benefits from these hawkish comments and the US Dollar Index was last seen rising 0.3% on the day at 101.30.

-

13:47

Fed’s Goolsbee: Mild recession is definitely on the table as a possibility

In an interview with CNBC on Friday, Federal Reserve Bank of Chicago President Austan Goolsbee said that a mild recession in the US was definitely on the table as a possibility, as reported by Reuters.

Additional takeaways

"When you have financial tightening occurring, that does the work of monetary policy."

"We still have several weeks before May meeting."

"I don't want to comment yet on what I am for at that meeting; still want to see the data."

"But let's be mindful we've raised a lot; some of the lag is coming through possibly in today's retail sales number."

"Inflation is coming down, still got clear stickiness on some inflation."

"Producer prices and retail sales show we are moving in right direction."

"I am focused on what is happening with credit conditions."

"We are spending too much time looking at wage growth as an indicator of prices."

"Wages do not serve as a leading indicator for inflation."

"We need to keep eye on prices series, not wages."

"I am going to spend next few weeks figuring out amount of credit tightening going on."

Market reaction

The US Dollar Index extends its recovery in the early American session after these comments and was last seen rising 0.3% on the day at 101.30.

-

13:32

Breaking: US Retail Sales decline by 1% in March vs. -0.4% expected

The data published by the US Census Bureau revealed on Friday that Retail Sales in the United States declined 1% on a monthly basis in March to $691.7 billion. This reading followed February's contraction of 0.2% (revised from -0.4%) came in worse than the market expectation for a decrease of 0.4%.

Retail Sales Ex-Autos fell by 0.8% in the same period, compared to analysts' estimate of -0.3%.

"Retail trade sales were down 1.2% from February 2023, but up 1.5% above last year," the publication further read. "Nonstore retailers were up 12.3% from last year, while food services and drinking places were up 13.0% from March 2022."

Market reaction

Following a quick decline with the immediate market reaction, the US Dollar Index reversed its direction and was last seen rising 0.15% on the day at 101.15.

-

13:31

United States Export Price Index (YoY) below expectations (-4.2%) in March: Actual (-4.8%)

-

13:31

United States Retail Sales (MoM) came in at -1%, below expectations (-0.4%) in March

-

13:31

United States Import Price Index (YoY) came in at -4.6%, below expectations (-3.7%) in March

-

13:30

United States Retail Sales ex Autos (MoM) came in at -0.8% below forecasts (-0.3%) in March

-

13:30

Canada Manufacturing Sales (MoM) below forecasts (-2.7%) in February: Actual (-3.6%)

-

13:30

United States Import Price Index (MoM) below expectations (-0.1%) in March: Actual (-0.6%)

-

13:30

United States Export Price Index (MoM) below forecasts (-0.1%) in March: Actual (-0.3%)

-

13:30

United States Retail Sales Control Group below forecasts (0.6%) in March: Actual (-0.3%)

-

13:14

AUD/USD flat-lines below 0.6700 mark, eyes US macro data for a fresh impetus

- AUD/USD stalls this week’s bullish trend near the 100-day SMA, just ahead of the 0.6700 mark.

- A modest USD recovery from a one-year high turns out to be a key factor acting as a headwind.

- Expectations for an imminent Fed rate-hike pause to cap the USD and lend support to the pair.

The AUD/USD pair struggles to capitalize on its weekly gains recorded over the past three sessions and seesaws between tepid gains/minor losses heading into the North American session on Friday. The pair, however, trades just a few pips below its highest level since February 24 touched on Thursday and is currently placed around the 0.6770-0.6775 area, nearly unchanged for the day.

A modest US Dollar (USD) bounce from a one-year low touched earlier this Friday is seen as a key factor acting as a headwind for the AUD/USD pair. The upside for the Greenback, however, remains capped amid firming expectations that the Federal Reserve (Fed) will pause its rate-hiking cycle amid signs of cooling inflationary pressures in the US. The bets were lifted by this week's release of softer consumer inflation figures and the Producer Price Index, which suggested that disinflation is progressing smoothly.

Apart from this, a generally positive risk tone might contribute to gains for the safe-haven buck and lend support to the risk-sensitive Aussie. Apart from this, the upbeat Australian jobs data on Thursday

revived bets for a 25 bps rate hike at the next Reserve Bank of Australia (RBA) meeting in May and supports prospects for the emergence of some dip-buying around the AUD/USD pair. That said, bulls might wait to move beyond the 100-day Simple Moving Average (SMA), around the 0.6700 mark, before placing fresh bets.Market participants now look forward to the US economic docket, featuring the release of monthly Retail Sales figures and the Preliminary Michigan Consumer Sentiment Index. This, along with the US bond yields and the broader market risk sentiment, might influence the USD price dynamics and provide some impetus to the AUD/USD pair. Nevertheless, spot prices remain on track to register strong weekly gains.

Technical levels to watch

-

12:41

When are US monthly Retail Sales figures and how could they affect EUR/USD?

US Monthly Retail Sales Overview

Friday's US economic docket highlights the release of monthly Retail Sales figures for March, due later during the early North American session at 12:30 GMT. The headline sales are expected to contract by 0.4% for the second straight month, while core sales, excluding automobiles, probably declined by 0.3% in March as compared to the 0.1% fall in the previous month. However, the downbeat expectations strengthen the case for an upside surprise.

According to Yohay Elam, Senior Analyst at FXStreet: “The relentless American consumer has a relatively low bar to pass, which may even be lower. The US retail sales report is highly important and will determine the closing moves of the week. I expect a small beat of the downbeat estimates, resulting in an ephemeral increase for the US Dollar, and an extension of the gradual gains in stocks.”

How Could It Affect EUR/USD?

Ahead of the key release, a modest US Dollar (USD) recovery from a one-year low keeps a lid on the EUR/USD pair's intraday uptick to the 1.1075 area, or the highest level since April 2022. A stronger US macro data could strengthen the USD further, though the immediate market reaction is likely to remain limited amid growing acceptance that the Federal Reserve (Fed) is nearing the end of its rate-hiking cycle.

Conversely, any disappointment from the US Retail Sales figures will reaffirm bets that the Fed will start cutting rates towards the end of the year, which should trigger a fresh leg down for the USD. This, in turn, suggests that the path of least resistance for the EUR/USD pair is to the upside and any meaningful pullback is more likely to attract fresh buyers at lower levels and remain limited.

Meanwhile, Eren Sengezer, Editor at FXStreet, offers a brief technical outlook and writes: “EUR/USD climbed out of the ascending regression channel and the Relative Strength Index (RSI) indicator on the four-hour chart rose toward 80, pointing to overbought conditions.”

Eren also outlines important technical levels to trade the EUR/USD pair“In case the pair stages a correction and returns within the ascending channel, 1.1020 (mid-point of the channel), 1.1000 (psychological level, static level) and 1.0970 (20-period Simple Moving Average (SMA)) align as support levels.”

“On the upside, 1.1100 (psychological level) aligns as the next bullish target ahead of 1.1150 (static level from March 2022),” Eren adds further.

Key Notes

• US Retail Sales Preview: Dollar set to jump above low barrier of expectations, three scenarios

• EUR/USD Forecast: Can Euro extend the rally?

• EUR/USD faces the next target at 1.1120 – UOB

About US Retail Sales

The Retail Sales released by the US Census Bureau measures the total receipts of retail stores. Monthly per cent changes reflect the rate of changes in such sales. Changes in Retail Sales are widely followed as an indicator of consumer spending. Generally speaking, a high reading is seen as positive (or bullish) for the USD, while a low reading is seen as negative (or bearish).

-

12:31

India FX Reserves, USD climbed from previous $578.45B to $584.76B in April 7

-

12:25

USD Index Price Analysis: A drop to 100.00 should not be ruled out

- DXY retreats further and prints fresh 2023 lows near 100.80.

- A deeper retracement could see the key 100.00 mark revisited.

DXY attempts a mild bounce off earlier 2023 lows in the 100.80/75 band at the end of the week.

If bears remain in control, the index could accelerate losses and put the psychological 100.00 mark to the test in the relatively short-term horizon. The loss of this region exposes a potential move to the late-March 2022 lows near 97.70.

Looking at the broader picture, while below the 200-day SMA, today at 106.36, the outlook for the index is expected to remain negative.

DXY daily chart

-

12:16

EUR/JPY Price Analysis: Next up-barrier emerges at the 2022 peak

- EUR/JPY remains well bid and trades close to the 147.00 region on Friday.

- The next target of note comes at the 2022 peak above 148.00.

The bid bias in EUR/JPY remains well and sound for yet another session at the end of the week.

Considering the ongoing price action, further gains in the cross remain in the pipeline for the time being. That said, the continuation of the upside momentum could extend further and challenge the 2022 peak at 148.40 (October 21) sooner rather than later.

So far, further upside looks favoured while the cross trades above the 200-day SMA, today at 142.02.

EUR/JPY daily chart

-

12:11

US: Inflation and FOMC Minutes till favour further tightening – UOB

UOB Group’s Head of Research Suan Teck Kin and Senior Economist Alvin Liew assess the latest US inflation figures and the FOMC Minutes.

Key Takeaways

“US headline consumer price index (CPI) increased by 0.1% m/m, 5.0% y/y in Mar (from 0.4% m/m, 6.0% y/y in Feb), slightly below Bloomberg’s survey and was also the lowest y/y headline reading since May 2021. However, core CPI (which excludes food and energy) proved to be stickier, as it rose sequentially at a faster m/m pace than the headline, at 0.4%, (from 0.5% in Feb). On a y/y basis, the Mar core CPI rose slightly faster to 5.6% (Feb: 5.5%).”

“US Inflation Outlook – For the full year, we still expect both headline and core inflation to average 3.0% in 2023, above the Fed’s 2% objective. But the 1Q CPI data showed that the balance of risk for US inflation remains on the upside as reflected by the persistent rise of shelter costs, still elevated food costs and components within core and services inflation remain elevated and rising.”

“Mar FOMC Minutes – Fed officials scaled back rate hike expectations this year due to the financial sector turmoil and monitoring for signs of a credit crunch. That said, Fed policymakers still raised their benchmark lending rate by 25-bps to a range of 4.75% to 5.00% in Mar, as they sought to balance the risk of a credit crunch with incoming data showing price pressures remained elevated. And furthermore, they did so even after taking into account that Fed staff economists were forecasting a “mild recession” later this year with recovery over the next two years.”

“FOMC Outlook – If our base case of no systemic impact on the US financial sector remains valid, it is reasonable to expect the US Fed to continue to stay focused on fighting inflation and push forward with its rate hike cycle. Thus, we will continue to assign a high probability the Fed will hike rates by a final 25bps to 5.00-5.25% at the upcoming May FOMC. We expect no rate cuts this year and this terminal rate of 5.25% to last through 2023.”

-

11:51

Gold Price Forecast: XAU/USD consolidates just below YTD peak ahead of US macro data

- Gold price enters a bullish consolidation phase near a fresh one-year high touched on Friday.

- Expectations for an imminent pause in the Federal Reserve's rate-hiking cycle lend support.

- The prevalent US Dollar selling bias further contributes to limiting the downside for the metal.

Gold price consolidates its recent gains to a fresh one-year high and seesaws between tepid gains/minor losses through the first half of the European session on Friday. The XAU/USD is currently placed around the $2,040 area and seems poised to prolong its recent upward trajectory witnessed over the past month or so.

Weaker US Dollar continues to underpin Gold price

The US Dollar (USD) languishes near its lowest level since April 2022 amid expectations that the Federal Reserve (Fed) will pause its rate-hiking cycle. This, in turn, is seen as a key factor acting as a tailwind for the US Dollar-denominated Gold price. Market participants now seem convinced that the Fed will be done with its policy tightening after hiking one last time in May in the wake of signs of easing inflationary pressures in the United States (US).

In fact, the US Producer Price Index (PPI) released on Thursday showed that US inflation at the wholesale level continued its downward slide and cooled dramatically in March. This comes on the back of the softer US Consumer Price Index (CPI) report on Wednesday and indicates that disinflation is progressing smoothly. Other data indicated that Jobless Claims rose more than expected last week, to the highest level since January 15, 2022.

Bets for an imminent pause by Federal Reserve also lend support

This was seen as a sign that labor market conditions were loosening up as higher borrowing costs continue to dampen demand in the economy, which should allow the Fed to pause after hiking one last time in May. Moreover, the March Federal Open Market Committee (FOMC) meeting minutes released on Wednesday revealed that several policymakers considered pausing interest rate increases after the failure of two regional banks.

Furthermore, Atlanta Fed president, Raphael Bostic, told Reuters this Friday that the recent developments are consistent with one more hike. This acts as a headwind for the US Treasury bond yields, which, in turn, keeps the USD bulls on the defensive and further acts as a tailwind for the non-yielding Gold price. Apart from this, a generally weaker tone around the equity markets is seen driving some haven flows towards the precious metal.

Looming recession risks further benefit the safe-haven XAU/USD

The International Monetary Fund (IMF) earlier this week trimmed its 2023 global growth outlook, citing the impact of higher interest rates. This, along with worries that the post-COVID recovery in China is losing steam, fuels recession fears and tempers investors' appetite for riskier assets. This, in turn, lends some support to traditional safe-haven assets, including the XAU/USD, and supports prospects for a further near-term appreciating move.

Traders now eye macro data from United States for a fresh impetus

That said, the slightly oversold Relatively Strength Index (RSI) on the daily chart is holding back traders from placing fresh bearish bets around the USD and acting as a headwind for the Gold price. Traders also prefer to wait on the sidelines ahead of Friday's US macro releases, monthly Retail Sales figures and the Preliminary Michigan Consumer Sentiment Index, which might influence the USD price dynamics and provide some impetus to the XAU/USD.

Gold price technical outlook

From a technical perspective, nothing seems to have changed for Gold price and the near-term bias remains tilted firmly in favour of bullish traders. Hence, some follow-through strength back towards retesting the all-time high, around the $2,070-$2,075 region, looks like a distinct possibility. On the flip side, any meaningful pullback could find decent support near the $2,020 area ahead of the $2,014-$2,013 region. The dip, however, is likely to attract fresh buyers near the $2,000 psychological mark, which should help limit losses for the XAU/USD near the $1,990-$1,980 horizontal support.

Key levels to watch

-

11:42

ECB's Lagarde: Inflation to continue to fall as lagged price pressures fade out

European Central Bank (ECB) President Christine Lagarde said on Friday that she expects inflation in the Euro area to continue to fall with lagged price pressure fading out, as reported by Reuters.

"Historically high wage growth, related to tight labour markets and compensation for high inflation, will support core inflation over the projection horizon, as it gradually returns to rates around our target," Lagarde further noted in her prepared statement delivered at the IMF spring event.

Market reaction

The EUR/USD pair showed no immediate reaction to these comments and it was last seen rising 0.1% on a daily basis at 1.1060.

-

11:33

USD/CNH risks extra losses below 6.8500 – UOB

Markets Strategist Quek Ser Leang and Senior FX Strategist Peter Chia at UOB Group suggest a deeper drop in USD/CNH is likely on a sustainable breach of 6.8500.

Key Quotes

24-hour view: “We expected USD to edge lower yesterday. However, we noted the mild downward momentum and held the view that any decline is unlikely to challenge 6.8500. USD dropped to a low of 6.8672 in NY trade. Downward momentum has improved, albeit not much. Today, USD is likely to trade with a downward bias but a clear break below 6.8500 is unlikely. Resistance is at 6.8780, followed by 6.8850.”

Next 1-3 weeks: “Our most recent narrative from Monday (10 Apr, spot at 6.8800) wherein we held the view that USD is likely to trade sideways between 6.8500 and 6.9200 for now. There is no change in our view for now even though, downward momentum is showing tentative signs of building. However, USD has to break clearly below 6.8500 before a sustained decline is likely. The likelihood of USD breaking below 6.8500 will increase in the next few days as long as USD stays below 6.9000.”

-

11:12

Fed's Bostic: Recent developments are consistent with one more rate hike in May

Atlanta Federal Reserve (Fed) President, Raphael Bostic, in an interview with Reuters this Friday, said that the recent developments are consistent with one more rate hike.

Additional quotes:

That can allow the Fed to pause and reassess.

We've got a lot of momentum suggesting that we're on the path to the 2% inflation target.

Still need to assess the economy, and inflation path to avoid unnecessary economic damage.

Rate increases in the past year now only starting to 'bite'; full impact may take some time.

Market reaction

The comments do little to influence the US Dollar (USD), which is seen languishing near a one-year high amid growing acceptance of an imminent pause in the Fed rate-hiking cycle.

-

11:00

US Dollar under pressure, Brazil’s Lula urges countries to ditch USD in trade

- US Dollar is struggling to find demand ahead of the weekend amid weak US data.

- Brazil President does not want to use US Dollar in international trade transaction.

- EUR/USD technical outlook shows that the pair could stage a technical correction in the short term.

The US Dollar (USD) stays on the back foot ahead of the weekend after having suffered large losses against its major rivals throughout the week. Soft inflation data from the United States, growing expectations for a Federal Reserve policy shift amid signs of economic slowdown and loudening calls to move away from the USD in trade transactions have been causing the currency to lose its value.

The US Dollar Index, which tracks the USD performance against a basket of six major currencies, touched its lowest level in over a year below 101.00 and is yet to stage a rebound.

Daily digest market movers: US Dollar eyes key US data releases

- While speaking at the inauguration ceremony of President Dilma Rousseff at the New Development Bank – formerly known as the BRICS bank – in Shanghai, Brazil President Luiz Inacio Lula Da Silva questioned why all countries have to use the US Dollar in their trade transactions. "Why can't a bank like BRICS have a currency that can finance the trade relationship between Brazil and China, between Brazil and other BRICS countries?" said Lula, adding to growing calls to look for an alternative currency to trade with.

- The US Census Bureau will release Retail Sales data for March, which is forecast to show a 0.4% contraction on a monthly basis.

- The Fed will publish Industrial Production figures for March and the University of Michigan’s will release the preliminary Consumer Sentiment Survey for April.

- The CME Group FedWatch Tool's probability for one more 25 basis points Fed rate increase in May holds near 70%. However, markets see a 90% chance that the Fed will lower its policy rate back to the range of 4.75%-5% by September, even if it opts for a rate hike at the upcoming meeting.

- The US Department of Labor's weekly publication revealed on Thursday that there were 239,000 Initial Jobless Claims in the week ending April 8, up from 228,000 in the previous week.

- The US Bureau of Labor Statistics (BLS) reported on Wednesday that the Consumer Price Index (CPI) declined to 5% on a yearly basis in March from 6% in February. This reading came in below the market expectation of 5.2%. Furthermore, the Core CPI, which excludes volatile food and energy prices, rose by 0.4% on a monthly basis, down from a 0.5% increase recorded in February.

- On Thursday, the BLS announced that the Producer Price Index (PPI) for final demand in the US declined to 2.7% on a yearly basis in March from 4.9% in February (revised from 4.6%). On a monthly basis, the PPI and the Core PPI came in at -0.5% and -0.1%, respectively, triggering a fresh leg of USD selloff.

- Commenting on the CPI inflation data, "the beginning of the end of rate hikes – or the beginning of the countdown toward slashing borrowing costs? That seems to be the message from markets, which are rushing forward to price the next moves of the Federal Reserve (Fed)," noted FXStreet analyst Yohay Elam. "The world's largest economy is experiencing a "process of disinflation" that is somewhat frustrating but is on the right track. Markets are buying it."

- San Francisco Federal Reserve Bank President Mary Daly said on Wednesday that the strength of the US economy and elevated inflation suggests that they have more work to do on rate hikes.

- Earlier in the week, NY Fed’s latest consumer survey revealed that the one-year inflation expectation climbed to 4.7% in March from 4.2% in February.

- NY Fed President John Williams argued on Monday that the pace of Fed rate increases was not behind the issues surrounding the two collapsed banks back in March. On Tuesday, "we've gotten policy to a restrictive stance, now we need to watch the data on retail sales, CPI and others," Williams stated.

- The US Bureau of Labor Statistics reported on Friday, April 7, that Nonfarm Payrolls in the US rose by 236,000 in March, slightly below the market expectation of 240,000. February’s print of 311,000 got revised higher to 326,000 from 311,000.

- Wage inflation in the US, as measured by Average Hourly Earnings, declined to 4.2% on a yearly basis from 4.6% in February. The Unemployment Rate ticked down to 3.5% with the Labor Force Participation Rate improving to 62.6% from 62.5%.

Technical analysis: US Dollar could limit losses against Euro in near term

EUR/USD extended its rally on Thursday and touched its highest level since early April above 1.1050. The pair seems to have gone into a consolidation phase early Friday and the near-term technical outlook suggests that the pair is about to turn overbought with the Relative Strength Index (RSI) indicator on the daily chart holding near 70.

In case EUR/USD pair stages a technical correction, 1.1000 (psychological level, former resistance) aligns as initial support before 1.0900 (20-day Simple Moving Average (SMA) and 1.0750 (50-day SMA).

On the upside, first resistance is located at 1.1100 (psychological level, static level) before 1.1160 (static level from April 2022) and 1.1200 (psychological level).

How does Fed’s policy impact US Dollar?

The US Federal Reserve (Fed) has two mandates: maximum employment and price stability. The Fed uses interest rates as the primary tool to reach its goals but has to find the right balance. If the Fed is concerned about inflation, it tightens its policy by raising the interest rate to increase the cost of borrowing and encourage saving. In that scenario, the US Dollar (USD) is likely to gain value due to decreasing money supply. On the other hand, the Fed could decide to loosen its policy via rate cuts if it’s concerned about a rising unemployment rate due to a slowdown in economic activity. Lower interest rates are likely to lead to a growth in investment and allow companies to hire more people. In that case, the USD is expected to lose value.

The Fed also uses quantitative tightening (QT) or quantitative easing (QE) to adjust the size of its balance sheet and steer the economy in the desired direction. QE refers to the Fed buying assets, such as government bonds, in the open market to spur growth and QT is exactly the opposite. QE is widely seen as a USD-negative central bank policy action and vice versa.

-

10:35

USD/JPY now faces some near-term consolidation – UOB

USD/JPY is likely to navigate within the 131.20-133.70 range in the next weeks, note Markets Strategist Quek Ser Leang and Senior FX Strategist Peter Chia at UOB Group.

Key Quotes

24-hour view: “We expected USD to trade in a range of 132.60/133.70 yesterday. However, USD dropped sharply to 132.01 and then rebounded. Despite the rebound, the weakness in USD has not stabilized. USD has scope to test 132.00 again before a sustained recovery is likely. On the upside, a breach of 133.25 (minor resistance at 132.90) would indicate that the weakness has stabilized.”

Next 1-3 weeks: “Yesterday (13 Apr, spot at 133.10), we noted that ‘upward momentum is beginning to fade and the odds of USD rising to 134.40 are diminishing’. We added, ‘only a break of 132.20 would indicate that USD is not strengthening further’. USD dropped to a low of 132.01 in NY trade. The breach of the ‘strong support’ at 132.20 indicates that the USD strength that started early this week has ended. USD appears to have moved into a consolidation phase and is likely to trade between 131.20 and 133.70 for now.”

-

10:33

PBOC: Will step up support to expand domestic demand

The People’s Bank of China (PBOC) said in a statement on Friday, they “will step up support to expand domestic demand.”

Additional takeaways

“Will make prudent monetary policy precise and forceful.”

“Will keep liquidity reasonably ample.”

“Will better use overall and structural policy tools.“

“Will stabilize growth, stabilize employment and prices.”

“Will deepen exchange rate reform, increase the flexibility of Yuan.”

“Will further improve monetary policy transmission mechanism.”

Related reads

- PBOC’s Yi: Expect China’s GDP this year to grow around 5%

- AUD/USD faces upside risks in the near term – UOB

-

10:20

USD/CAD consolidates its recent losses to two-month low, holds above 1.3300 mark

- USD/CAD drifts lower for the fifth straight day and drops to a fresh two-month low on Friday.

- Expectations for an imminent Fed rate-hike pause weigh on the USD and exert some pressure.

- A modest downtick in Oil prices undermines the Loonie and limits the downside for the major.

The USD/CAD pair enters a bearish consolidation phase and oscillates in a narrow range near a fresh two-month low touched earlier this Friday. The pair trades around the 1.3325-1.3330 region through the first half of the European session and remains in the negative territory for the fifth successive day.

The US Dollar (USD) drops to a one-year low amid growing acceptance that the Federal Reserve (Fed) is nearly done with its rate-hiking cycle and turns out to be a key factor exerting some pressure on the USD/CAD pair. In fact, the markets now seem convinced that the US central bank will pause after hiking one last time next month. The bets were lifted by the incoming US macro data, which pointed to signs of easing inflationary pressures.

Moreover, the March FOMC meeting minutes released on Wednesday showed that several policymakers considered pausing interest rate increases after the failure of two regional banks. This continues to act as a headwind for the US Treasury bond yields and is seen weighing on the Greenback. That said, a generally weaker tone around the equity markets helps limit losses for the safe-haven buck and lends some support to the USD/CAD pair.

The International Monetary Fund (IMF) earlier this week trimmed its 2023 global growth outlook, citing the impact of higher interest rates. This, along with worries that the post-COVID recovery in China is losing steam, raised recession fears and keep a lid on the optimism witnessed since the beginning of this week. Apart from this, softer Crude Oil prices undermine the commodity-linked Loonie and act as a tailwind for the USD/CAD pair.

Investors remain concerned that a deeper global economic downturn will dent fuel demand, which, in turn, drags Oil prices away from a fresh YTD peak touched on Wednesday. That said, a surprise decision last week by OPEC+ to cut output lends some support to the black liquid. This, along with the Bank of Canada's (BoC) readiness to raise borrowing costs again if needed to restore price stability, limits losses for the Canadian Dollar.

The aforementioned fundamental backdrop suggests that the path of least resistance for the USD/CAD pair is to the downside. The negative outlook is reinforced by the overnight breakdown through a multi-month-old ascending trend-line support and a technically significant 200-day Simple Moving Average (SMA). Hence, any attempted recovery might still be seen as a selling opportunity and runs the risk of fizzling out rather quickly.

Market participants now look forward to the US economic docket, featuring the release of monthly Retail Sales figures and the Preliminary Michigan Consumer Sentiment Index later during the early North American session. This, along with the US bond yields, will drive the USD demand and provide some impetus to the USD/CAD pair. Apart from this, traders will take cues from Oil price dynamics to grab short-term opportunities.

Technical levels to watch

-

09:57

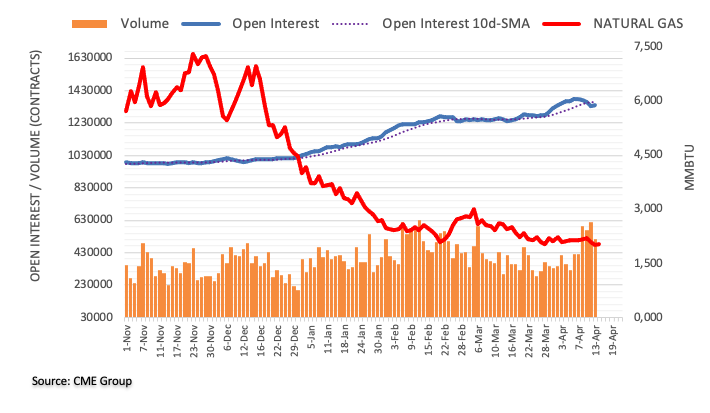

Natural Gas Futures: Extra losses in the pipeline

In light of advanced figures from CME Group for natural gas futures markets, open interest rose by nearly 8K contracts after fourth consecutive daily pullbacks on Thursday. Volume, on the other hand, shrank by around 101.3K contracts and reversed the previous daily build.

Natural Gas: Rising bets for another test of the sub-$2.00 area

Prices of the natural gas closed Thursday’s session just above the key $2.00 mark. The daily retracement was amidst rising open interest and opens the door to further weakness in the short-term horizon, and always with the immediate target at the 2023 low at $1.97 per MMBtu (February 22).

-

09:51

German Economy Ministry: Economy expected to avert recession

According to an Economy Ministry report published on Friday, the German economy is seen narrowly skirting a recession in the first quarter of the year.

Key takeaways

"A technical recession of two negative quarters in a row appears to have been averted.”

“Current forecasts also predict a slight year-on-year increase in gross domestic product (GDP) for 2023 as a whole.”

Market reaction

Despite upbeat remarks, EUR/USD is unable to capitalize, as it is consolidating its rally to fresh 13-month highs of 1.1076. The pair is trading at 1.1061, up 0.16% on the day.

-

09:48

AUD/USD faces upside risks in the near term – UOB

In the opinion of Markets Strategist Quek Ser Leang and Senior FX Strategist Peter Chia at UOB Group, AUD/USD could extend the current advance to the area beyond the 0.6800 hurdle in the near term.

Key Quotes

24-hour view: “While we expected AUD to rise yesterday, we underestimated the pace of advance as it surged to a high of 0.6797 (we were of the view that AUD is unlikely to challenge the major resistance at 0.6760). Not surprisingly, upward momentum is strong and AUD could continue to advance. However, severely overbought conditions suggest that AUD might not be able to break clearly above 0.6820 today. Overall, only a breach of 0.6730 (minor support is at 0.6760) would indicate that AUD is not advancing further.”

Next 1-3 weeks: “Our most recent narrative was from Monday (10 Apr, spot at 0.6670) wherein we held the view that AUD ‘is likely to trade in a range of 0.6600/0.6760 for the time being’. Yesterday (13 Apr), AUD lifted off and surged above 0.6760 (high has been 0.6797). The rapid improvement in momentum suggests AUD is likely to advance further. Resistance is at 0.6820, followed by a rather strong level at 0.6860. The upside risk is intact as long as AUD stays above 0.6700 in the next few days.”

-

09:47

WTI struggles near $82 after IEA warns of risks to global economic recovery

In its latest oil market report published on Friday, the International Energy Agency (IEA) said that “OPEC+ supply cuts risk aggravating expected oil supply deficit in H2 2023,” which could lead to high prices that will hurt consumers and threaten economic growth.

Additional takeaways

OECD industry stocks in Jan surged by 53 mln barrels to 2.830 bln barrels, highest since July 2021.

Russian oil exports in March rose to highest since April 2020, with oil shipments rising by 600,000 bpd.

Russian oil product flows returned to levels last seen before Russia invaded Ukraine.

Rising global oil stocks may have contributed to OPEC+ decision.

Gains of 1 mln bpd from non-OPEC+ starting in March will fail to offset a 1.4 mln bpd decline from OPEC+.

Extra cuts by OPEC+ will push world oil supply down 400,000 bpd by end-2023.

Oecd demand contracted by 390,000 bpd YoY in Q1 due to weak industrial activity, warm weather.

Non-OECD countries led by China will make up 90% of demand growth.

Global oil demand is set to rise by 2 mln bpd in 2023 to a record 101.9 mln bpd.

Market reaction

WTI is struggling near the $82 mark after IEA’s oil market outlook. The US oil is losing 0.41% on the day.

-

09:35

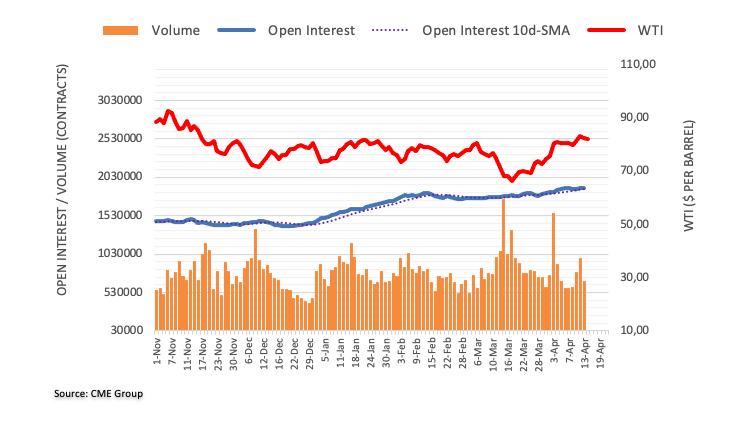

Crude Oil Futures: Outlook is expected to remain bullish

CME Group’s flash data for crude oil futures markets showed traders reduced their open interest positions by around 12.4K contracts on Thursday, while volume reversed three dailu pullbacks in a row and went up by around 294.3K contracts.

WTI appears supported by $80.00

Thursday’s knee-jerk in prices of the WTI came in tandem with declining open interest and volume, leaving scarce room for the continuation of the corrective decline in the very near term. In the meantime, the $80 region per barrel should hold the initial test for the time being.

-

09:34

Silver Price Analysis: XAG/USD eases from one-year peak, bullish bias remains intact

- Silver pulls back from a fresh one-year high touched earlier this Friday amid overbought RSI.

- The technical setup still favours bulls and supports prospects for a further appreciating move.

- Any meaningful corrective slide might still be seen as a buying opportunity and remain limited.

Silver touches a fresh one-year high on the last day of the week, albeit struggles to capitalize on the move and faces rejection near the $26.00 round-figure mark. The white metal surrenders its modest gains and trades near the lower end of its daily range, around the $25.85-$25.80 region during the early part of the European session.

Against the backdrop of a strong rally witnessed over the past month or so, the slightly overbought Relative Strength Index (RSI) on the daily chart turns out to be a key factor holding back traders from placing fresh bets around the XAG/USD. That said, the recent breakout through the $24.30-$24.40 strong horizontal barrier and a subsequent move beyond the $25.00 psychological mark support prospects for additional gains.

Hence, any subsequent pullback is more likely to attract fresh buyers near the $25.40-$25.35 area, or the overnight swing low. This should help limit the downside for the XAG/USD near the $25.00 mark. That said, a convincing break below the latter might prompt some technical selling and accelerate the corrective slide towards the $24.30-$24.40 resistance-turned-support. The latter should act as a strong near-term base for the metal.

On the flip side, bulls might now wait for some follow-through buying beyond the daily swing high, around the $26.00 mark, before placing fresh bets and positioning for a further appreciating move. The XAG/USD might then climb further towards the next relevant hurdle near the $26.40-$26.50 zone before eventually aiming to test the 2022 peak, just ahead of the $27.00 mark.

Silver daily chart

Key levels to watch

-

09:28

GBP/USD: A test of 1.2600 appears on the cards – UOB

The continuation of the upside momentum could motivate GBP/USD to challenge the 1.2600 neighbourhood in the next few weeks, suggest Markets Strategist Quek Ser Leang and Senior FX Strategist Peter Chia at UOB Group.

Key Quotes

24-hour view: “We highlighted yesterday that GBP ‘is likely to break 1.2525 but it might not be able to hold above this level’. We added, ‘The next significant resistance level at 1.2600 is not expected to come into view today’. As expected, GBP took out 1.2525 as it rose to a high of 1.2537. Despite the advance, upward momentum has not improved much. While GBP could continue to advance, 1.2600 is still unlikely to come into view today (there is a minor resistance level at 1.2560). Support is at 1.2500, a break of 1.2475 would indicate that the current upward pressure has eased.”

Next 1-3 weeks: “We highlighted yesterday (13 Apr, spot at 1.2490) that ‘the rapid improvement in momentum suggests GBP is ready to head higher’. We noted resistance levels are at 1.2525 and 1.2600. Our view for a higher GBP was not wrong as it rose above 1.2525 (high has been 1.2537). While momentum has not increased by all that much, GBP is likely to advance further to 1.2600, possibly 1.2665. On the downside, a break of 1.2440 (‘strong support’ level was at 1.2400 yesterday) would indicate that our view for GBP to continue to rise is wrong.”

-

09:22

EUR/USD remains firm and climbs to fresh highs near 1.1080

- EUR/USD advances further and prints new YTD peaks at 1.1075.

- The greenback remains offered and navigates fresh 2023 lows.

- US Retail Sales, Consumer Sentiment take centre stage in the NA session.

Further selling pressure in the greenback pushes EUR/USD to fresh 2023 highs in the vicinity of 1.1080 at the end of the week.

EUR/USD now looks at 1.1100 and above

EUR/USD advances for the fourth session in a row and consolidates further the recent breakout of the psychological 1.1000 hurdle on Friday in a context of persistent weakness hurting the dollar.

The pair’s weekly leg higher has been underpinned by investors’ firmer perception that the Fed might halt its hiking cycle in the near term and most likely following the May gathering, when it is still expected to hike the Fed Funds Target Range (FFTR) by another 25 b

Also propping up the solid momentum in the pair, many ECB rate setters have been advocating for the continuation of the tightening process in the region, putting back on the table a potential 50 bps rate raise next month.

Data wise in the region, final inflation figures in France showed the CPI rose 0.9% MoM in March and 5.7% from a year earlier.

It will be an interesting calendar across the pond, where Retail Sales are due along with Industrial Prodcution, the advanced Michigan Consumer Sentiment and Business Inventories. In addition, FOMC’s C. Waller (permanent voter, centrist) is due to speak.

What to look for around EUR

EUR/USD prints new peaks well north of 1.1000 the figure on the back of the pronounced decline in the greenback and expectations of further tightening by the ECB.

In the meantime, price action around the single currency should continue to closely follow dollar dynamics, as well as the incipient Fed-ECB divergence when it comes to the banks’ intentions regarding the potential next moves in interest rates.

Moving forward, hawkish ECB-speak continue to favour further rate hikes, although this view appears in contrast to some loss of momentum in economic fundamentals in the region.

Eminent issues on the back boiler: Continuation, or not, of the ECB hiking cycle. Impact of the Russia-Ukraine war on the growth prospects and inflation outlook in the region. Risks of inflation becoming entrenched.

EUR/USD levels to watch

So far, the pair is gaining 0.11% at 1.1058 and a break above 1.1075 (2023 high April 14) would target 1.1100 (round level) en route to 1.1184 (weekly high March 21 2022). On the flip side, the next support comes at 1.0788 (monthly low April 3) followed by 1.0754 (55-day SMA) and finally 1.0712 (low March 24).

-

09:07

EUR/USD faces the next target at 1.1120 – UOB

According to Markets Strategist Quek Ser Leang and Senior FX Strategist Peter Chia at UOB Group, further upside in EUR/USD should meet the next resistance level at 1.1120 in the near term.

Key Quotes

24-hour view: “While we expected EUR to strengthen yesterday, we were of the view that ‘a sustained break above 1.0335 is unlikely today’. The pace of the advance in EUR exceeded our expectations as it rose to 1.0975 before closing at a 1-year high of 1.1044 (+0.50%). There is scope for EUR to advance further even though the next significant resistance at 1.1120 is likely out of reach for today (there is a minor resistance at 1.1080). On the downside, a breach of 1.0995 (minor support is at 1.1020) would indicate that the advance in EUR is ready to take a breather.”