Noticias del mercado

-

23:59

Schedule for today, Wednesday, Aug 10’2016

(time / country / index / period / previous value / forecast)

00:30 Australia Westpac Consumer Confidence August -3%

01:30 Australia Home Loans June -1% 2.4%

03:05 Australia RBA's Governor Glenn Stevens Speech

06:45 France Industrial Production, m/m June -0.5% 0.2%

14:00 U.S. JOLTs Job Openings June 5.5 5.52

14:30 U.S. Crude Oil Inventories August 1.413

18:00 U.S. Federal budget July 6 -129.9

21:00 New Zealand RBNZ Interest Rate Decision 2.25% 2%

21:00 New Zealand RBNZ Rate Statement

21:05 New Zealand RBNZ Press Conference

-

21:00

DJIA 18521.51 -7.78 -0.04%, NASDAQ 5224.51 11.37 0.22%, S&P 500 2180.38 -0.51 -0.02%

-

18:00

European stocks closed: FTSE 6851.30 42.17 0.62%, DAX 10692.90 260.54 2.50%, CAC 4468.07 52.61 1.19%

-

17:54

Oil rose today

Today, during the American session oil rose while market participants expect the publication of fresh weekly report on US oil and petroleum products.

The American Petroleum Institute is scheduled to release its report on stocks today, while government data expected on Wednesday may show the decrease in inventories by 1.0 million barrels for the week ending 5 August.

Gasoline stocks are expected to decline by 1.2 million barrels, while, according to analysts, distillate stocks, including heating oil and diesel fuel, will increase by 375,000 barrels.

On Monday in New York crude oil futures jumped $ 1.22, or 2.92%, as renewed hopes for an agreement between the exporters supported the market by freezing production.

Despite the recent growth, the market experts believe that increased fuel product inventories amid slowing global demand growth, most likely, will put pressure on prices in the short term.

Futures for WTI crude oil lost nearly 17% this year after falling from highs above $ 50 per barrel reached in early June amid signs of recovery in the US drilling activity combined with higher fuel product inventory.

According to Baker Hughes, the number of drilling rigs in the US increased by 7 to 381 last week, increasing the sixth week in a row and the ninth week of the last ten.

Number of oil rigs in the United States increases the sixth consecutive week, increasing concern about the over-saturation of the oil market.

A day earlier, the price of Brent crude rose $ 1.12, or 2.53%, as sentiment rose amid renewed hopes for an agreement on exporting production freeze.

According to some sources, several OPEC members, including Venezuela, Ecuador and Kuwait, want to revive the idea of limits on oil production in an attempt to stabilize the market this fall.

Qatar's Energy Minister Mohammed bin Saleh Al Sada, who has served as president of OPEC this year, has confirmed that the cartel will hold an informal meeting of 26-28 September at the International Energy Forum in Algiers.

Nevertheless, market participants are still skeptical about this meeting. Earlier this year, an attempt to freeze level of production was not a success because of Iran's refusal to participate in the initiative.

Meanwhile, Venezuela's oil minister Eulogio del Pino said that the meeting of OPEC and countries outside the cartel could take place "in the coming weeks", but Alexander Novak, Minister of Energy of Russia sees no grounds for the resumption of freeze negotiations.

Brent lost almost 15% from the high in early June, $ 52.80, as the prospects for increasing exports from the Middle East and North African countries, such as Iran, Libya and Nigeria, have raised concern that an excess of oil will reduce demand from refiners.

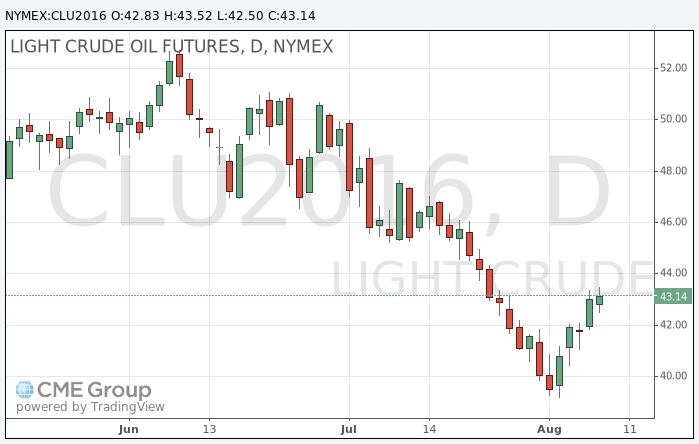

The cost of the September futures on WTI rose to 43.52 dollars per barrel.

September futures price for North Sea petroleum mix of mark Brent fell to 45.77 dollars a barrel on the London Stock Exchange ICE Futures Europe.

-

17:38

WSE: Session Results

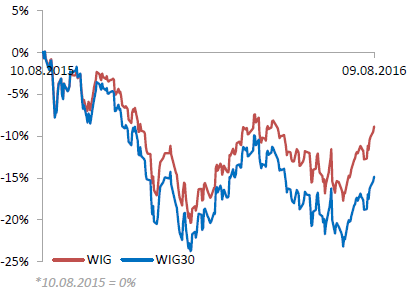

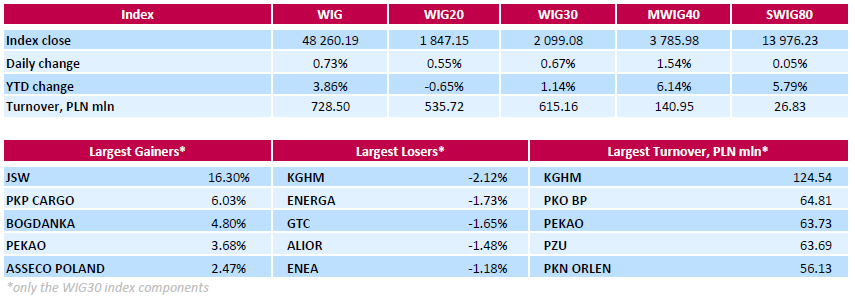

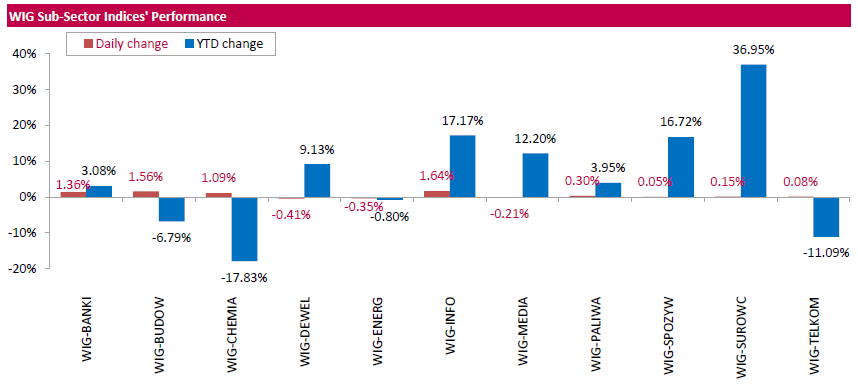

Polish equity market closed higher on Tuesday. The broad market measure, the WIG index, added 0.73%. Sector-wise, information technology stocks (+1.64%) fared the best, while developing sector names (-0.41%) fell the most.

The large-cap benchmark, the WIG30 Index, surged by 0.67%. Within the index components, coking coal miner JSW (WSE: JSW) led the gainers, skyrocketing by 16.3%, supported by the announcement the company agreed to transfer its Krupiński coal mine to the state-funded restructuring company by the end of January 2017. The transfer is within the frames of JSW's ongoing corporate restructuring and is expected to allow the company to reduce capex and labor costs. Other major advancers were railway freight transport operator PKP CARGO (WSE: PKP), thermal coal miner BOGDANKA (WSE: LWB) and bank PEKAO (WSE: PEO), climbing 6.03%, 4.8% and 3.68% respectively. On the other side of the ledger, copper producer KGHM (WSE: KGH), genco ENERGA (WSE: ENG) and property developer GTC (WSE: GTC) topped the list of the underperformers, dropping by 2.12%, 1.73% and 1.65% respectively.

-

17:29

Gold price increased moderately

Gold moved from decline to growth, but fears that the US Federal Reserve may raise interest rates this year undermining the interest in the metal.

According to the data by CME Group Fed Watch, traders' views on the possible lUS interest rates hike in December is now divided exactly evenly.

"Gold is generally settled at a higher range between $ 1.335 and $ 1.365, - said the chief commodities analyst at Saxo Bank Ole Hansen -. I think we are waiting for clues, especially the dollar, as investors are not ready to force without the support of a weaker dollar. "

The dollar was little changed against the currency basket on Tuesday. Stock markets rose due to investors' appetite for risk.

Senior Fed official Jerome Powell said on Monday that the increased risk of a long phase of slow growth of the US economy points to the need for lower interest rates than previously expected.

Stocks of the world's largest gold exchange-traded fund SPDR Gold Shares on Monday fell by 6.5 tons, it is the strongest one-day outflow in the past month.

The cost of the October futures on COMEX gold rose to $ 1,343.90 an ounce.

-

17:18

Wall Street. Major U.S. stock-indexes slightly rose

Major U.S. stock-indexes traded near record highs on Tuesday morning as a rise in technology stocks added to the lift from steadying oil prices. Oil edged further above $45 on estimates of a drop in U.S. inventories and speculation of producer action to freeze output.

Most of Dow stocks in positive area (19 of 30). Top gainer - The Goldman Sachs Group, Inc. (GS, +0.82%). Top loser - American Express Company (AXP, -0.29%).

All S&P sectors, but for Industrial Goods (-0.11%), in positive area. Top gainer - Conglomerates(+0.73%).

At the moment:

Dow 18512.00 +52.00 +0.28%

S&P 500 2182.00 +6.50 +0.30%

Nasdaq 100 4803.00 +23.75 +0.50%

Oil 43.04 +0.02 +0.05%

Gold 1347.40 +6.10 +0.45%

U.S. 10yr 1.56 -0.02

-

16:48

US inventories unexpectedly showing an increase

Reflecting a jump in inventories of non-durable goods, the Commerce Department released a report on Tuesday unexpectedly showing an increase in U.S. inventories of wholesale goods in the month of June.

The report said wholesale inventories rose by 0.3 percent in June following an upwardly revised 0.2 percent increase in May.

Economists had expected inventories to come in unchanged compared to the 0.1 percent uptick that had been reported for the previous month.

The unexpected increase in wholesale inventories came as inventories of non-durable goods surged up by 1.1 percent in June after inching up by 0.1 percent in May.

Inventories of drugs and druggists' sundries and farm product raw materials showed significant increases during the month.

On the other hand, the report said inventories of durable goods fell by 0.3 percent in June after rising by 0.2 percent in May.

A drop in inventories of electrical and electronic goods offset an increase in inventories of lumber and other construction materials - RTT news.

-

16:46

US: the index of economic optimism from IBD / TIPP rose sharply in August

The data showed that the index of economic optimism in the US, calculated by the newspaper Investor's Business Daily and research firm TechnoMetrica, rose in August by 2.9 points, or 6.4%, reaching 48.4 points. Economists had expected the index to rise to 46.2 points. It is worth emphasizing the last value is 1.6 points higher than the 12-month average (46.8 points), but still 0.6 points lower than the all time average (49.0 points). Tndex value above 50 indicates optimism, while below 50, pessimism.

Economic Optimism Index is comprised of three main components. This month, two components have improved: the sub-six-month economic outlook index rose 8.0 points, or 21.8%, to 44.7 points, while the sub-index of the personal financial outlook for the next six months rose to 0.8 points , or 1.4%, to 58.0 points. Meanwhile, the sub-index of confidence in federal economic policies fell by 0.2 points, or 0.5%, to 42.7 points.

"The economic confidence of americans rose again in August after a strong deterioration in the last month caused by concerns about the global economy after Brexit. Despite the fact that the economic recovery continues its seventh year run, the trust will continue to be shaky at best, which is reflected in the continued level of pessimism in our index. 48 percent of respondents believe that the economic situation does not improve, while 49 percent believe that improves. in addition, 59 percent of respondents said that the economy is not in recession, and 37 percent reported the opposite, "- said Raghavan Maur, president of TechnoMetrica.

-

16:40

-

16:01

United Kingdom: NIESR GDP Estimate, July 0.3%

-

16:00

U.S.: Wholesale Inventories, June 0.3% (forecast 0.1%)

-

15:50

WSE: After start on Wall Street

The beginning of trading on Wall Street is slightly upward, although the last days we may see a weaker performance of Wall Street compare to shining triumphs of emerging markets or even the German DAX. After a quiet yesterday's session, today's trade promises to have a similar style, which fits in neutral opening and cosmetic increases of contracts. For the bulls it is important that goof mood is still maintained.

On the Warsaw market afternoon trading phase is quite successful, which, like yesterday, may be associated with the activity of foreign funds managed from the United States.

-

15:45

Option expiries for today's 10:00 ET NY cut

EURUSD 1.0800 (EUR 261m) 1.1099-1.1100 (435m)

USDJPY 102.00 (USD 825m) 104.00 (570m) 104.50 (348m)

GBPUSD 1.2800 (GBP 203m) 1.2900-05 (270m) 1.2950 (275m) 1.2960-65 (248m)

USDCHF 0.9615 (USD 240m) 1.0000 (600m)

AUDUSD 0.7600 (AUD 225m) 0.7625 (260m)

USDCAD 1.3100-05 (USD 470m) 1.3200 (1.1bln)

EURJPY 111.35 (EUR 370m)

AUDJPY 78.83 (AUD 241m)

-

15:40

US labour productivity is underrated and this is why

Labour productivity in the United States continued to decline in the spring of this year, to record a third consecutive quarterly decline, which could jeopardize the growth rate of wages in the whole economy in the coming years. This was stated by the Ministry of Labour.

The data showed that the level of labor productivity in the agricultural sector - the gauge of production of goods and services for one hour of work - decreased in the 2nd quarter by 0.5% compared to the 1st quarter (seasonally adjusted). The reason for this change has been a more rapid growth in the hours worked than in output. Recall that in the first quarter productivity fell by 0.6%.

In annual terms, the labor productivity decreased by 0.4%, recording the first annual decline in three years.

Unit labor costs among the non-agricultural enterprises in the second quarter rose by 2.0% after falling 0.2% in the first quarter (revised from + 4.5%). Compared to 2015, unit labor costs rose by 2.1% Economists had expected productivity to rise by 0.5%, while labor costs to increase by 1.8%.

The rate of growth of labor productivity is a key factor in determining how quickly wages and the economy can grow as a whole. Strong productivity gains, as noted in the late 1990s and early 2000s, can lead to sustainable economic growth and wage inflation. But sluggish growth performance may restrain wage growth and economic expansion. According to the data, average annual productivity growth from 2007 to 2015 was 1.3%, which is less than half the pace recorded from 2000 to 2007.

-

15:31

U.S. Stocks open: Dow +0.06%, Nasdaq +0.04%, S&P +0.03%

-

15:19

Before the bell: S&P futures +0.08%, NASDAQ futures +0.14%

U.S. stock-index futures were little changed as investors assessed recent gains.

Global Stocks:

Nikkei 16,764.97 +114.40 +0.69%

Hang Seng 22,465.61 -29.15 -0.13%

Shanghai 3,025.91 +21.63 +0.72%

FTSE 6,833.69 +24.56 +0.36%

CAC 4,439.17 +23.71 +0.54%

DAX 10,526.11 +93.75 +0.90%

Crude $42.95 (-0.16%)

Gold $1,338.50 (-0.21%)

-

14:54

Wall Street. Stocks before the bell

(company / ticker / price / change ($/%) / volume)

ALCOA INC.

AA

10.45

-0.00(-0.00%)

2130

ALTRIA GROUP INC.

MO

66.6

0.11(0.1654%)

416

Amazon.com Inc., NASDAQ

AMZN

767

0.44(0.0574%)

16267

Apple Inc.

AAPL

108.11

-0.26(-0.2399%)

143998

Barrick Gold Corporation, NYSE

ABX

21.51

0.09(0.4202%)

79576

Boeing Co

BA

133

0.81(0.6128%)

772

Chevron Corp

CVX

101.5

0.30(0.2964%)

6085

Cisco Systems Inc

CSCO

31.1

0.09(0.2902%)

1421

Citigroup Inc., NYSE

C

45.99

0.03(0.0653%)

3153

Exxon Mobil Corp

XOM

88.69

0.10(0.1129%)

5146

Facebook, Inc.

FB

125.39

0.13(0.1038%)

30198

Ford Motor Co.

F

12.22

0.04(0.3284%)

44514

Freeport-McMoRan Copper & Gold Inc., NYSE

FCX

12.2

-0.09(-0.7323%)

47730

General Electric Co

GE

31.25

-0.02(-0.064%)

4300

General Motors Company, NYSE

GM

31.06

0.18(0.5829%)

2800

Google Inc.

GOOG

781.02

-0.74(-0.0947%)

259

Intel Corp

INTC

35.04

0.00(0.00%)

4934

International Business Machines Co...

IBM

162.14

0.10(0.0617%)

549

Merck & Co Inc

MRK

62.61

-0.25(-0.3977%)

4650

Microsoft Corp

MSFT

58.12

0.06(0.1033%)

484

Nike

NKE

56

0.02(0.0357%)

880

Pfizer Inc

PFE

34.95

0.02(0.0573%)

1878

Tesla Motors, Inc., NASDAQ

TSLA

226.69

0.53(0.2343%)

7426

Twitter, Inc., NYSE

TWTR

18.19

-0.01(-0.0549%)

17113

Verizon Communications Inc

VZ

53.7

0.11(0.2053%)

460

Wal-Mart Stores Inc

WMT

73.45

0.11(0.15%)

1118

Walt Disney Co

DIS

96.03

0.28(0.2924%)

2344

Yahoo! Inc., NASDAQ

YHOO

39.47

0.23(0.5861%)

178081

-

14:43

Upgrades and downgrades before the market open

Upgrades:

Chevron (CVX) upgraded to Overweight from Neutral at Piper Jaffray; target raised to $117

Downgrades:

Other:

Volkswagen AG (VOW3) initiated with an Underperform at Jefferies

General Motors (GM) initiated with a Hold at Jefferies; target $33

General Motors (GM) initiated with Buy ratings at Seaport Global Securities

Ford Motor (F) initiated with a Underperform at Jefferies; target $10

Barrick Gold (ABX) initiated with an Equal Weight at Morgan Stanley

-

14:30

U.S.: Nonfarm Productivity, q/q, Quarter II -0.5% (forecast 0.5%)

-

14:30

U.S.: Unit Labor Costs, q/q, Quarter II 2% (forecast 1.8%)

-

14:21

Canda: July’s housing starts continued to pick up pace

The trend measure of housing starts in Canada was 201,936 units in July compared to 197,847 in June, according to Canada Mortgage and Housing Corporation (CMHC). The trend is a six-month moving average of the monthly seasonally adjusted annual rates of housing starts.

"July's housing starts continued to pick up pace, as construction strengthened in BC and Ontario's multi-unit segments," said Aled ab Iorwerth, CMHC's Deputy Chief Economist. "This reflects continued strong demand for lower-priced homes and low inventories of completed and unsold new units."

-

14:19

European session review: the US dollar strengthened against the pound

The following data was published:

(Time / country / index / period / previous value / forecast)

5:45 Switzerland's unemployment rate (not seasonally adjusted) July 3.1% 3.1% 3.1%

6:00 Germany Current Account 18.4 26.3 bln in June

6:00 Germany Trade balance (not seasonally adjusted), 24.9 billion on June 21

6:00 Japan Change in orders for equipment (preliminary data), y / y in July -19.9% -19.6%

8:30 UK Industrial Production m / m in June -0.6% 0.1% 0.1%

8:30 UK Industrial Production y / y in June 1.4% 1.6% 1.6%

8:30 UK Manufacturing production m / m in June -0.6% -0.2% -0.3%

8:30 UK Manufacturing production, y / y in June 1.5% 1.3% 0.9%

8:30 UK total trade balance in June -4.2 -5.1

The pound depreciated significantly against the dollar, updating the monthly lows. Certain influence on the dynamics of trade had statistics on Britain. The Office for National Statistics said that industrial output rose by 0.1 percent compared to May, confirming the forecasts of economists. At the end of May the production declined by 0.6 percent (revised from -0.5 percent). Output in the manufacturing sector decreased by 0.3 percent, which was slower than the fall of 0.6 percent in May. Experts predicted a decrease of 0.2 percent. Annual industrial production growth accelerated to 1.6 percent, in line with expectations, compared with 1.4 per cent. Manufacturing output increased by 0.9% y/y, after rising 1.5 percent in May. Analysts had expected an increase of 1.3 percent. For the three-month period to June, the volume of industrial production increased by 2.1 percent. This was the highest growth since the third quarter of 1999.

A separate report showed that the deficit in trade in goods widened in June to 12,4 billion in May (revised from 9,880 billion). Last change reflects an increase in exports by 1.0 billion pounds to 24.6 billion., as well as increased imports of 1.8 billion pounds to 37.0 billion. The surplus on trade in services remained unchanged at 7.3 billion pounds. As a result, the overall trade deficit amounted to 5.1 billion.

In focus were also statements by the Bank of England and member of the Monetary Policy Committee Ian McCafferty, who pointed to the possibility of expanding monetary stimulus measures if the state of the British economy deteriorates. Recall, last week the Bank of England lowered the benchmark interest rate to a record low level and increased the volume of bond purchases to soften the negative impact of Brexit. In general, the last stimulus program indicates a strong concern for the Bank of England officials about the economic outlook.

The euro is trading flat vs usd. Recall, the Federal Statistical Office of Germany stated that exports rose in June by 0.3% compared to May, while imports by 1.0%. The trade surplus amounted to 21.7 billion euros against 22.1 billion euros in May. At the end of the 2nd quarter exports grew by 0.7%, while imports decreased by 1.6%.

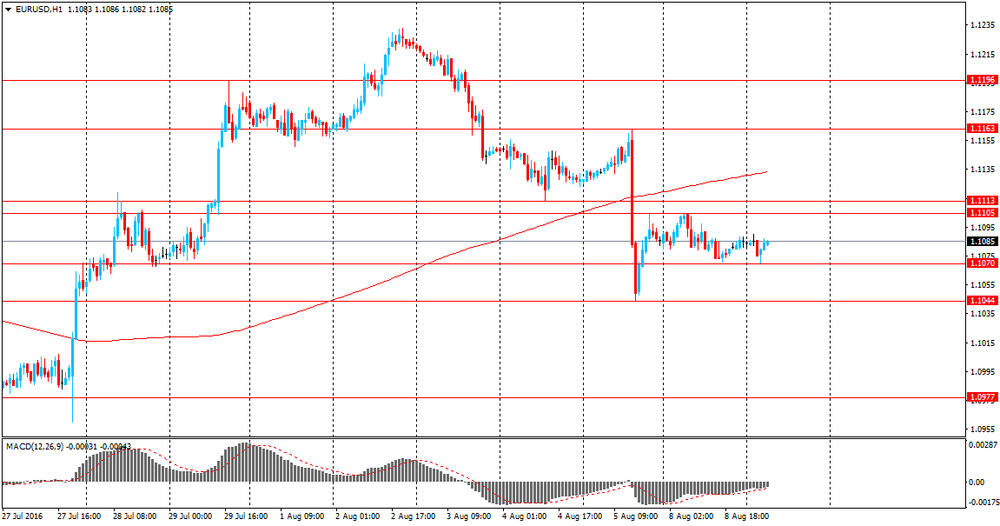

EUR / USD: during the European session, the pair rose to $ 1.1097, but then fell back to $ 1.1075

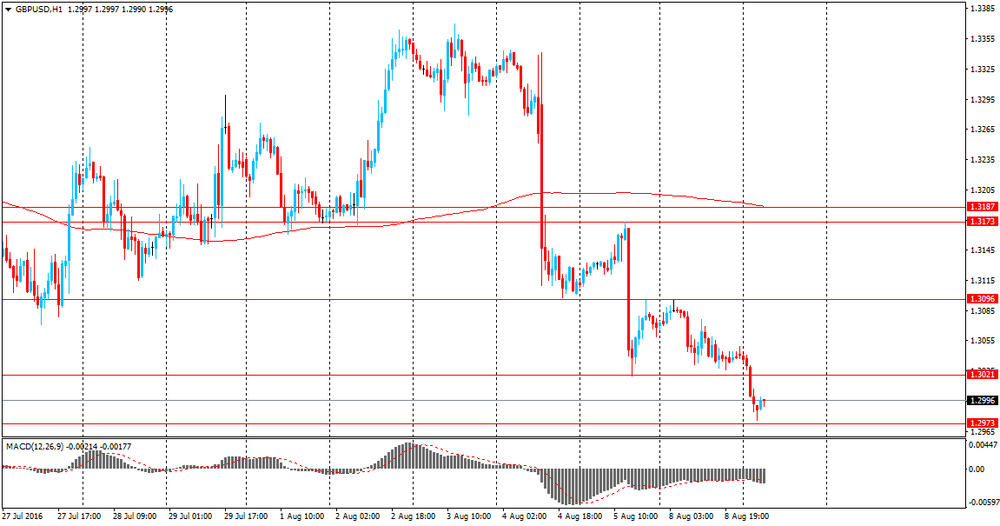

GBP / USD: during the European session, the pair fell to $ 1.2960

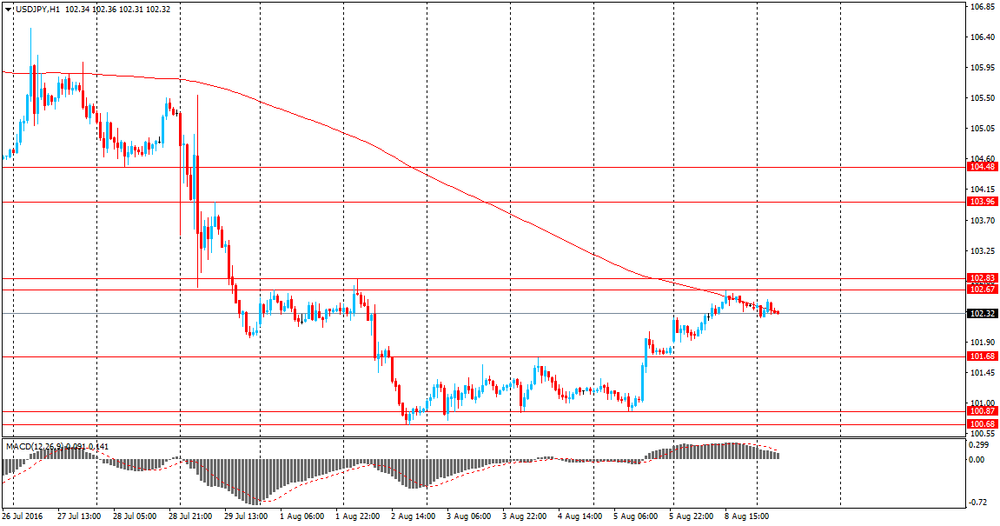

USD / JPY: during the European session, the pair fell to Y102.14

-

14:14

Canada: Housing Starts, July 198.4 (forecast 195)

-

13:45

Orders

EUR/USD

Offers 1.1085 1.1100 1.1120 1.1155-60 1.1180 1.1200

Bids 1.1070 1.1050-55 1.1020-25 1.1000-05 1.0980 1.0950-60

GBP/USD

Offers 1.3000 1.3020 1.3045-50 1.3080 1.3100-05 1.3130 1.3150

Bids 1.2950 1.2930 1.2900-05 1.2880 1.2865 1.2850

EUR/GBP

Offers 0.8550 0.8580 0.8600 0.8630 0.8650

Bids 0.8520 0.8500 0.8475-80 0.8450 0.8430 0.8400 0.8350

EUR/JPY

Offers 113.85 114.00 114.50 114.80 115.00

Bids 113.20 113.00 112.85 112.50 112.00-10 111.50 111.00

USD/JPY

Offers 102.60 102.80-85 103.00 103.30 103.50-60 103.85 104.00

Bids 102.25-30 102.00 101.65-70 101.50 101.20 101.00 100.70-75100.50

AUD/USD

Offers 0.7670 0.7685 0.7700 0.7720 0.7750

Bids 0.7620 0.7600 0.7585 0.7565 0.7570 0.7550 0.7520 0.7500

-

13:42

US: The Index of Small Business Optimism increased slightly

The Index of Small Business Optimism increased 0.1 points to 94.6, still well below the 40 year average of 98. Four of the 10 Index components posted a gain, four declined and two were unchanged. GDP growth in the last three quarters has averaged 1 percent, not a recession but only matching the growth in the population. The outlook for business conditions six months from the current period continued to improve, gaining 16 percentage points since January but still in negative territory - more owners expecting deterioration than improvement.

-

13:07

WSE: Mid session comment

Today's session, as yesterday, runs very quietly and is devoid of significant new impulses to trade. In Europe, a slightly falling prices of commodity companies, other industries are on small pros. Further good behave banking sector. The German market is located at the previous highs, and in close proximity to a maximum of April. Exceeding these resistances will be a medium-term buy signal, which should improve the climate for a long time in Europe, which recently lost a little in the eyes of global investors.

On the Warsaw market rather unexpected drop in the morning in the southern phase of trade has been neutralized and the WIG20 index has returned to the levels of today's opening. Activity remains small, and quotes differ a little from the area of yesterday's many hours of consolidation. At the halfway point of the session the WIG20 index was at 1,836 points (-0,04%) and with turnover of approx. PLN 235 million.

-

12:42

Major stock indices in Europe show moderate gains

European stocks traded with a moderate increase, helped by positive corporate reporting of a number of companies and recovery of oil prices.

Certain influence on the dynamics of trade had statistics on Britain. The Office for National Statistics said that industrial output rose by 0.1 percent compared to May, confirming the forecasts of economists. At the end of May the production declined by 0.6 percent (revised from -0.5 percent). Output in the manufacturing sector decreased by 0.3 percent, which was slower than the fall of 0.6 percent in May. Experts predicted a decrease of 0.2 percent. Annual industrial production growth accelerated to 1.6 percent, in line with expectations, compared with 1.4 per cent. Manufacturing output increased by 0.9% y/y, after rising 1.5 percent in May. Analysts had expected an increase of 1.3 percent. For the three-month period to June, the volume of industrial production increased by 2.1 percent. This was the highest growth since the third quarter of 1999.

A separate report showed that the deficit in trade in goods widened in June to 12,4 billion in May (revised from 9,880 billion). Last change reflects an increase in exports by 1.0 billion pounds to 24.6 billion., as well as increased imports of 1.8 billion pounds to 37.0 billion. The surplus on trade in services remained unchanged at 7.3 billion pounds. As a result, the overall trade deficit amounted to 5.1 billion.

In focus were also statements by the Bank of England and member of the Monetary Policy Committee Ian McCafferty, who pointed to the possibility of expanding monetary stimulus measures if the state of the British economy deteriorates. Recall, last week the Bank of England lowered the benchmark interest rate to a record low level and increased the volume of bond purchases to soften the negative impact of Brexit. In general, the last stimulus program indicates a strong concern for the Bank of England officials about the economic outlook.

The composite index of Europe's largest companies Stoxx 600 added 0.2 percent. Over the last four sessions the index rose by 1.8 percent. The trading volume today is 39 percent lower than the monthly average.

Altice cost rose 12 percent amid reports of increasing profits. The company said that the increase was due to the good performance in Portugal and the USA.

Voestalpine AG Shares fell 3.2 percent, putting pressure on the shares of mining companies. Today, the company reported a 64 percent decline in profits.

Quotes of Amec Foster Wheeler Plc surged 13 percent as revenue and profit of the company exceeded the forecasts of experts.

Share of SFR Group SA rose 12 percent after Altice said it plans to cut 5,000 jobs in the French company.

Cost of Legal & General Group Plc fell 6.5 percent, as the profit margin was lower than analysts' estimates.

At the moment:

FTSE 100 +22.27 6831.40 + 0.33%

DAX +51.54 10483.90 + 0.49%

CAC 40 +21.14 4436.60 + 0.48%

-

11:46

USD/CAD: Risks 'Largely' To The Upside From Current Levels - Credit Agricole

"The CAD has remained on the sidelines of the recent USD sell-off. While CAD's daily correlation with oil has weakened, crude's further decline has prevented the CAD from strengthening over the past two weeks. Further downside may be limited from here but conditions for a rebound are also lacking in our view, which implies that oil will not be offering much support to the Canadian economy and currency soon.

Meanwhile, the BoC will likely remain in a wait-and-see mode at least until it sees Q3 data. We think policymakers may be excessively optimistic on the impact of fiscal spending while a combination of a neutral policy stance and falling inflation expectations may trigger an unwanted tightening in real rates in Canada. Furthermore an over-leveraged consumer and further signs of housing market excesses in BC are paradoxically helping CAD by restraining the BoC in the short-term but they are a looming risk to the economy and currency over the medium-term.

We continue to see risks as largely favouring USD/CAD upside from current levels" - efxnews.

-

10:44

UK's trade balance deficit increased sharply

The UK's deficit on trade in goods and services was estimated to have been £5.1 billion in June 2016, a widening of £0.9 billion from May 2016. Exports increased by £1.0 billion and imports increased by £1.9 billion. Imports reached a record high of £48.9 billion.

The deficit on trade in goods was £12.4 billion in June 2016, widening by £0.9 billion from May 2016. This widening reflected an increase in exports of £1.0 billion to £24.6 billion and an increase in imports of £1.8 billion to £37.0 billion.

Between Quarter 1 (January to March) 2016 and Quarter 2 (April to June) 2016, the total trade deficit for goods and services widened by £0.4 billion to £12.5 billion.

Between Quarter 1 2016 and Quarter 2 2016 the deficit on trade in goods widened by £0.1 billion to a deficit of £34.4 billion. Exports increased by £4.1 billion (5.8%) and imports increased by £4.1 billion (4.0%).

-

10:42

UK manufacturing production down 0.3% in June

Total production output is estimated to have increased by 2.1% between Quarter 1 (Jan to Mar) 2016 and Quarter 2 (Apr to Jun) 2016.

The largest contribution to the quarterly increase in total production came from manufacturing, which increased by 1.8%. The largest contribution to the increase in manufacturing came from the manufacture of transport equipment, which increased by 5.6%.

Total production output is estimated to have increased by 1.6% in June 2016 compared with June 2015. There were increases in all of the main sectors, with the largest contribution coming from manufacturing (the largest component of production), which increased by 0.9%.

Total production output is estimated to have increased by 0.1% in June 2016 compared with May 2016. There were increases in 3 of the 4 main sectors, with the only downward contribution coming from manufacturing, which decreased by 0.3%. There were decreases in 9 of the 13 manufacturing subsectors, with the largest contribution coming from the manufacture of transport equipment, which decreased by 1.0%.

-

10:31

United Kingdom: Total Trade Balance, June -5.1

-

10:30

United Kingdom: Industrial Production (MoM), June 0.1% (forecast 0.1%)

-

10:30

United Kingdom: Manufacturing Production (YoY), June 0.9% (forecast 1.3%)

-

10:30

United Kingdom: Industrial Production (YoY), June 1.6% (forecast 1.6%)

-

10:30

United Kingdom: Manufacturing Production (MoM) , June -0.3% (forecast -0.2%)

-

10:21

Option expiries for today's 10:00 ET NY cut

EUR/USD 1.0800 (EUR 261m) 1.1099-1.1100 (435m)

USD/JPY 102.00 (USD 825m) 104.00 (570m) 104.50 (348m)

GBP/USD 1.2800 (GBP 203m) 1.2900-05 (270m) 1.2950 (275m) 1.2960-65 (248m)

USD/CHF 0.9615 (USD 240m) 1.0000 (600m)

AUD/USD 0.7600 (AUD 225m) 0.7625 (260m)

USD/CAD 1.3100-05 (USD 470m) 1.3200 (1.1bln)

EUR/JPY 111.35 (EUR 370m)

AUD/JPY 78.83 (AUD 241m)

-

09:52

Oil trading lower

This morning, New York crude oil futures for WTI fell by -0.93% to $ 42.62 and Brent oil futures were down -0.99% to $ 44.92 per barrel. Thus, the black gold is trading lower on the background of concerns about the glut of world markets, as well as investors booked profits after the nearly 3 percent gain in the previous session. Venezuela's oil minister said that in the near future OPEC and non-OPEC countries will meet, looking for support to revive the oil markets. OPEC officials said that a freeze of production can be on the table at the planned meeting in September. Russia said that sees no reason to freeze production at current levels

-

09:28

Today’s events:

At 15:30 GMT the United States will hold an auction of 4-week bills.

At 17:00 GMT the United States will hold an auction of 3-year bonds.

At 20:30 GMT the report of the American Petroleum Institute (API) on oil stocks.

Also today, UK will hold an auction of 30-year government bonds.

-

09:27

Positive start for major stock exchanges: FTSE 100 6,811.22 + 17.75 + 0.26%, DAX 10,438.97 + 6.61 + 0.06%

-

09:15

WSE: After opening

WIG20 index opened at 1836.65 points (-0.02%)*

WIG 47919.88 0.02%

WIG30 2085.05 0.00%

mWIG40 3729.62 0.03%

*/- change to previous close

The cash market opened up with a modest fall of 0.02% to 1,836 points, what is the answer to the lack of major changes in global markets after the end of yesterday's session on the Warsaw Stock Exchange.

Prices of PKO BP (WSE: PKO) shares go down and the negative reaction we see in the case of values of Getin Noble Bank (WSE: GNB) which incidentally collect the second turnover on the market. The German DAX remains stable, and the local market is doing quite well with a worse behavior of KGHM and PKO BP.

-

08:52

Asian session review: the pound fall in anticipation of manufacturing data

During today's Asian session, the US dollar traded in a narrow range against the euro and the yen, while maintaining stability.

The pound was lower against the US dollar, despite the positive data on retail sales from the UK. According to British Retail Consortium retail sales increased by 1.1% year on year. Analysts had expected a decline to -0.7%. The previous value was also negative and amounted to -0.5%.

A report on retail sales, published by the British Retail Consortium, estimates changes in the actual retail sales companies, members of the consortium on the basis of regularly provided reliable information. This indicator shows the trend in the retail sector.

The BRC report states that recorded growth in retail sales is contrary to the UK talk about slowing consumer spending after Brexit. The growth of retail sales in July was the strongest since January of this year.

Also, the course of trading was influence by pricing in of today's statistics on industrial production in the UK. It is projected that by the end of June, industrial production increased by 0.2% in monthly terms and by 1.6% y/y. Meanwhile, production in the manufacturing sector is likely to contract by 0.2% in the month and increased by 1.3% per annum.

The Australian dollar has weakened since the beginning of the session, as the published results of the latest survey conducted by NAB showed that the index of business conditions in Australia fell in July to 8 with the previous value of 11, and the index of confidence in the business community dropped to 4 from 5 June.

Business conditions and confidence in business circles in Australia worsened amid growing uncertainty over the long-term prospects for the Australian economy.

NAB chief economist Alan Oster said the long-term risks are increasing, and it is likely to force the Reserve Bank of Australia to lower interest rates twice this year. Oster also said that short-term trends in the economy are satisfactory.

The Consumer Price Index of China, published by the National Bureau of Statistics of China, increased by 0.2% in July after falling 0.1% the previous month. This had an influence on commodity currencies. Analysts had expected an increase of 0.1%. In annual terms, the inflation indicator rose 1.8%. The pace of consumer price growth slowed slightly compared with +1.9% in June. The main factor that put pressure on the annual inflation was slowing food prices.

The result is a detailed summary of the data of urban and rural indices of consumer prices. The purchasing power of the Chinese currency is reduced under the influence of inflation. CPI - a key indicator of inflation and changes in purchasing trends. A decline in the consumer price index is a sign that inflation is becoming a destabilizing factor in the economy and could potentially provoke the People's Bank of China to tighten monetary policy and fiscal policy. In general, a high value is positive for China's currency.

Inflation remains well below the maximum target of 3% this year, giving the central bank room for easing monetary policy against the backdrop of the economic downturn.

Yu Qiumei, Senior Statistician at National Bureau of Statistics of China noted that a great influence on prices in the last month had heavy rains and flooding of the Yangtze basin. "Powerful rains significantly affected the processes of production and transport of fresh vegetables, which led to a rather strong increase in their prices in a number of regions".

Also, the National Bureau of Statistics of China released data on producer price index, which in July fell by 1.7% after falling 2.6% in June. Analysts had expected a decline to -2.0%

EUR / USD: during the Asian session, the pair was trading in the $ 1.1070-75 range.

GBP / USD: during the Asian session, the pair was trading in $ 1.2965-90 range.

USD / JPY: during the Asian session, the pair was trading in Y102.25-102.45 range.

-

08:39

The Fed Likely To Stay Behind The Curve; Staying USD Bearish - Morgan Stanley

"As long as US inflation expectations remain low, the Fed is unlikely to raise rates early.

In this respect, the 5Y/5Y inflation swap rising by 4bp on Friday was muted compared to the 10bp rise in the nominal US 5-year yield, driving real US yields higher. This is a short-term USD positive, but this support is unlikely to last long as the Fed may have no intention of allowing real rates to rise pre-emptively. An economy running high debt levels and relatively low returns on investment fares best when bond yields follow inflation expectations.

Hence, the Fed is likely to stay behind the curve, suggesting US real yields coming down again. However, it is not only the Fed which makes us USD-bearish".

-

08:33

Business confidence in Australia ebbed in July

Business confidence in Australia ebbed in July, the latest survey from National Australia Bank revealed on Tuesday with an index score of +4.

That's down from the downwardly revised +5 in June (originally +6).

The index for business conditions also took a hit, slipping to +8 from the downwardly revised +11 in the previous month (originally +12).

For the first half of the year, business confidence is roughly unchanged - RTT.

-

08:32

BoE's McCafferty: BoE should have a gradual approach as it’s hard to determine correct amount of stimulus - Times

-

08:29

Retail sales in UK remain strong in July

According to British Retail Consortium retail sales increased by 1.1% year on year. Analysts had expected a decline to -0.7%. The previous value was also negative and amounted to -0.5%.

A report on retail sales, published by the British Retail Consortium, estimates changes in the actual retail sales companies, members of the consortium on the basis of regularly provided reliable information. This indicator shows the trend in the retail sector.

The BRC report states that recorded growth in retail sales is contrary to the UK talk about slowing consumer spending after Brexit. The growth of retail sales in July was the strongest since January of this year.

-

08:28

Options levels on tuesday, August 9, 2016:

EUR/USD

Resistance levels (open interest**, contracts)

$1.1253 (4070)

$1.1196 (1738)

$1.1156 (802)

Price at time of writing this review: $1.1076

Support levels (open interest**, contracts):

$1.1029 (3089)

$1.0977 (4454)

$1.0944 (4390)

Comments:

- Overall open interest on the CALL options with the expiration date September, 9 is 45139 contracts, with the maximum number of contracts with strike price $1,1250 (4827);

- Overall open interest on the PUT options with the expiration date September, 9 is 52772 contracts, with the maximum number of contracts with strike price $1,1050 (4454);

- The ratio of PUT/CALL was 1.17 versus 1.15 from the previous trading day according to data from August, 8

GBP/USD

Resistance levels (open interest**, contracts)

$1.3305 (2316)

$1.3207 (1846)

$1.3111 (941)

Price at time of writing this review: $1.2989

Support levels (open interest**, contracts):

$1.2892 (1712)

$1.2795 (1978)

$1.2697 (932)

Comments:

- Overall open interest on the CALL options with the expiration date September, 9 is 28737 contracts, with the maximum number of contracts with strike price $1,3300 (2316);

- Overall open interest on the PUT options with the expiration date September, 9 is 23245 contracts, with the maximum number of contracts with strike price $1,2800 (1978);

- The ratio of PUT/CALL was 0.81 versus 0.80 from the previous trading day according to data from August, 8

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

08:26

Mixed start of trading expected on the major stock exchanges in Europe: DAX-0.2%, CAC40 -0.1%, FTSE + 0.1%

-

08:26

WSE: Before opening

Yesterday's session on Wall Street ended with little drop, which was accompanied by one of the lowest this year turnover. In Asia, the inflation data from China was in line with expectations, which, like yesterday's information about the trade, went unnoticed.

The Asian stock markets quotations are calm, both the Nikkei index and the Shanghai market are in little gain. Contracts in the US are flat and show that since yesterday afternoon nothing special in the world had happened.

During today's session, the Central Statistic Office will give data regarding the average salary level in the second quarter in Poland. In addition, the markets attention should focus on indications from the UK (industrial production) and the US (data regarding the labor market), but it is hard to talk about the key macro readings.

The relevant information may be the fact that the PFSA wants to considered Getin Noble Bank (WSE: GNB) as an institution of systemic importance and impose additional buffer. It will be smaller than in the case of PKO BP (proposed 0.25% of the total exposure to the risks) but we know what's going on - on foreign currency loans and have to reckon with further messages regarding the banks involved in these products, what today may slightly reduce appetite for those shares.

-

08:25

China's consumer price index above expectations in July

The Consumer Price Index, published by the National Bureau of Statistics of China, increased by 0.2% in July after falling 0.1% the previous month. Analysts had expected an increase of 0.1%. In annual terms, the inflation indicator rose 1.8%. The pace of consumer price growth slowed slightly compared with +1.9% in June. The main factor that put pressure on the annual inflation was slowing food prices.

The result is a detailed summary of the data of urban and rural indices of consumer prices. The purchasing power of the Chinese currency is reduced under the influence of inflation. CPI - a key indicator of inflation and changes in purchasing trends. A decline in the consumer price index is a sign that inflation is becoming a destabilizing factor in the economy and could potentially provoke the People's Bank of China to tighten monetary policy and fiscal policy. In general, a high value is positive for China's currency.

Inflation remains well below the maximum target of 3% this year, giving the central bank room for easing monetary policy against the backdrop of the economic downturn.

Yu Qiumei, Senior Statistician at National Bureau of Statistics of China noted that a great influence on prices in the last month had heavy rains and flooding of the Yangtze basin. "Powerful rains significantly affected the processes of production and transport of fresh vegetables, which led to a rather strong increase in their prices in a number of regions".

Also, the National Bureau of Statistics of China released data on producer price index, which in July fell by 1.7% after falling 2.6% in June. Analysts had expected a decline to -2.0%

-

08:19

Swiss unemployment stable at 3.1% in July

According to surveys conducted by the State Secretariat for Economic Affairs the unemployment rate remained at 3.1 % in June. Compared to the previous month , unemployment increased by 5'556 persons ( + 4.2% ) . Youth unemployment in July 2016 ( 15 to 24 year ) increased by 1,316 persons ( + 8.3% ) to 17'107 . Compared to the same month last year registered a decrease by 75 persons ( -0.4 %).

-

08:16

German trade balance lower than forecasts

Germany exported goods to the value of 106.8 billion euros and imported goods to the value of 82.0 billion euros in June 2016. Based on provisional data, the Federal Statistical Office (Destatis) also reports that German exports increased by 1.2% and imports by 0.3% in June 2016 year on year. Compared with May 2016, exports increased by a calendar and seasonally adjusted 0.3%, and imports by 1.0%.

The foreign trade balance showed a surplus of 24.9 billion euros in June 2016. In June 2015, the surplus amounted to 23.9 billion euros. In calendar and seasonally adjusted terms, the foreign trade balance recorded a surplus of 21.7 billion euros in June 2016.

According to provisional results of the Deutsche Bundesbank, the current account of the balance of payments showed a surplus of 26.3 billion euros in June 2016, which takes into account the balances of trade in goods including supplementary trade items (+26.8 billion euros), services (-2.7 billion euros), primary income (+4.4 billion euros) and secondary income (-2.1 billion euros). In June 2015, the German current account showed a surplus of 25.3 billion euros.

-

08:01

Germany: Trade Balance (non s.a.), bln, June 24.9

-

08:01

Japan: Prelim Machine Tool Orders, y/y , July -19.6%

-

08:00

Germany: Current Account , June 26.3

-

07:46

Switzerland: Unemployment Rate (non s.a.), July 3.3% (forecast 3.1%)

-

07:09

Global Stocks

European stocks finished a bit higher Monday, with gains for bank shares helping the regional benchmark eke out a nearly two-week high.

The Stoxx Europe 600 SXXP, +0.04% closed up less than 0.1% at 341.53. The pan-European index marked its best close since July 27, FactSet data showed.

The Stoxx 600 has advanced for four trading days in a row. The benchmark on Friday jumped 1.1%, continuing to gain after the Bank of England ramped up its stimulus efforts.

U.S. stocks closed lower Monday after touching record highs as Wall Street caught its breath in the wake of last week's upbeat jobs data.

The S&P 500 index SPX, -0.09% pulled back from an intraday record of 2,185.44, reached shortly after the opening bell, to close with a loss of 1.98 points, or 0.1%, at 2,180.89. The index was dragged down by a sharp drop in health-care stocks, which outweighed a rise in energy shares that accompanied strong gains for crude-oil futures CLU6, -0.81%

The Dow Jones Industrial Average DJIA, -0.08% closed down 14.24 points, or 0.1%, at 18,529.29. A 1.6% drop in shares of Merck & Co. MRK, -1.57% and a 1.4% decline in Pfizer Inc. PFE, -1.44% shares dragged the blue-chip gauge down. Oil giant Exxon Mobil Corp. XOM, +1.18% was the average's best performer with a 1.2% gain, while Chevron Corp. CVX, +0.69% shares closed up 0.7%.

The Nasdaq Composite Index COMP, -0.15% fell 7.98 points, or 0.2%, to close at 5,213.14, after logging its first closing record in more than a year on Friday, following the employment report. Earlier in the session, the index carved out a new all-time intraday high of 5,228.40.

Asian shares stood atop one-year peaks on Tuesday as investors' desperate search for yield drove a record inflow into emerging market funds, while the pound slipped to one-month lows on speculation of further policy easing in the UK.

Analysts at Bank of America Merrill Lynch noted the search for yield had led to the largest 5-week inflow on record to emerging market debt funds and the longest inflow streak to equity funds in two years.

MSCI's broadest index of Asia-Pacific shares outside Japan .MIAPJ0000PUS gained 0.1 percent, having already risen for three sessions in a row.

Japan's Nikkei .N225 was also attempting a fourth session of gains with a tentative rise of 0.2 percent, while Shanghai stocks .SSEC were flat.

The major data out in Asia was Chinese inflation for July and it caused few ripples by coming exactly as forecast at 1.8 percent ECONCN. The benign result merely confirmed there was plenty of scope for further policy easing if needed.

The need for stimulus was clear in Chinese trade flows which disappointed in July amid slack demand both at home and abroad.

-

03:31

Australia: National Australia Bank's Business Confidence, July 4

-

03:30

China: CPI y/y, July 1.8% (forecast 1.8%)

-

03:30

China: PPI y/y, July -1.7% (forecast -2.0%)

-

00:31

Commodities. Daily history for Aug 08’2016:

(raw materials / closing price /% change)

Oil 42.87 -0.35%

Gold 1,341.00 -0.02%

-

00:29

Stocks. Daily history for Aug 08’2016:

(index / closing price / change items /% change)

Nikkei 225 16,650.57 +396.12 +2.44%

Shanghai Composite 3,004.72 +28.02 +0.94%

S&P/ASX 200 5,537.84 +40.43 +0.74%

FTSE 100 6,809.13 +15.66 +0.23%

CAC 40 4,415.46 +4.91 +0.11%

Xetra DAX 10,432.36 +65.15 +0.63%

S&P 500 2,180.89 -1.98 -0.09%

Dow Jones Industrial Average 18,529.29 -14.24 -0.08%

S&P/TSX Composite 14,755.62 +106.85 +0.73%

-

00:28

Currencies. Daily history for Aug 08’2016:

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1085 -0,01%

GBP/USD $1,3041 -0,28%

USD/CHF Chf0,9826 +0,21%

USD/JPY Y102,40 +0,59%

EUR/JPY Y113,53 +0,57%

GBP/JPY Y133,56 +0,40%

AUD/USD $0,7654 +0,48%

NZD/USD $0,7149 +0,11%

USD/CAD C$1,3162 -0,08%

-

00:04

Schedule for today, Tuesday, Aug 09’2016

(time / country / index / period / previous value / forecast)

01:30 Australia National Australia Bank's Business Confidence July 6

01:30 China PPI y/y July -2.6% -2.0%

01:30 China CPI y/y July 1.9% 1.8%

05:45 Switzerland Unemployment Rate (non s.a.) July 3.1%

06:00 Germany Current Account June 17.5

06:00 Germany Trade Balance (non s.a.), bln June 21

06:00 Japan Prelim Machine Tool Orders, y/y July -19.9%

08:30 United Kingdom Industrial Production (MoM) June -0.5% 0.2%

08:30 United Kingdom Industrial Production (YoY) June 1.4% 1.6%

08:30 United Kingdom Manufacturing Production (MoM) June -0.5% -0.2%

08:30 United Kingdom Manufacturing Production (YoY) June 1.7% 1.3%

08:30 United Kingdom Total Trade Balance June -2.263

12:15 Canada Housing Starts July 218.3

12:30 U.S. Unit Labor Costs, q/q (Preliminary) Quarter II 4.5% 1.8%

12:30 U.S. Nonfarm Productivity, q/q(Preliminary) Quarter II -0.6% 0.5%

14:00 United Kingdom NIESR GDP Estimate July 0.6%

14:00 U.S. Wholesale Inventories June 0.1% 0%

23:50 Japan Core Machinery Orders June -1.4% 3.1%

23:50 Japan Core Machinery Orders, y/y June -11.7% -4.2%

-